Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: THE GREAT ROTATION IS CONFIRMED -- FROM WAR TRADES TO GROWTH

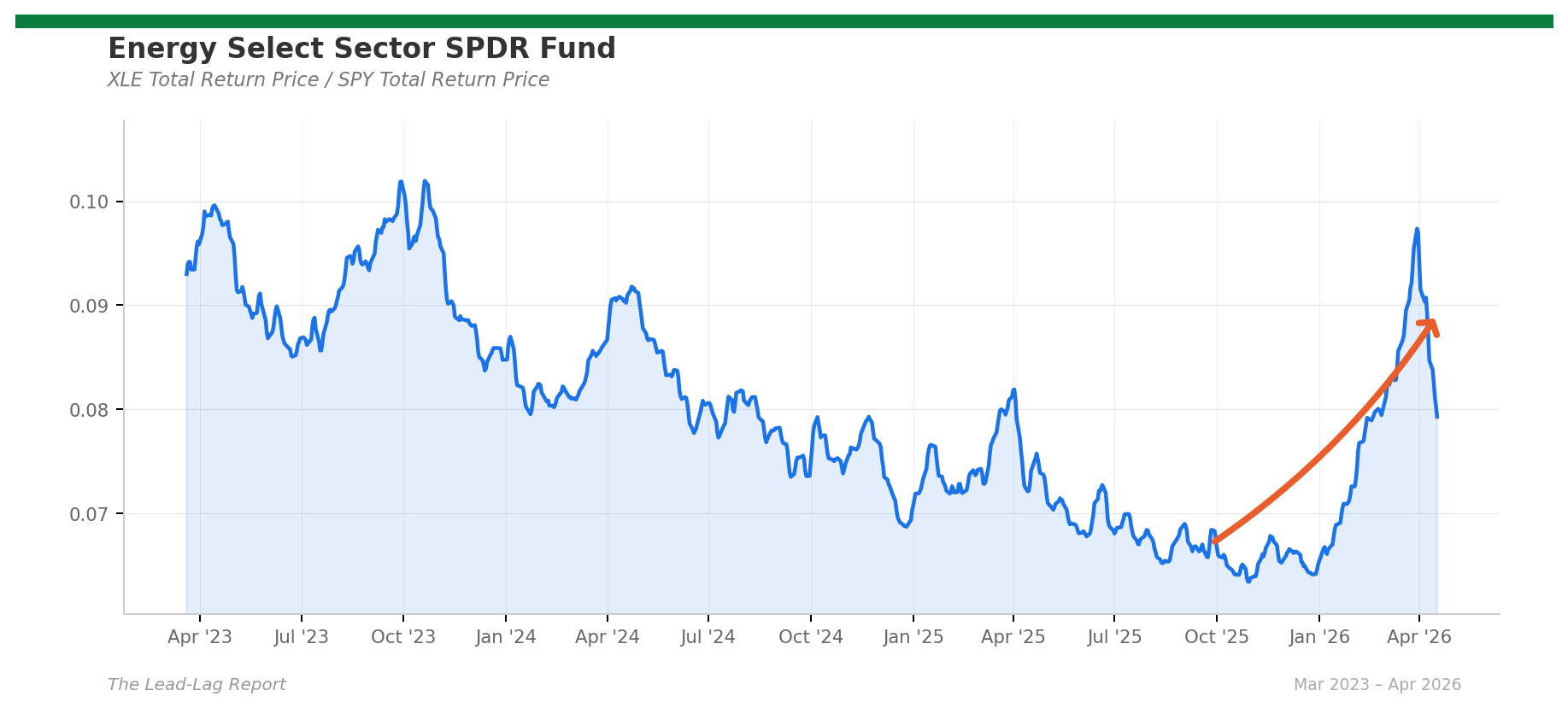

Energy (XLE) -- Still the Three-Month Leader, but the Unwind Just Accelerated

Energy remains the three-month leader at +12.8%, but the weekly decline of 6.9% was the fourth consecutive week of underperformance relative to SPY. On Friday, Iran’s Foreign Minister announced the Strait of Hormuz is “completely open,” sending WTI crude plunging 11% to $83.85 and Brent 9.1% to $90.38. Energy stocks fell 2.94% on Friday. The one-month picture at -13.6% tells the story of how fast the war premium is pricing out. I’m keeping energy as a leader on the three-month trend, but this ratio may cross into laggard territory within weeks if the ceasefire extends past April 22.

