Beat and Drop, Yield and Gold

When the best earnings report in semiconductor history cannot lift a market, what exactly is it waiting for?

Key Highlights

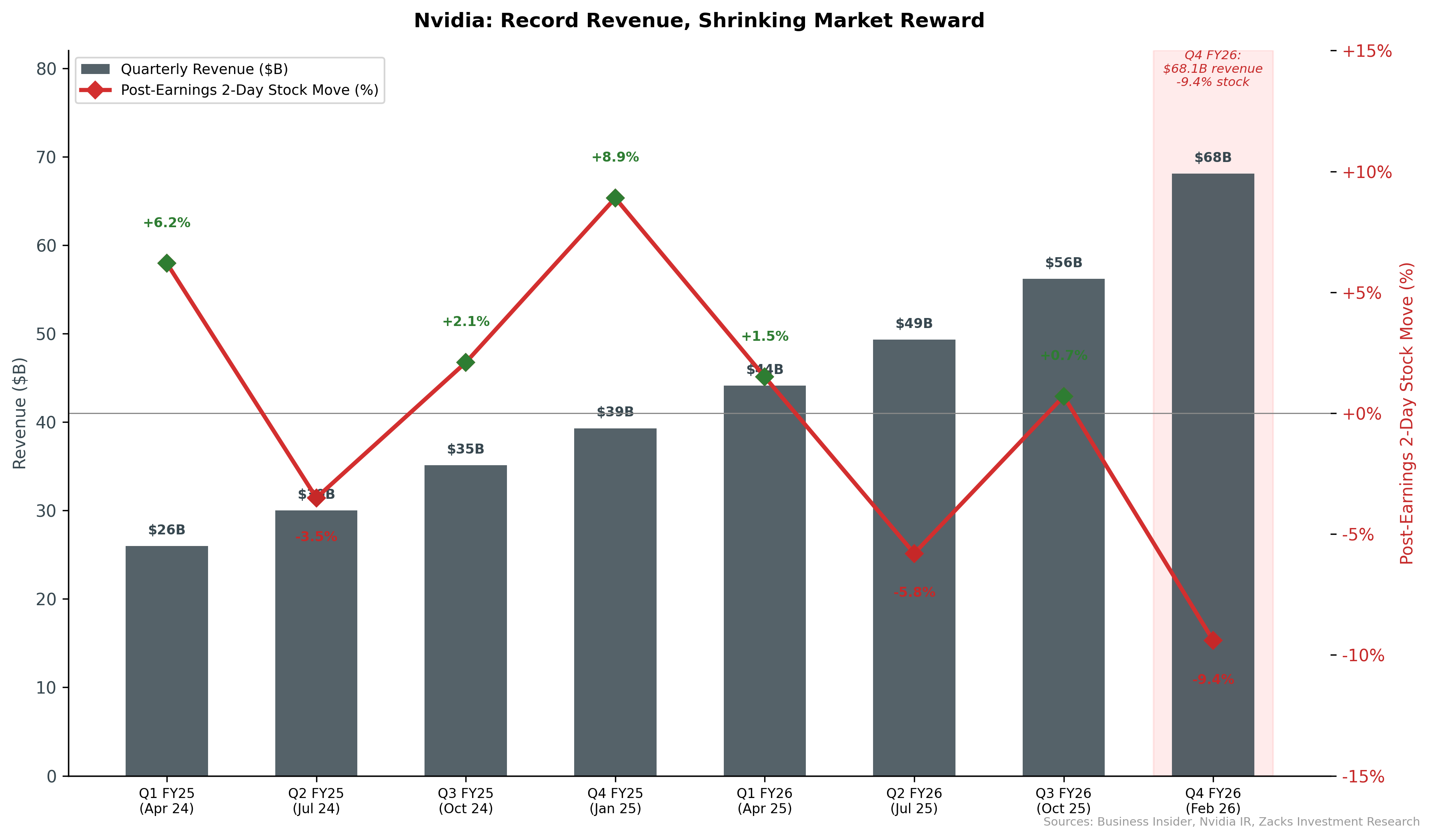

• Nvidia reported $68.1 billion in quarterly revenue, beating estimates by over $2 billion, yet shares fell 9.4% over Thursday and Friday, erasing roughly $450 billion in market capitalization.1

