Are Central Banks About to Dump Gold to Defend Fiat Power?

If Central Banks Sell Gold, What Would It Signal About Fiat Confidence?

Key Highlights

A sustained shift from net official gold buying to net selling would mark a meaningful regime change in global reserve management.

The reason for selling matters more than the headline. Orderly portfolio rebalancing signals confidence; emergency liquidity sales signal stress.

Gold’s role in a fiat system is tied to trust, crisis insurance, and geopolitical hedging.

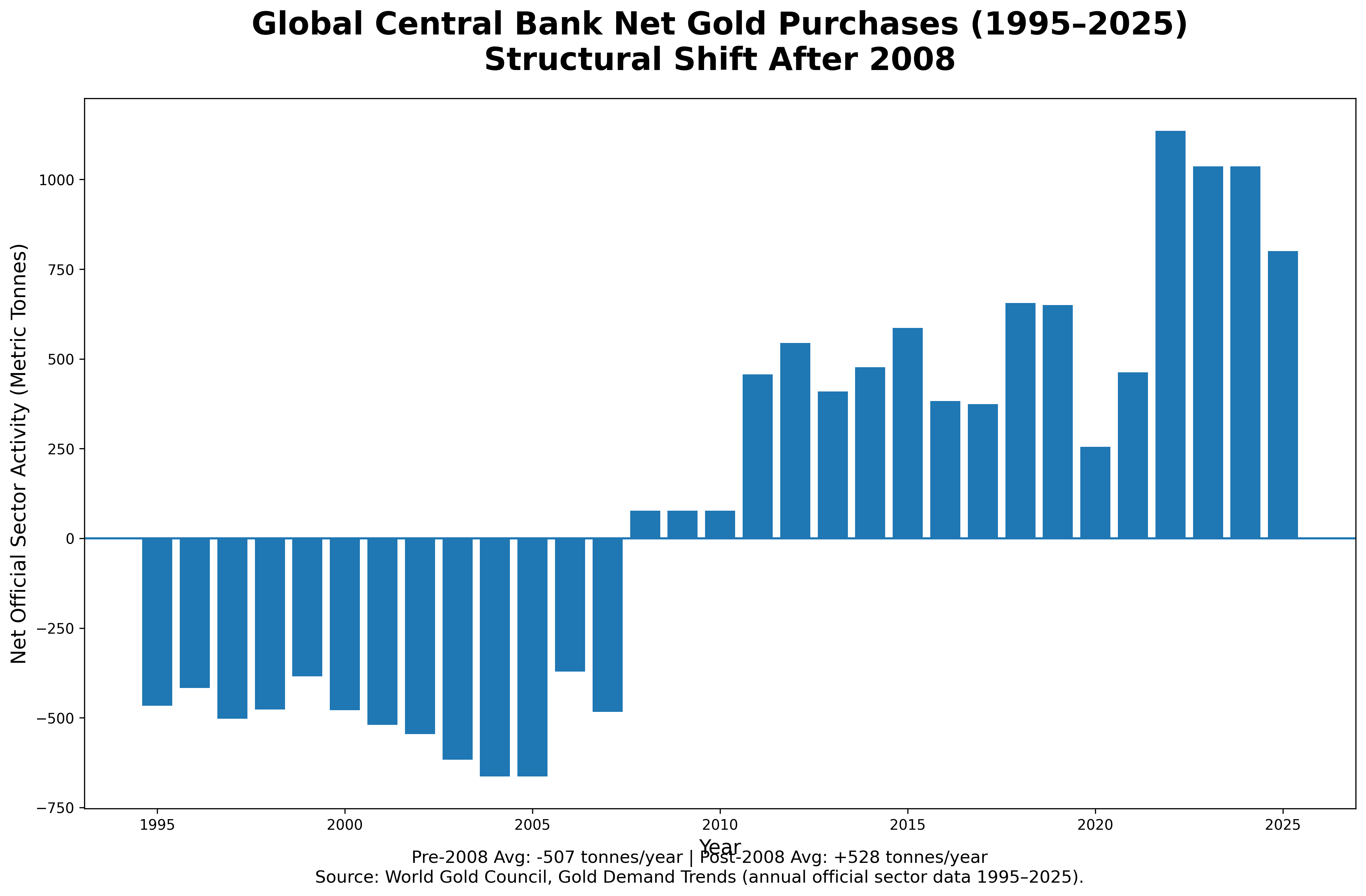

Since 2008, central banks have treated gold as a strategic reserve asset. Any reversal would carry unusual informational weight.