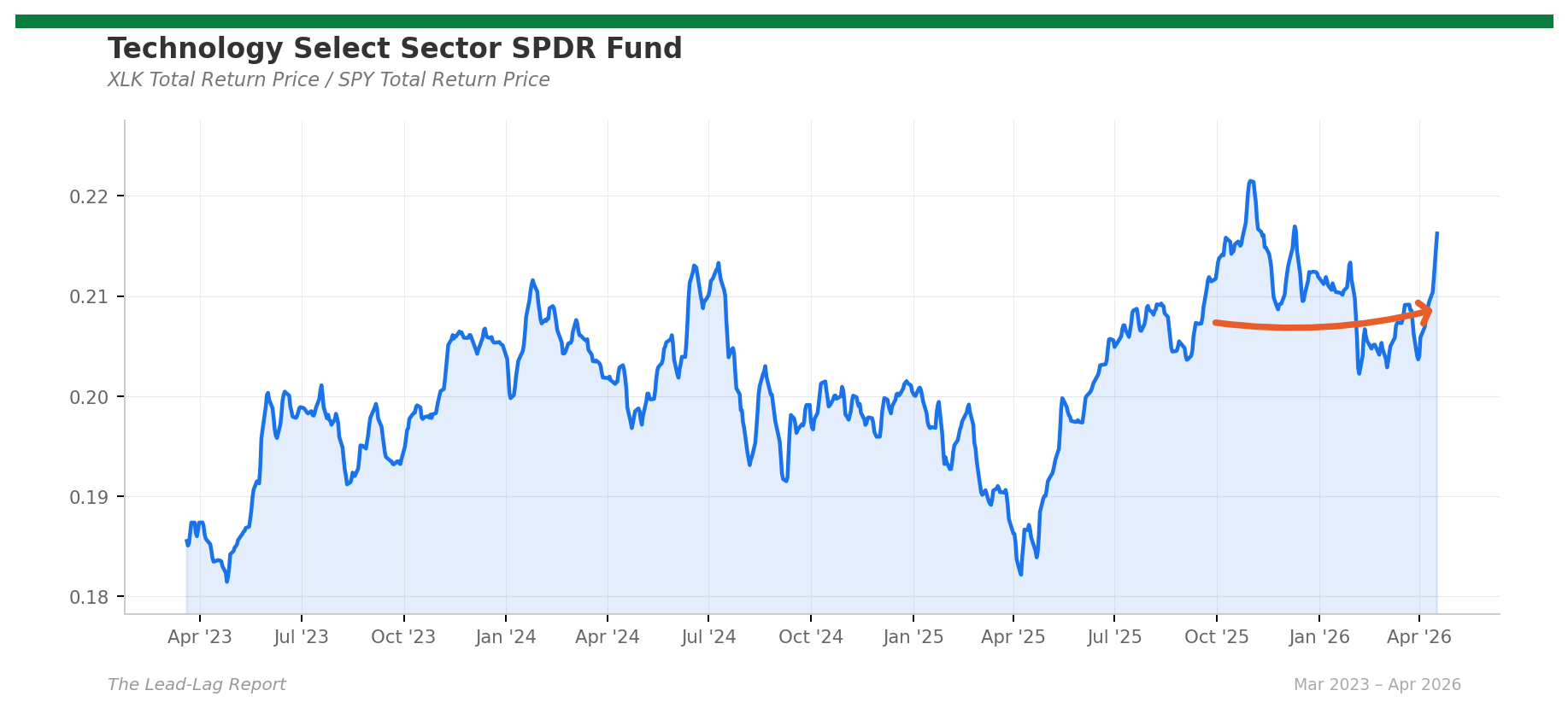

Technology (XLK) -- The Inflection Is Confirmed: Tech Is a Leader Again

This is the most important classification change of the cycle. Technology’s three-month ratio vs SPY is now +3.1%, with a one-month gain of 3.4%. The Nasdaq hit its longest winning streak since 1992, gaining 6.8% for the week. Oil falling from $112 to $84 compresses inflation expectations, pulling down the discount rate on growth earnings. Technology has officially moved from laggard to leader.

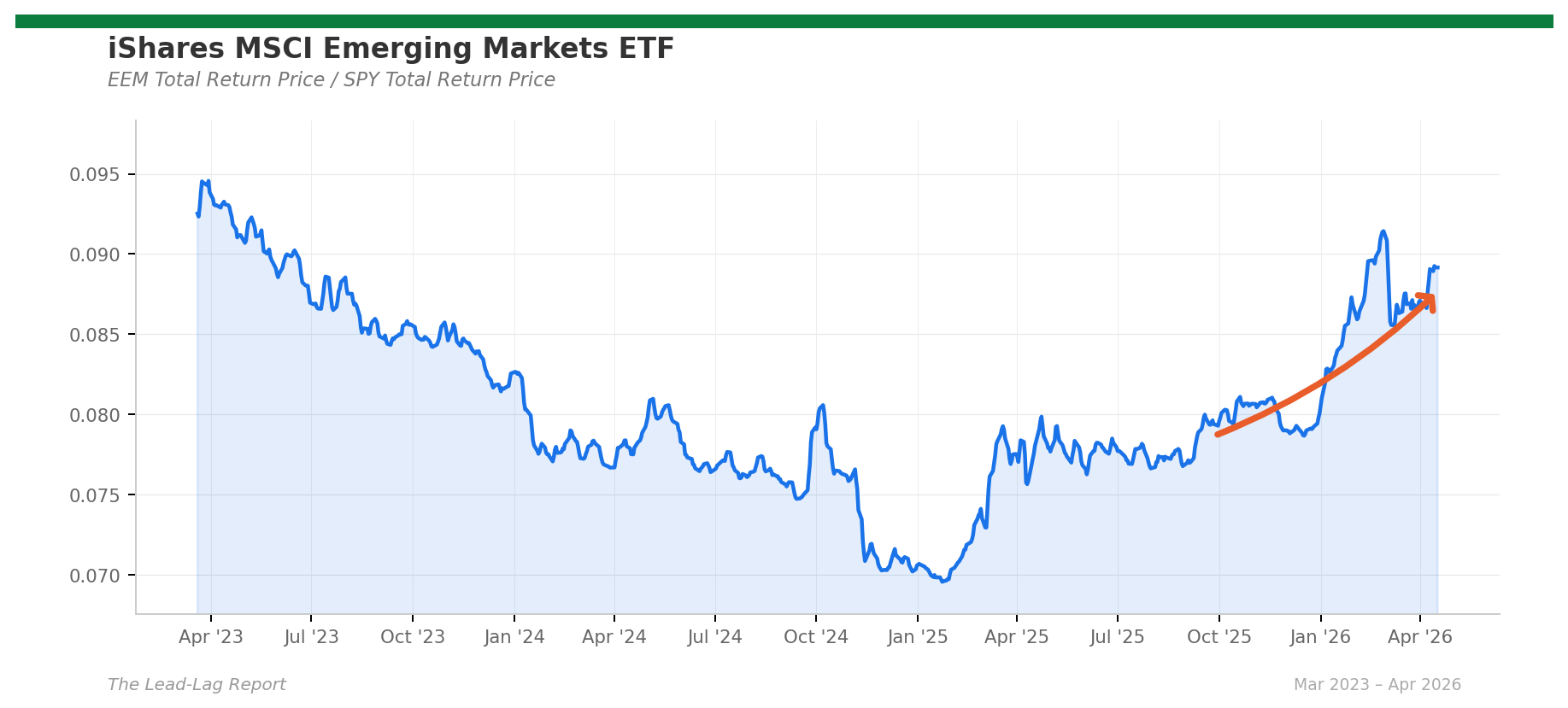

Emerging Markets (EEM) -- The Biggest Ceasefire Winner

Emerging markets gained 0.7% relative to SPY this week and the three-month outperformance of 6.8% makes it the second-strongest leader. The Strait reopening is the most bullish development for EM trade flows since the war began. Credit spreads at 2.84% provide additional tailwind.