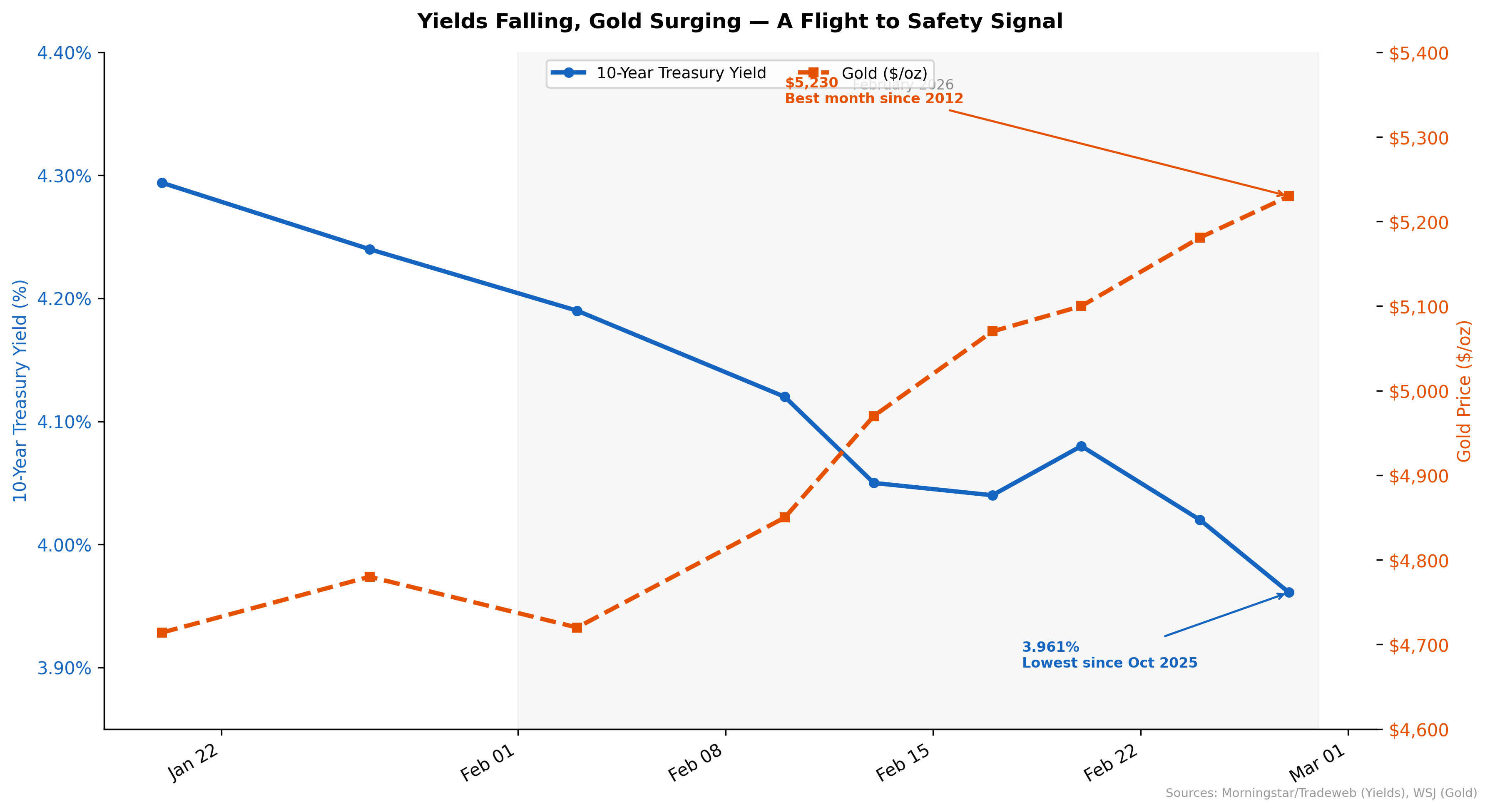

• The 10-year Treasury yield fell 12.2 basis points on the week to 3.961%, its lowest close since October 2025, while gold surged to $5,230 per ounce, its best monthly gain since January 2012.2,3

