August's labor market report delivered a jarring reality check with employers adding a meager 22,000 jobs, dramatically below expectations of around 77,000. This marks a fundamental shift in the employment landscape as job openings have fallen below the number of unemployed individuals for the first time since 2021. The unemployment rate climbed to 4.3%, reaching its highest level since 2021, confirming what monthly trend data has been suggesting: the labor market is losing momentum much faster than anticipated. What's particularly notable is the composition of these changes. Health care added 31,000 positions, but these gains were offset by losses in federal government employment and manufacturing sectors. The rapid deterioration suggests we may be approaching a tipping point where Fed policy will need to shift more decisively toward supporting employment rather than fighting inflation.

Manufacturing weakness continues to weigh on the broader economy with the Institute for Supply Management reporting the sixth consecutive month of contraction in the sector. This isn't just a temporary dip, but increasingly appears to be a structural issue affecting multiple industries. New orders have shown persistent weakness, indicating demand isn't showing signs of meaningful recovery. Perhaps most concerning is the employment component. It’s saying that manufacturers are actively reducing their workforces in response to prolonged weak conditions. I suspect this manufacturing slump will be harder to reverse than many expect, potentially creating headwinds for any economic rebound even after the Fed begins its cutting cycle.

Bond markets have responded decisively to these developments with traders now pricing in increased expectations for Fed rate cuts. This represents a significant shift from just a month ago when the debate centered on whether the Fed would cut at all in September or wait until late 2025/early 2026. Analysts now anticipate the Federal Reserve might lower rates by 75 basis points before year-end (with an outside shot at 100), a significant revision to the expected policy path. The yield curve has steepened as short-term rates fall while longer-dated yields hold up better, suggesting markets believe aggressive Fed action could prevent a deeper economic downturn. This rapid repricing creates a tricky environment for investors.Equities have proven surprisingly resilient so far. Major indices are still hovering near record highs despite deteriorating fundamentals. This disconnect between market pricing and economic reality creates a challenging setup as we head toward what historically has been the most volatile period of the year.

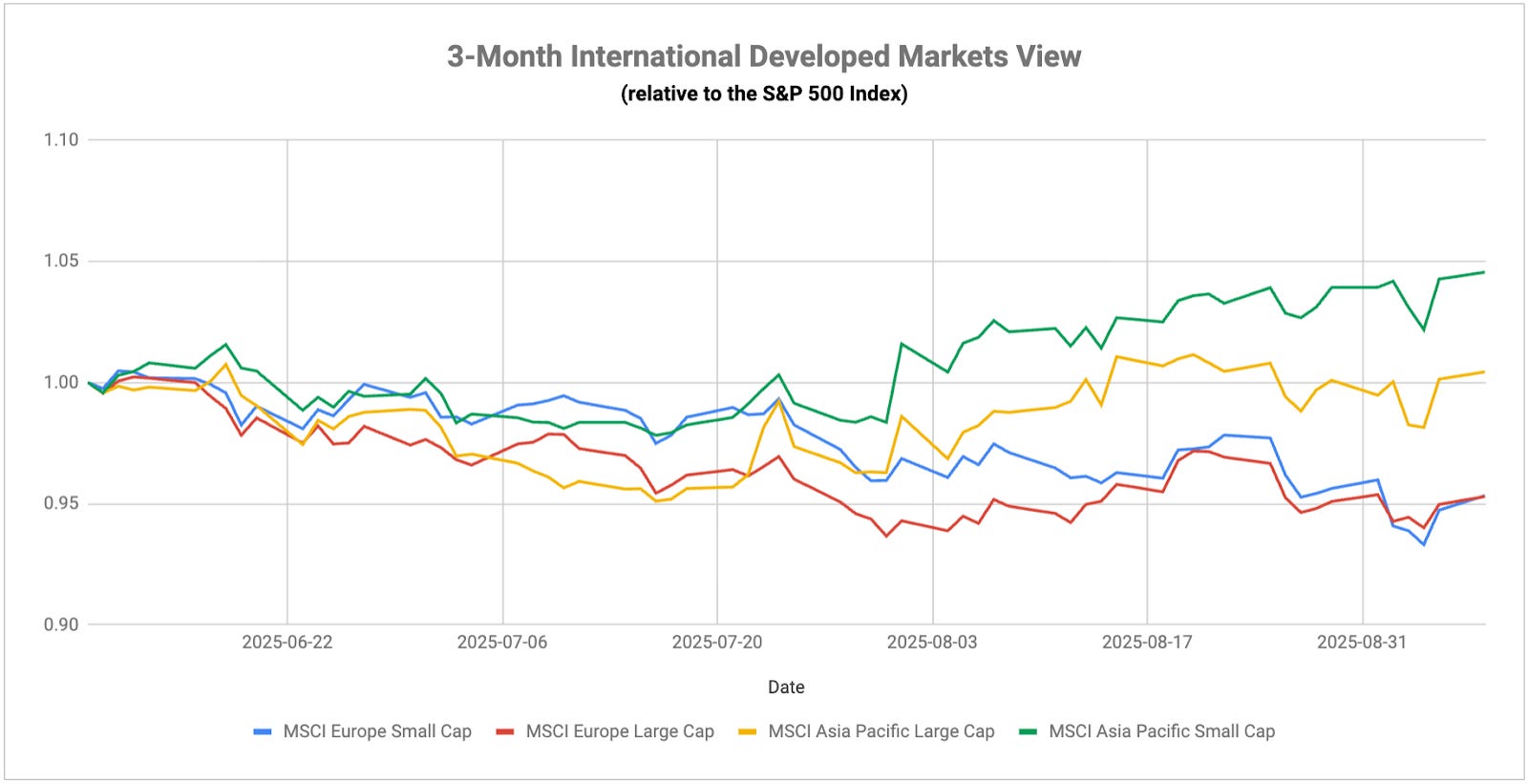

European economic sentiment has deteriorated sharply in recent weeks with some indicators falling to multi-year lows. The regional recovery was delicate to begin with, but this broader-based decline has touched nearly every sector and major economy within the bloc. Industrial confidence has plummeted, while services sentiment has also fallen significantly. Germany, the region's largest economy, has seen particularly steep declines, reflecting growing concerns about the manufacturing sector's persistent weakness. French sentiment has also deteriorated following political turbulence from recent elections, creating additional uncertainty for businesses already dealing with geopolitical pressures. The timing couldn't be worse for the ECB, which had been planning to pause its cutting cycle after the September meeting to assess inflation trends, but may now face pressure to continue easing despite core inflation remaining above target.