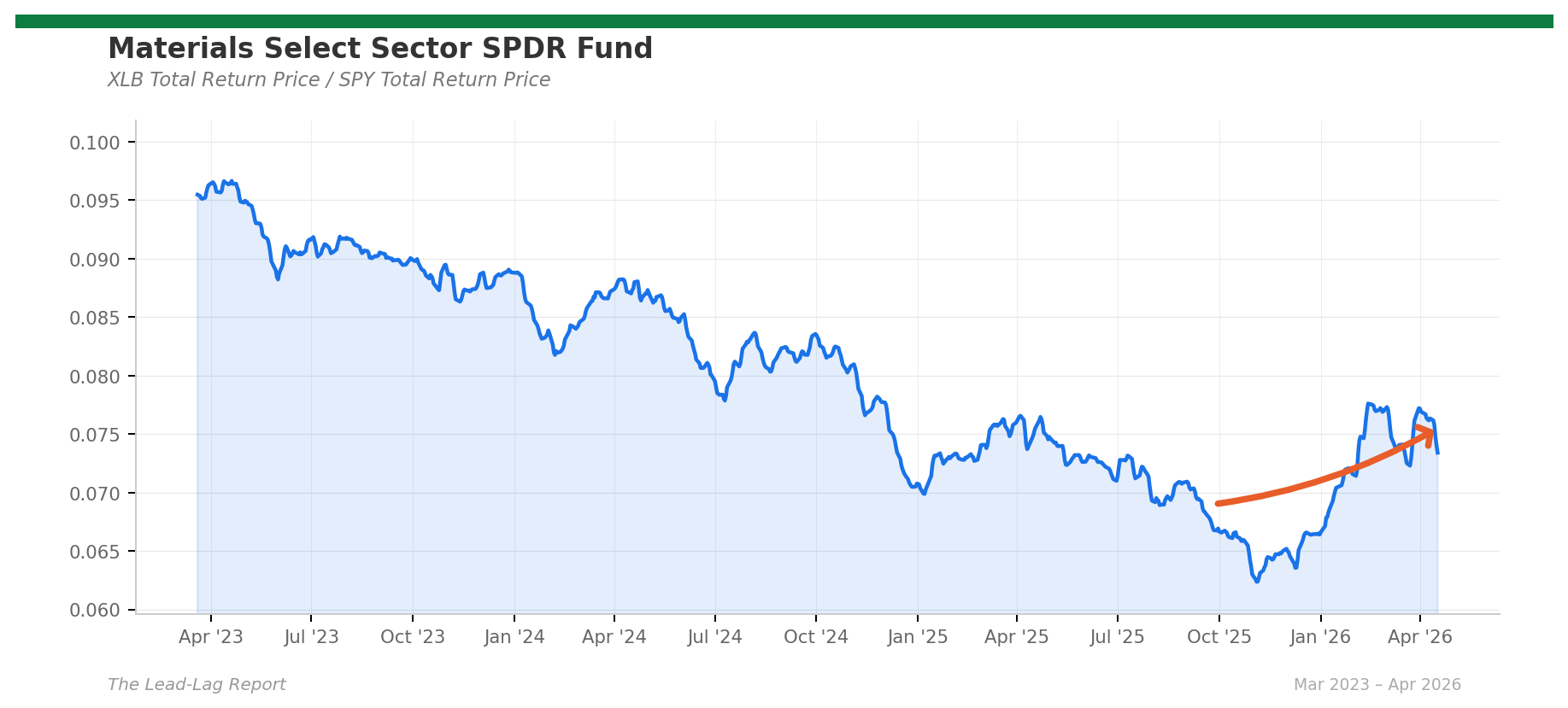

Materials (XLB) -- The Structural Leader Survives

Materials pulled back 4.0% relative to SPY but the three-month outperformance of 4.0% keeps it in the leader column. Reshoring demand, defense spending, and tariff-driven import substitution are independent of the Iran conflict.

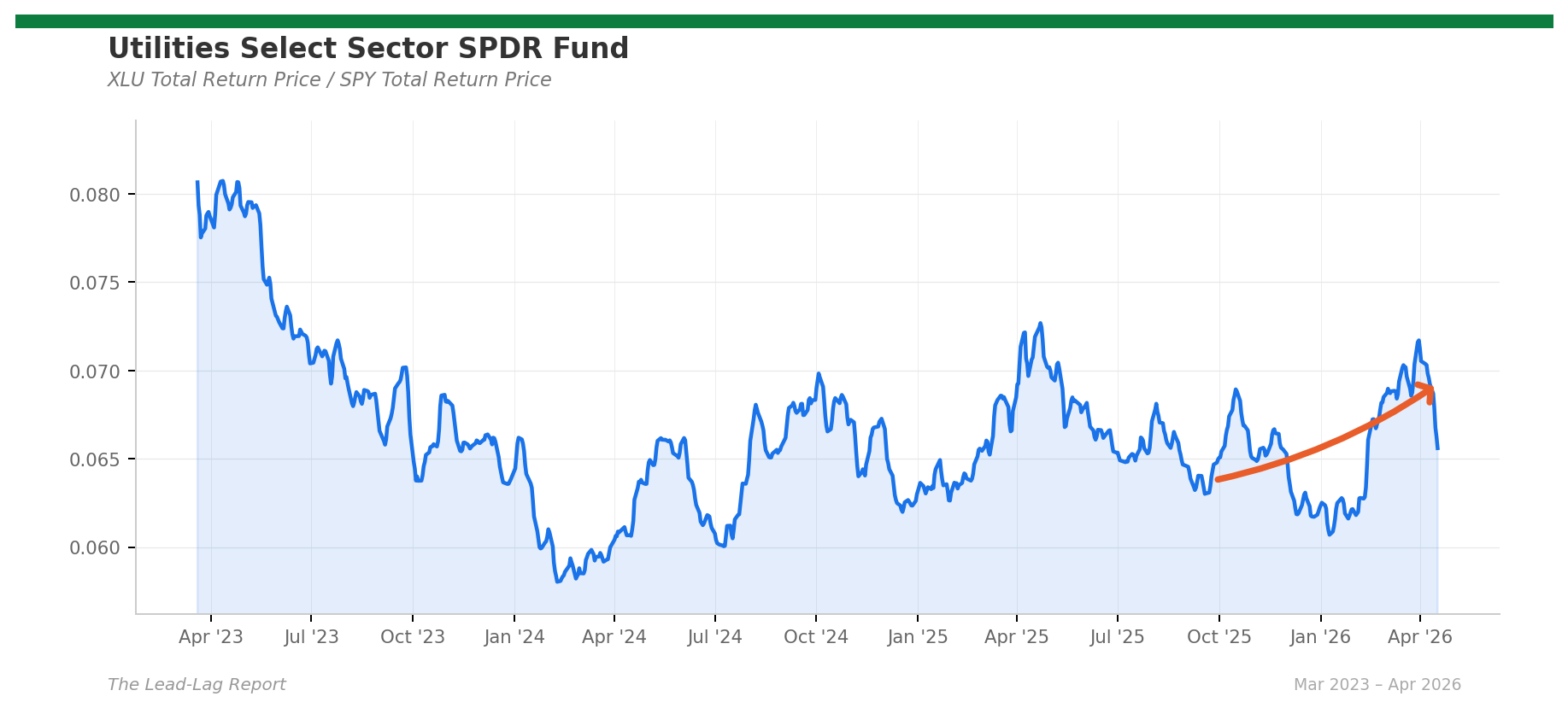

Utilities (XLU) -- The Defensive Trade’s Final Chapter

Utilities fell 3.9% relative to SPY and the three-month outperformance compressed from 13.3% two weeks ago to 4.1%. VIX below 20, oil collapsing, S&P at all-time highs -- worst environment for defensives.

