Is all that capex spending going to be rendered moot by DeepSeek? That’s the big question that Wall Street is trying to answer right now. If a Chinese startup can develop a ChatGPT-like LLM that works just as well at a fraction of the price, are the big tech giants flushing a lot of their money down the toilet? NVIDIA got hammered because it’s been not only one of the biggest spenders on AI tech, but one of the biggest beneficiaries based on the red-hot demand for its chips. If DeepSeek can build comparable models with a handful of NVIDIA’s older chips, it could potentially render a good chunk of the company’s AI development obsolete. It’s China, granted, so maybe we should take what they’re telling us about cost and such with a grain of salt, but this could be a legitimate game changer for the AI market going forward. If so, NVIDIA’s downside might not be finished.

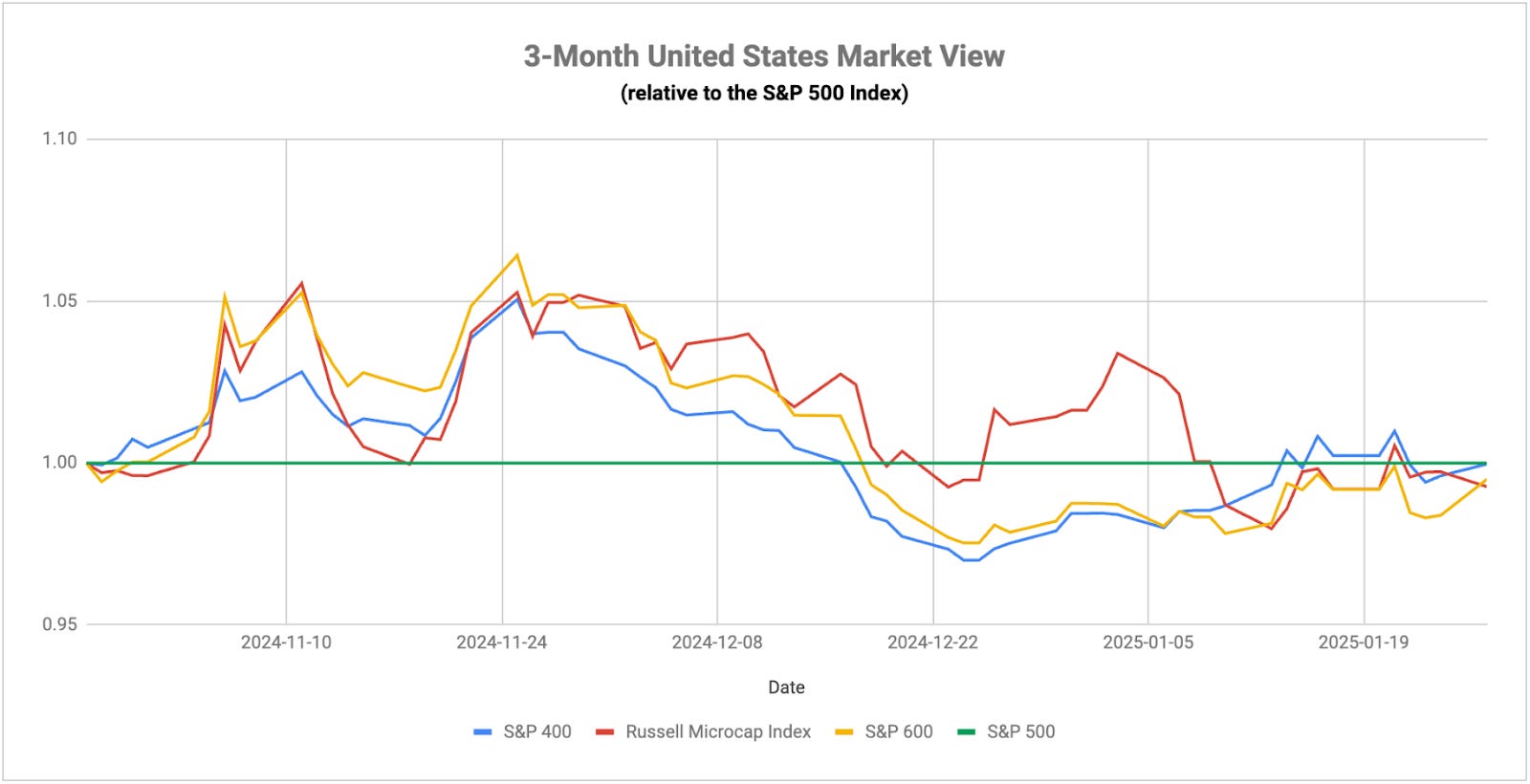

For the markets, one encouraging sign is that Monday’s action wasn’t a broad sell-off. It was a broad rotation. Even within the magnificent 7 names, Apple and Facebook were up 3% and 2%, respectively. Seven S&P 500 sectors had positive returns. Dividends, value, low volatility and long-term Treasuries all posted gains of at least 1%. Investors didn’t seem inclined to sell all equities outright. They shifted broadly into more defensive strategies. That kind of market broadening could actually be healthier long-term. A tech plunge like we saw on Monday, even one that was largely only driven by a single stock, was always a big risk in a highly concentrated market, but the damage wasn’t nearly as bad beyond tech. This has traditionally been the situation where the dip buyers show up and quickly recover what was lost. If they fail to show up this time, it could signal that sentiment has legitimately changed.

There will be a really good opportunity to see if or how the rhetoric changes this week. The Fed will meet again this week and it will be interesting to see if they take on a slightly more dovish tone in order to not spook the markets any further (we hear about their sole focus in supposed to be inflation and employment, but don’t think for a second that they’re not paying attention to the markets). The futures market is back to pricing in two full rate cuts by year-end and pulling the calendar forward where a May cut is squarely back on the table. We’ll also get earnings from Facebook, Apple and Microsoft this week. They’ve been among the biggest spenders on AI including the latter’s $80 spend commitment on data centers just a month ago. I’m sure they’ll all make passionate defenses of their capex spending plans, but the market will be watching closely for any tone of caution.

On the plus side, there are some firm signs of the manufacturing sector improving. Home sales over the past couple of months have been surprisingly strong. Manufacturing PMI moved back into expansion for the first time since June. The Philly Fed manufacturing index shot through the roof in January, although we should wait to see if that’s an aberration. Even Europe is showing signs of a pickup. This is still a services-heavy economy, but an improvement in manufacturing signals healthier business conditions and sentiment. It could mean better times ahead for non-tech stocks and even international markets.