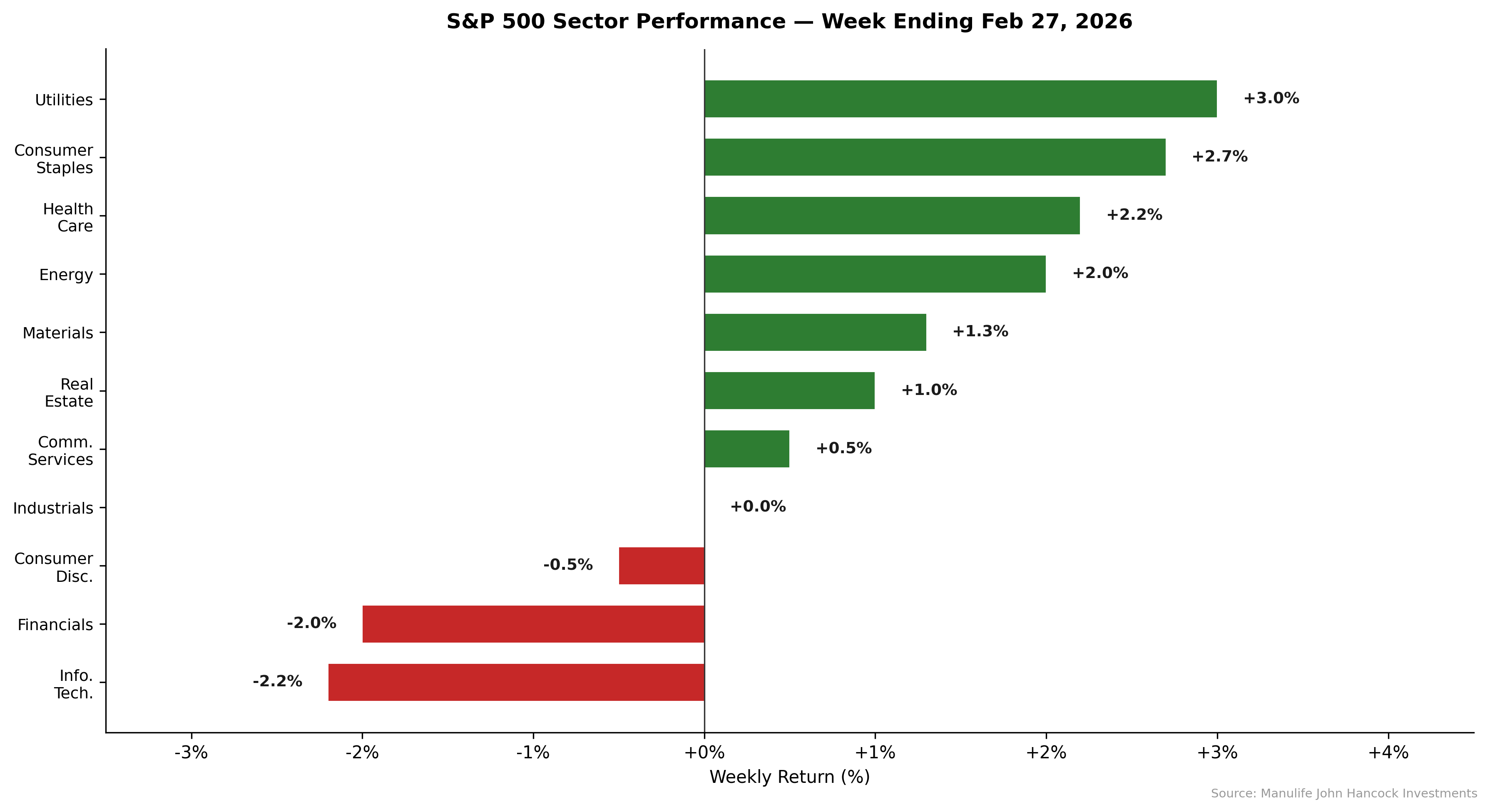

• Defensive sectors led decisively: Utilities (+3.0%), Consumer Staples (+2.7%), and Health Care (+2.2%) outperformed while Technology (-2.2%) and Financials (-2.0%) lagged, signaling a rotation beneath stable headline indices.4