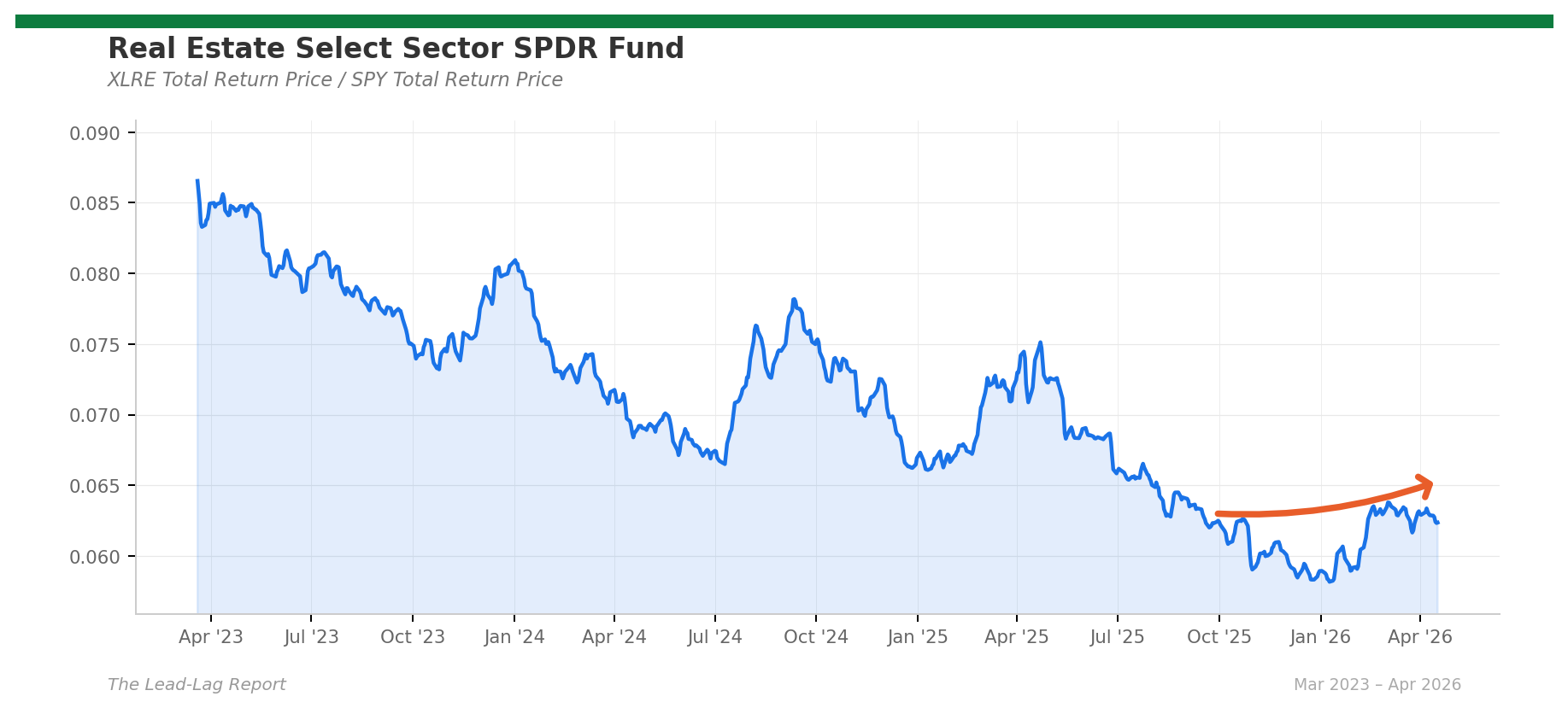

Real Estate (XLRE) -- Rate Relief Arrives

Real estate was flat relative to SPY, preserving 3.0% three-month outperformance. The 10-year yield fell to 4.24% and the 2-year dropped below the Fed Funds rate of 3.75%.

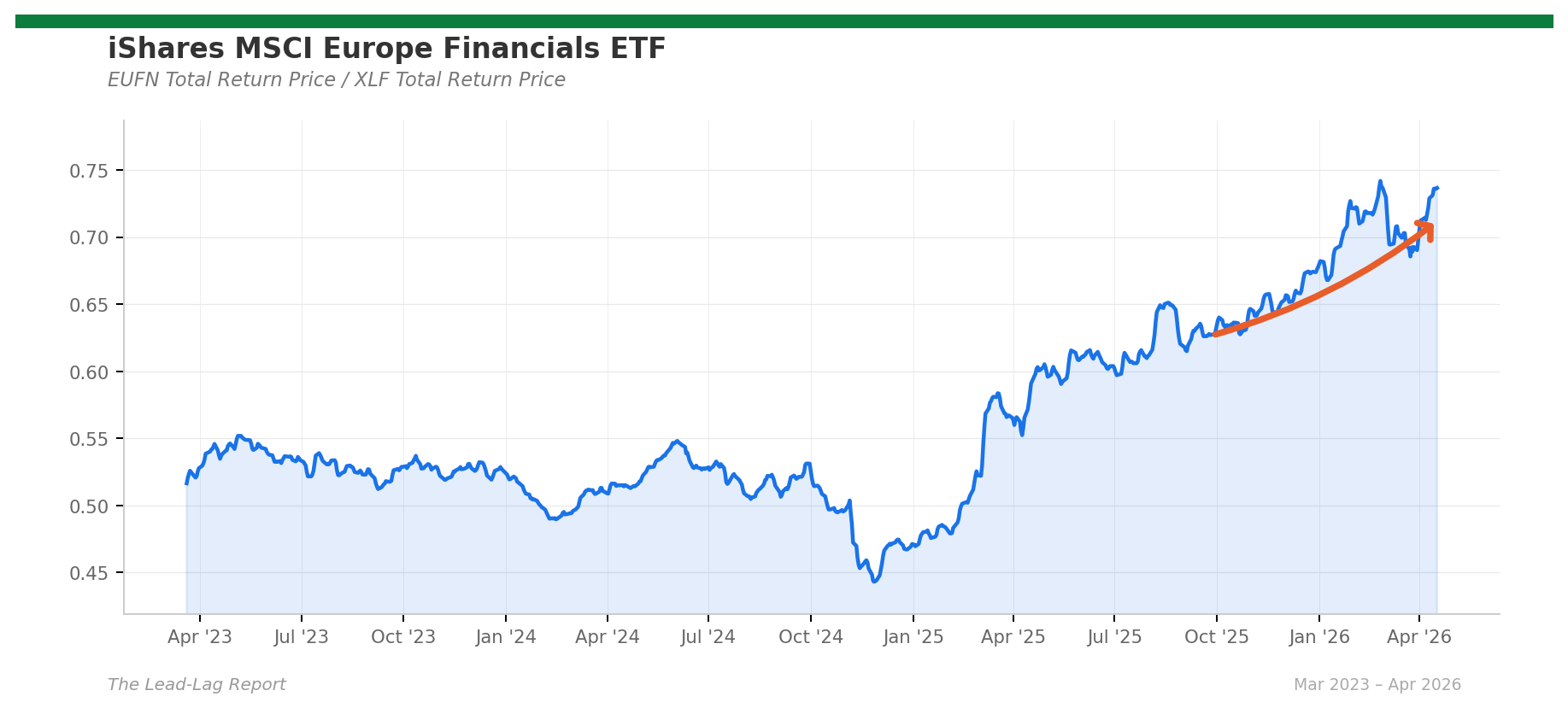

European Banks vs U.S. Banks (EUFN/XLF) -- The Transatlantic Divergence

EUFN/XLF gained 1.1% this week and is up 7.1% over three months. European banks are the most consistent peace trade beneficiaries. U.S. banks remain stuck in laggard territory.

