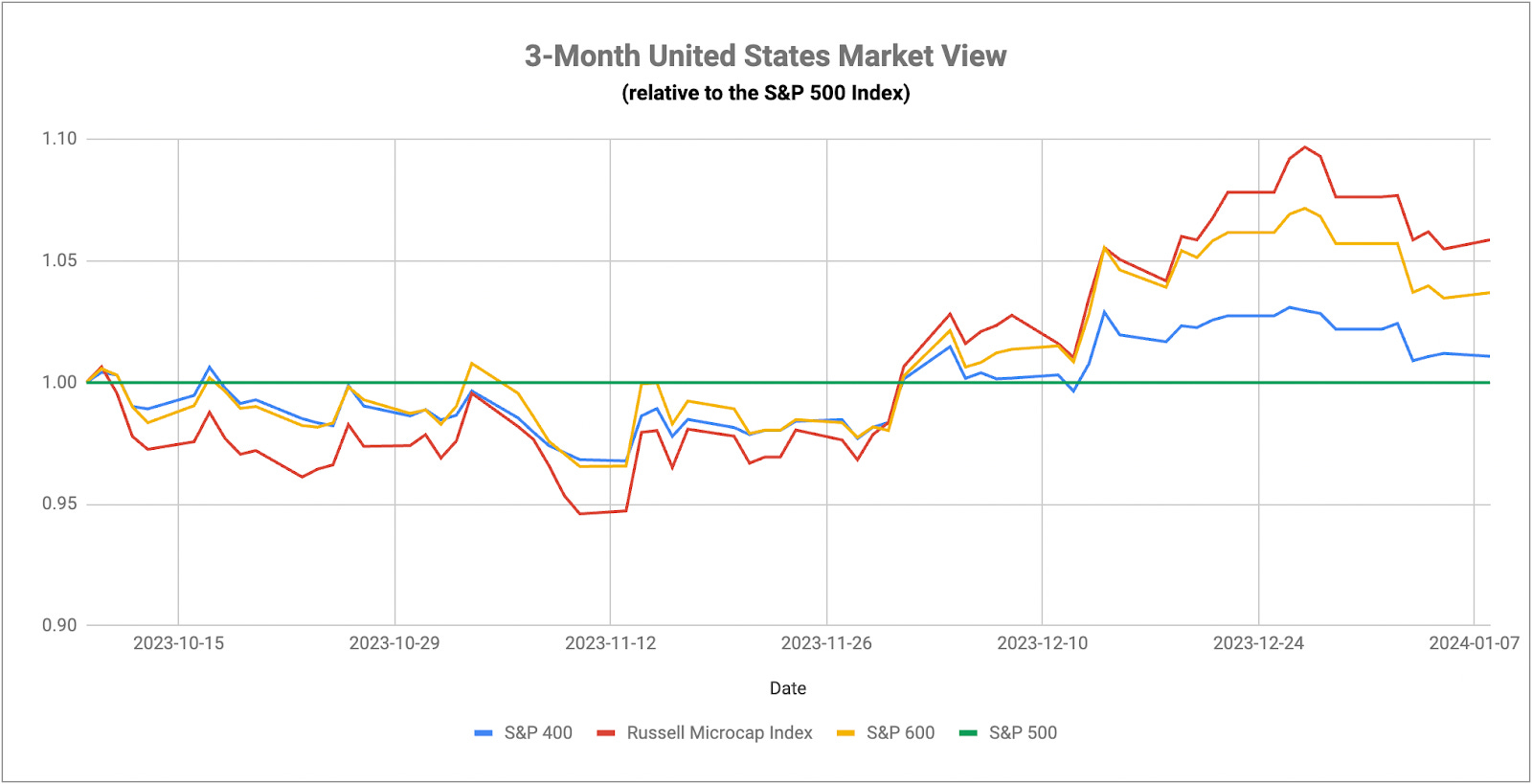

While the big pivot to defensive themes is taking a bit of a breather to start this week, it’s still hanging close to the major indices, which would be a good sign indicating this move isn’t just a flash in the pan. The VIX is still subdued and 10-year Treasury yields are hanging around the 4% level, so this could be a short-term pause where investors start digesting all the information they’ve gotten since the Fed meeting before planning their next moves. The small-cap breakout failed and has been sucked back into the trading range it’s been in for nearly two years. This is important because 1) it’s essentially confirming what we’re seeing elsewhere in the equity markets, which is defensive leadership and 2) small-caps are usually leaders in big cyclical recovery trades. If this group breaks down, it’s a sign that investors aren’t actually buying into the soft landing narrative as much as they’d have you believe.

The market is still signaling its expectation for 5-6 rate cuts in 2024, but we’re still getting mixed signals from the Fed. Dallas Fed president Lorie Logan said just this week that rate hikes shouldn’t be off the table in order to prevent another inflation spike, citing the recent plunge in Treasury yields. Fed governor Michelle Bowman said that, while rate hikes are likely over, she doesn’t think they should be cutting yet. If inflation continues moving closer to the central bank’s 2% target, which it’s already done on a short-term trend basis, it certainly makes sense to begin backing off on policy restrictiveness, but investors appear to be a little early in declaring the Fed’s job finished. The markets have already priced risk assets as if there are a half dozen cuts coming in the next 12 months, leaving very little room for error in the process. If Powell follows through on his expectation of only 2-3 cuts in 2024, stocks will likely need to correct in the process.

Would the Fed be taking the right path by cutting 2-3 times this year versus the 5-6 the market is expecting. I think you can argue the answer is yes. Back in 2022, the Fed didn’t hike for the first time until the inflation rate was nearly 8%. Right now, GDP growth is still healthy and inflation is at around 3%, but trending sideways, not down. Cutting by 50-75 basis points now starts to normalize the gap between the Fed Funds rate and the inflation rate, while still keeping some pressure on inflation from experiencing a second surge. If inflation does eventually return closer to 2% without any spike or the economy starts trending towards recession, you’ve already started the clock on the 12-month lag that’s typically needed for rate cuts to get baked in. If the soft landing is achieved, you’ve minimized some of the risk of overswinging too far in the other direction. It could be a happy medium for monetary policy, although one that the Fed doesn’t typically take.

The narrative in Japan has quickly shifted from “when will the BoJ tighten policy conditions” to “should they be tightening at all”.