Investors should analyze who is selling, how they are selling, and what other macro signals accompany the move.

A Regime Shift Hiding in Plain Sight

Imagine a town selling its fire truck. Either leaders believe the neighborhood has become safer, or they urgently need cash. Central bank gold sales operate under the same logic.

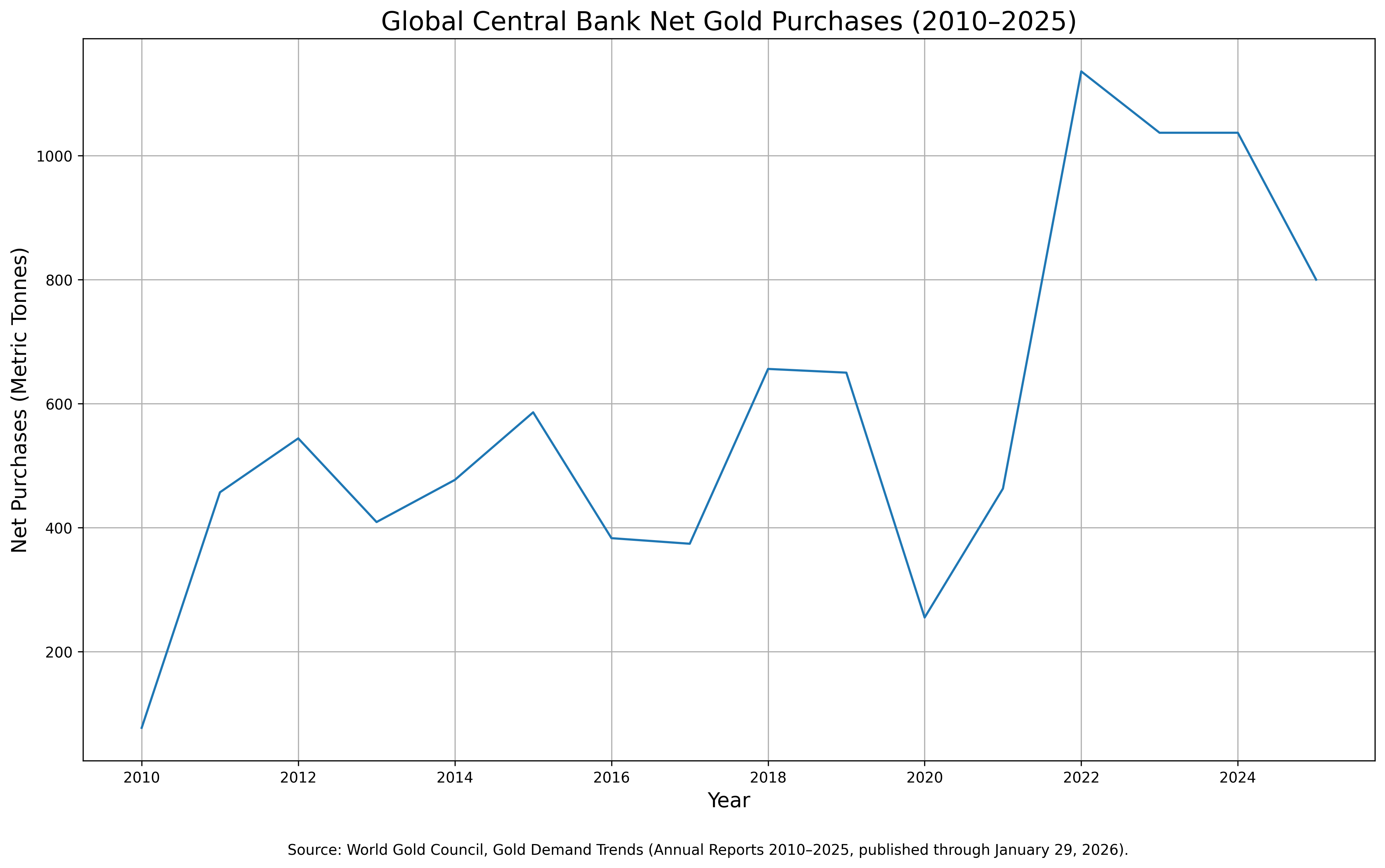

The investment thesis is straightforward: a broad, sustained turn from official net buying to official net selling would represent a regime shift. The interpretation depends on context. Gold moves not only on inflation narratives, but on trust and liquidity. Central banks sit at the center of both.¹

Gold demand has remained historically elevated in recent years. The World Gold Council reported that total demand exceeded 5,000 tonnes in 2025, with investment demand rising and central bank purchases still substantial, even after moderating from prior peaks.¹ That backdrop matters. A world in which central banks are accumulating gold sends a different macro signal than one in which they are distributing it back into the market.

Fiat currency is backed by the taxing authority of governments and the credibility of central banks, not by convertibility into metal. Trust and policy discipline do the heavy lifting. Gold occupies a peculiar place in that system. It is not anyone’s liability. Treasury bills depend on an issuer. Bank deposits depend on institutions and legal frameworks. Gold stands outside that chain.

Reserve managers consistently cite gold’s long-term store-of-value characteristics, performance during crises, and diversification properties. Surveys also point to concerns over sanctions risk and structural shifts in the international monetary system.² IMF research similarly documents the post–Global Financial Crisis rise in official gold holdings, led primarily by emerging markets.⁶

Gold is not a museum artifact in central bank vaults. It is classified as “monetary gold” when held as part of official reserves.³ It can also be mobilized through swaps and repurchase-style arrangements, allowing central banks to obtain liquidity without permanently reducing reserves.³ That distinction matters. Mobilization and outright sales send different signals.