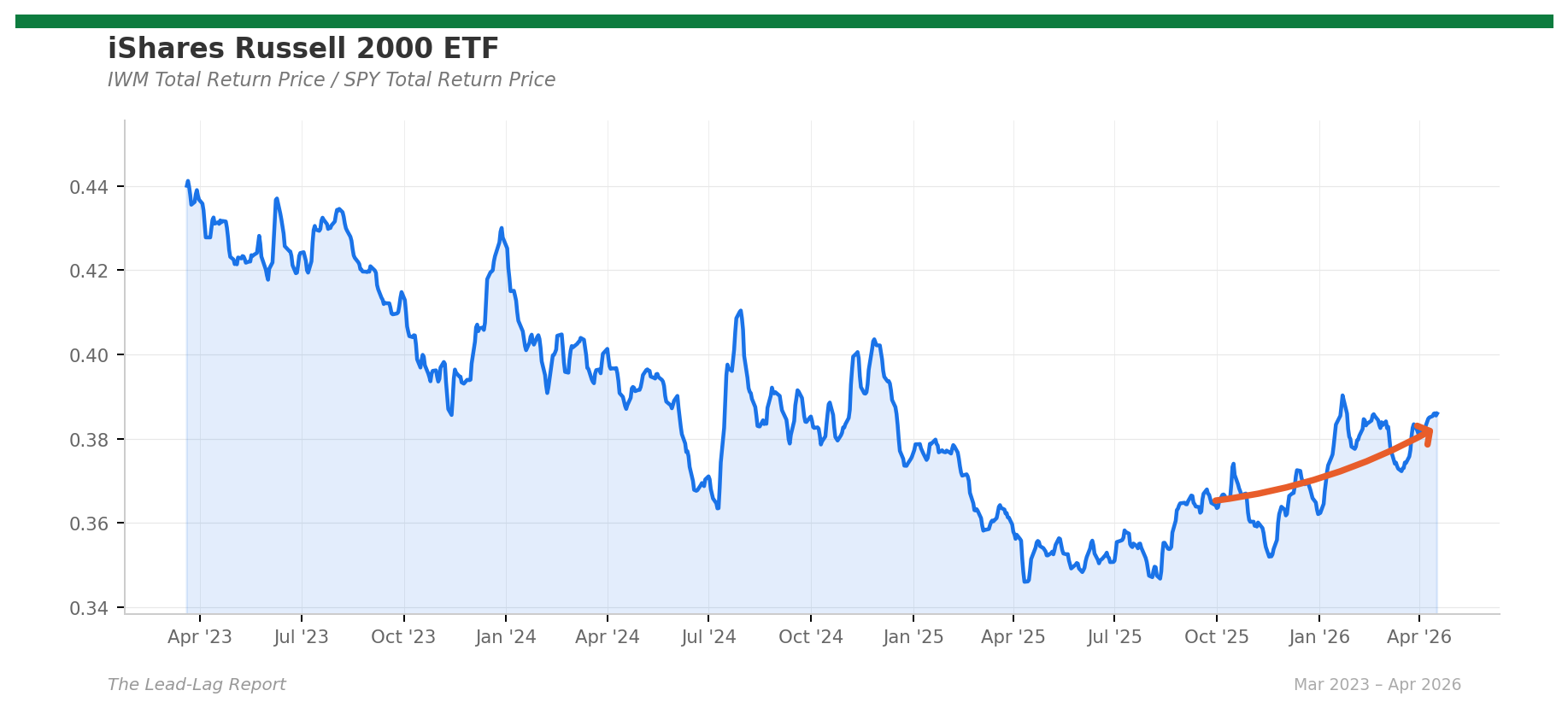

Small-Caps (IWM) -- Domestic Recovery Holds

Small-caps gained 0.5% relative to SPY. The Russell 2000 surged 5.6% -- best weekly performance of any major index. Credit spreads at 2.84% are well below pre-war levels.

LAGGARDS: THE WAR’S CASUALTIES AND THE SECTORS STILL SEARCHING

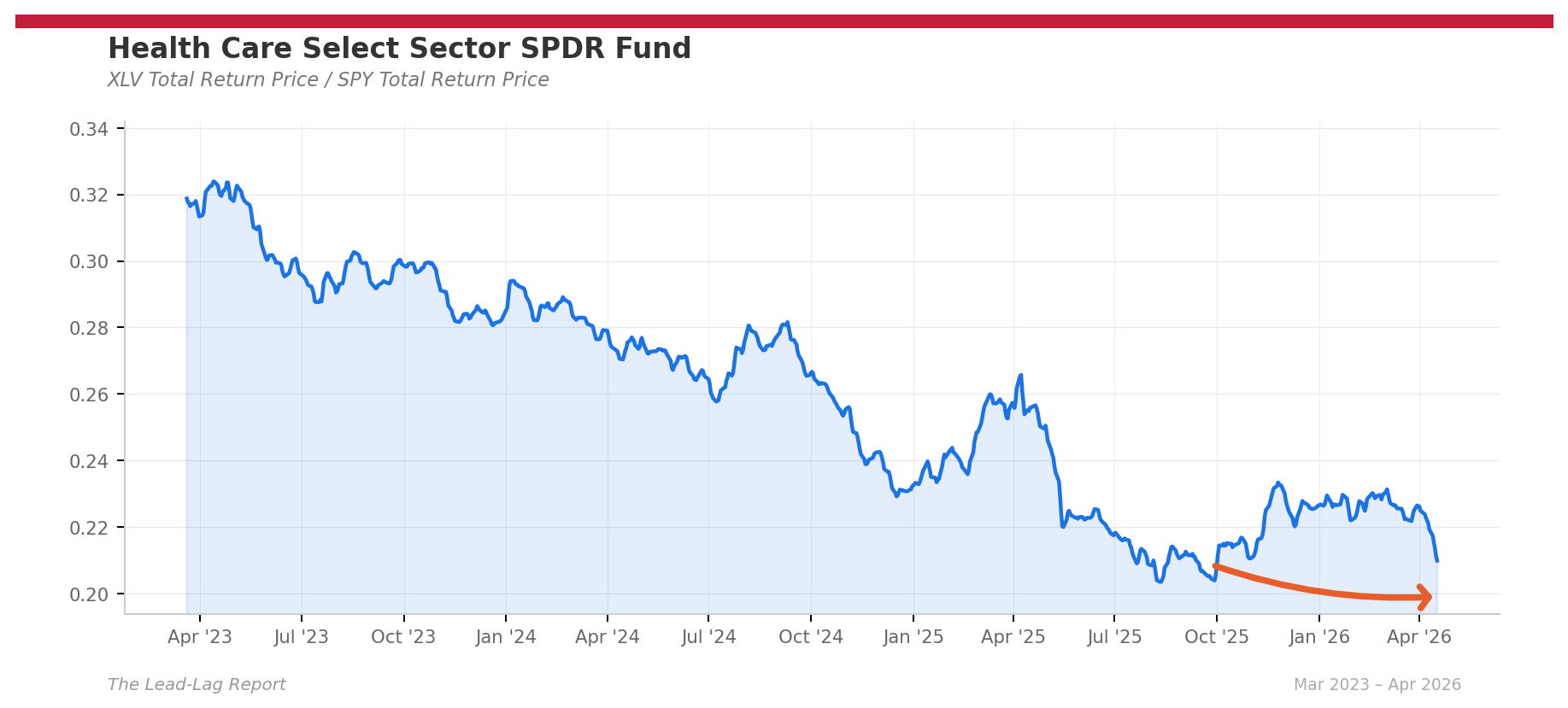

Health Care (XLV) -- The Deepest Laggard

Health care fell 2.8% relative to SPY. The -6.8% three-month ratio is the deepest laggard.