• The S&P 500 finished February down 0.9%, the Nasdaq fell 3.3%, and the Dow eked out a 0.2% gain for its tenth consecutive positive month, a divergence that speaks to the narrowing of what is working and what is not.5

The Surface Narrative

On the surface, the week ending February 27 appeared manageable. The S&P 500 declined just 0.4%, a rounding error given the noise surrounding it.4 Consumer confidence ticked up modestly to 91.2, beating expectations.6 Initial jobless claims came in at 212,000, comfortably below consensus and running at levels consistent with 2023 and 2024.7 The VIX settled near 20, neither alarming nor reassuring. For index-watchers, the week was a non-event.

Yet beneath that placid surface, the cross-asset tape told a different story. The single most anticipated earnings report of the quarter produced not relief but a $450 billion drawdown. The 10-year Treasury yield slipped below 4% for the first time since October, even as the Bureau of Labor Statistics reported a producer price index that shocked to the upside.2,8 Gold finished the month up roughly 11%, its largest monthly advance in over a decade.3 Defensive sectors surged. Financials broke down. These are not the characteristics of a market digesting good news. They are the characteristics of a market that has begun to question its own assumptions.

Figure 1: Seven of eleven sectors advanced, yet the index fell. Defensives led; Technology and Financials lagged.

The Real Catalyst

The headline catalyst was Nvidia. The company delivered fiscal fourth-quarter revenue of $68.1 billion, up 73% year over year, with data center revenue of $62.3 billion surpassing estimates by nearly $2 billion. Guidance for Q1 was set at $78 billion at the midpoint, well above the $72.8 billion consensus.1 By any conventional standard, the results were exceptional. The stock rose after hours on Wednesday. By Friday’s close, it had surrendered all of those gains and then some, falling 9.4% over two sessions.

The reaction was not about the numbers. Goldman Sachs highlighted what it termed a “dislocation” between Nvidia’s earnings trajectory and its stock price, noting the challenges of perceived “over-earning” when a dominant near-term position gives way to fears about sustainability and competition.9 Deutsche Bank’s Jim Reid observed that recent earnings surprises no longer match the scale investors had internalized during the peak of the AI rally.4 The market, in other words, has begun to discount the durability of hyperscaler capital expenditure, not its current magnitude.

Figure 2: Nvidia’s revenue trajectory continues to accelerate while the market’s willingness to reward each beat is declining.

This skepticism was amplified by the week’s other defining event: Block’s announcement that it would cut approximately 4,000 employees, nearly 40% of its workforce, citing the accelerating capabilities of AI tools.10 CEO Jack Dorsey framed the decision not as distress but as structural inevitability, predicting that most companies would reach the same conclusion within a year. Block shares surged as much as 27% on the news. The implication was stark: a trade that rewards companies for eliminating workers is a trade pricing in deflation of human capital, not expansion of it. When the market cheers a 40% headcount reduction and punishes a 73% revenue beat, the underlying narrative has shifted.

Meanwhile, the bond market acted as if a different economy existed entirely. Friday’s PPI report showed wholesale prices rising 0.5% in January, with core wholesale prices excluding food and energy surging 0.8%, more than double the 0.3% consensus.8 Yet the 10-year yield fell, finishing the week at 3.961% and the month down 27.9 basis points, the largest monthly decline since February 2025.2 Bonds rallied through a hot inflation print. That is not a market ignoring data. It is a market pricing in something else entirely: the possibility that growth, not inflation, is the variable to watch.

Figure 3: The 10-year yield fell 33 basis points from its January high while gold surged over $500 in February. Falling yields alongside surging gold signal a market repricing growth risk.

Divergences Beneath the Surface

The most telling signal of the week was not found in any single index level. It was in the rotation. Seven of eleven S&P 500 sectors finished in positive territory, yet the index itself declined.4 Utilities gained 3.0%. Consumer Staples rose 2.7%. Health Care advanced 2.2%. Energy added 2.0%, supported by firmer crude amid escalating U.S.-Iran tensions. These are sectors that lead when capital seeks shelter, not when it seeks opportunity. That they outperformed while Technology fell 2.2% and Financials dropped 2.0% describes a market where breadth is improving but conviction is narrowing.

Financials deserve particular attention.