Confidence Sales vs. Stress Sales

Not all central bank selling looks the same.

A confidence sale tends to be pre-announced, structured, and paced to avoid market disruption. It is framed as portfolio optimization rather than necessity.

The United Kingdom’s gold auctions between 1999 and 2002 illustrate this model. HM Treasury disclosed that approximately 395 tonnes were sold across 17 auctions, restructuring reserves toward foreign currency assets.⁷ The rationale emphasized liquidity and risk management. Subsequent Bank of England analysis described a transparent, rules-based auction structure aligned with prevailing market benchmarks.⁸

Switzerland offers another example. The Swiss National Bank completed sales of 1,300 tonnes by March 2005 following legal reforms that removed gold-standard constraints. The program was described as transparent and tied to excess reserve capital no longer required for monetary purposes.⁹

In both cases, officials conveyed that they could afford to sell. Gold was treated as optional insurance within a stable monetary regime.

Stress sales look different. They emerge when external financing channels narrow and hard currency liquidity becomes scarce.

India’s 1991 balance-of-payments crisis is a textbook case. Government documentation describes how gold was leased and physically shipped abroad to raise foreign exchange during acute external pressure.¹² The move was not a commentary on valuation. It was a funding decision under duress.

Modern systems add complexity. Central banks can pledge or swap gold before resorting to outright sales. The Bank for International Settlements lists gold-related services including swaps and location exchanges for central banks.¹¹ The IMF’s 2009–2010 gold sales program similarly emphasized phased, carefully managed transactions to avoid destabilizing markets.¹⁰

The key takeaway: stress often appears first as gold being mobilized, not sold. When outright sales arrive abruptly or without clear structure, markets pay attention.

The Post-2008 Pivot

Any shift toward official selling today would occur in a very different landscape than in the late 1990s.