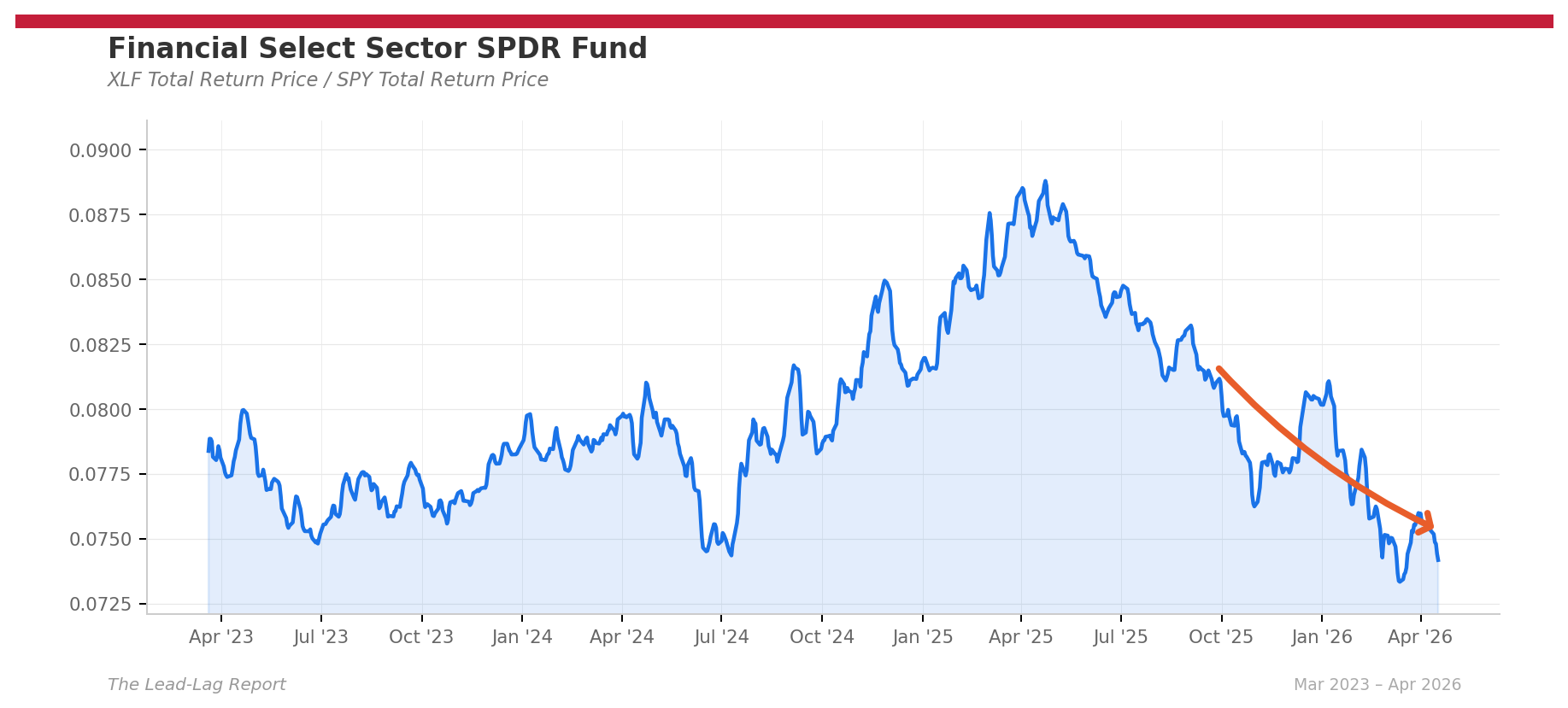

Financials (XLF) -- Credit Heals, Equity Doesn’t

Financials fell 1.9% relative to SPY despite HY OAS at 2.84%. The -6.0% three-month ratio is the second-deepest laggard. European banks outperform U.S. banks by 7.1% over three months.

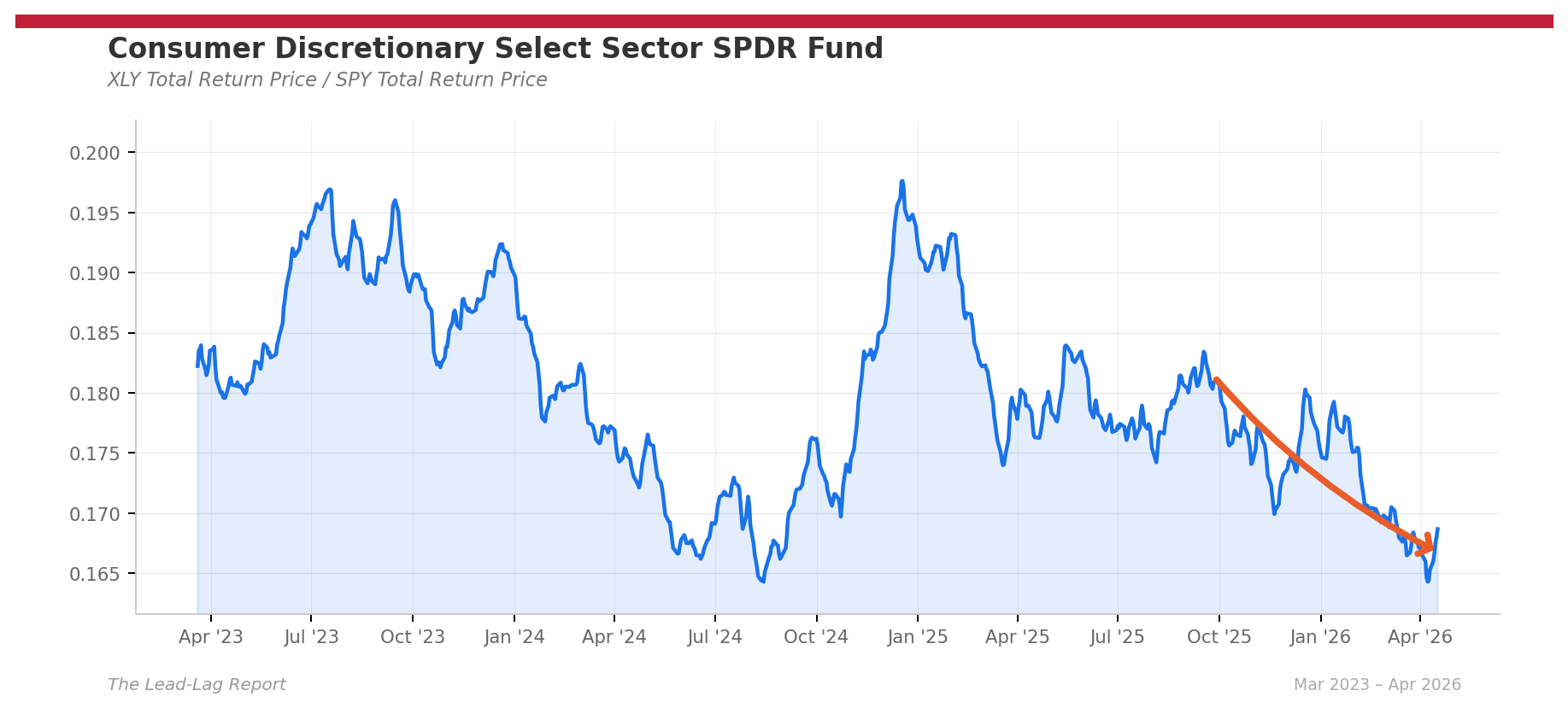

Consumer Discretionary (XLY) -- A Reprieve

Consumer discretionary gained 2.1% relative to SPY as oil’s collapse sent cruise lines surging. But -4.2% three-month keeps it in laggard territory.

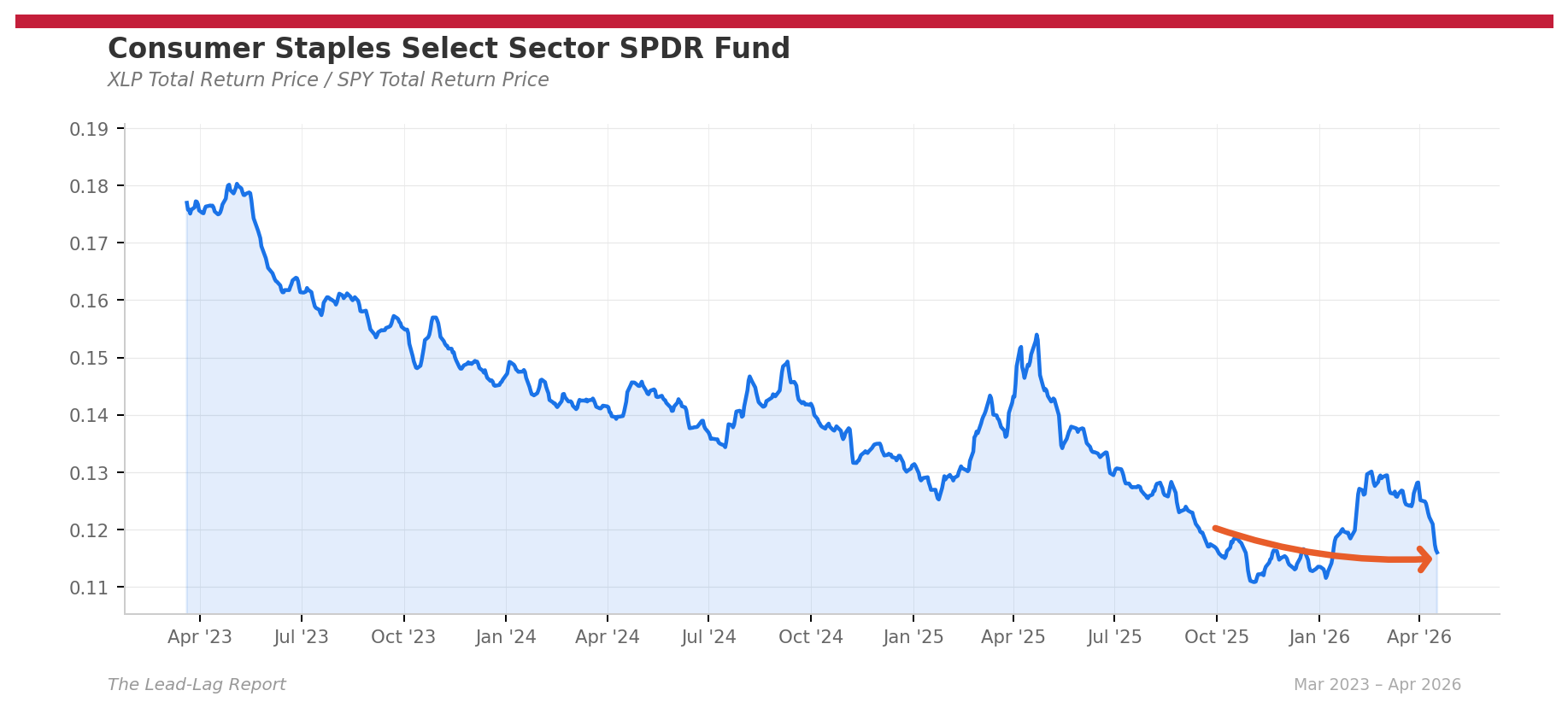

Consumer Staples (XLP) -- Former Leader Now Negative

Staples fell 2.3% relative to SPY. The three-month ratio flipped negative at -1.9%. Four weeks ago this was a +14.1% leader.

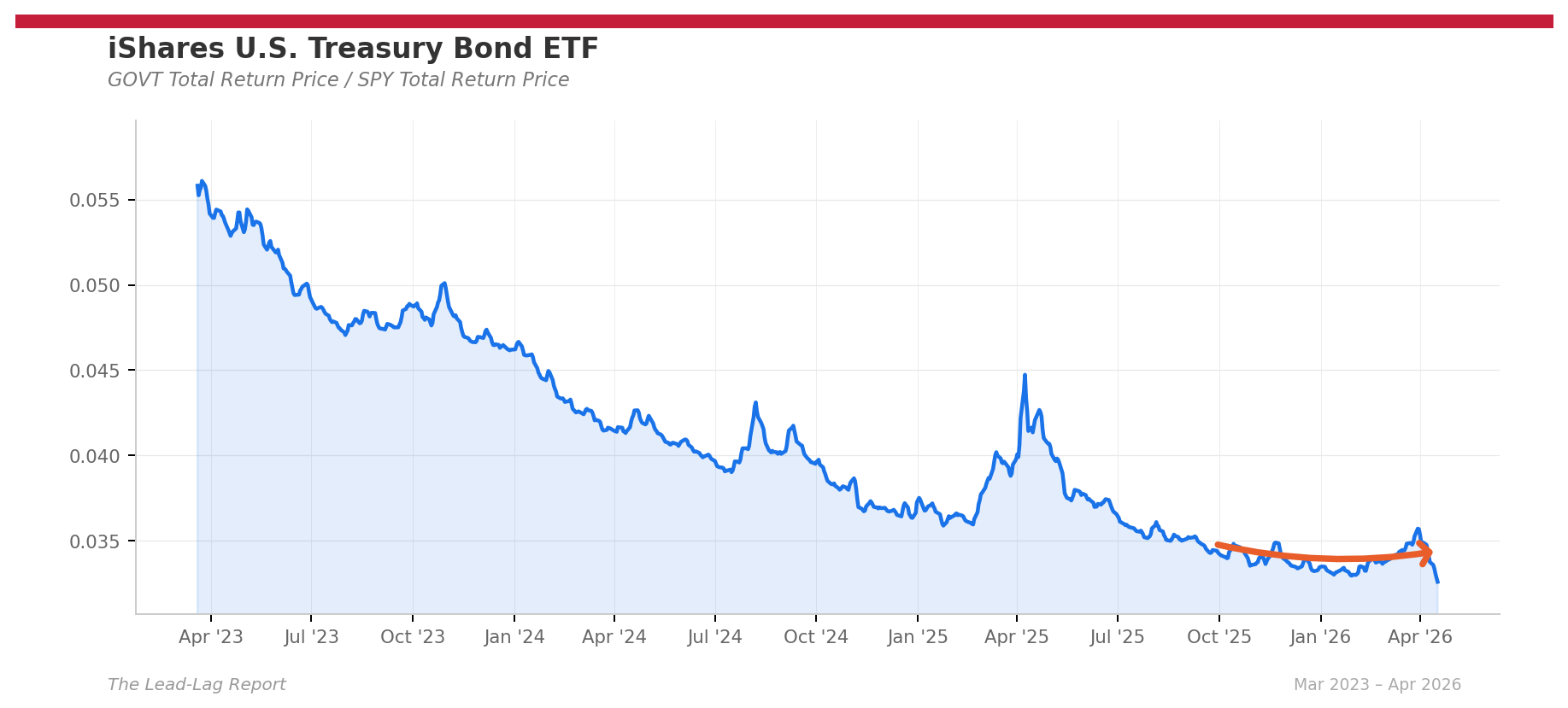

Treasuries (GOVT) -- Bonds Lose Their Edge

GOVT/SPY fell 3.0% this week. The 10-year yield fell to 4.24%, but equities rallied +4.5%. The peace dividend is an equity story, not a bond story.

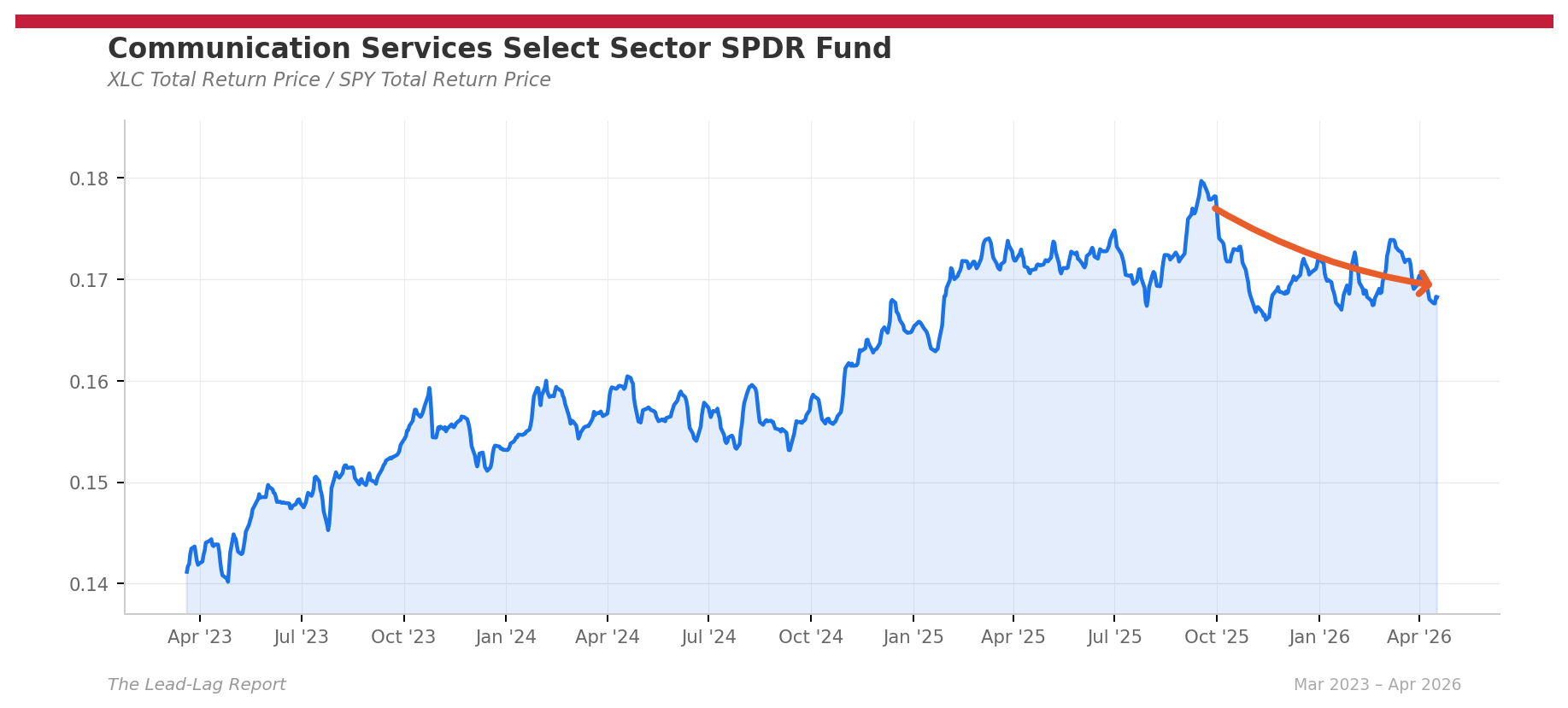

Communication Services (XLC) -- Sideways

Comm services gained 0.2% relative to SPY despite the Nasdaq’s 6.8% surge.

Gold -- Insurance the Market Won’t Cancel

Gold rose to $4,866.60 even as equities hit all-time highs. The ceasefire expires April 22, and Trump said the blockade “remains in full force.”

Lumber/Gold Ratio -- Gold Overwhelms the Signal

Lumber at $581.50 is stable but gold’s march to $4,866 keeps compressing the ratio.

The week ending April 17 may be the week the war ended in the market’s eyes. Iran reopened the Strait of Hormuz. Oil collapsed 11% to $83.85. The S&P 500 crossed 7,100 for the first time (7,126.06) -- a new all-time high, fully recovering all war losses. The Nasdaq posted its longest winning streak since 1992. Credit spreads at 2.84%. Technology has officially flipped from laggard to leader. The ceasefire expires April 22. Stay positioned accordingly.

Data Sources

1. WSJ | 2. Washington Post | 3. Xinhua | 4. CNBC | 5. El Pais | 6. WA Trust | 7. FRED HY OAS | 8. Yahoo Finance via yfinance

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.