Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Even though Treasuries have gotten bounced around quite a bit over the past few years, they remain one of the best long-term risk-off assets. When the market makes a true flight to safety shift, long-term Treasuries could be one of the best risk balancers and upside opportunities available. The “safe haven” status of Treasuries have largely been lost in the past couple years as inflation has driven the narrative and resulted in a generational bear market for bonds that crushed their ability to hedge against market volatility.

Long bonds are down slightly on the year and, save for a couple of brief periods, there hasn’t been high demand for safe haven trades. Covered call strategies, however, have been in demand. Several of the huge number of single stock covered call ETFs launched this year have become household names, but broader strategies have also garnered a lot of interest. One of the more interesting launches recently have been the iShares Treasury-based covered call ETFs, including the iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (TLTW). Up until their debut, fund issuers almost exclusively centered their covered call strategies around equities. iShares changed the game.

TLTW has been able to deliver huge yields up to this point, but total returns have been mixed. If market volatility picks up and yields start to head lower again, there could be a big return opportunity here.

Fund Background

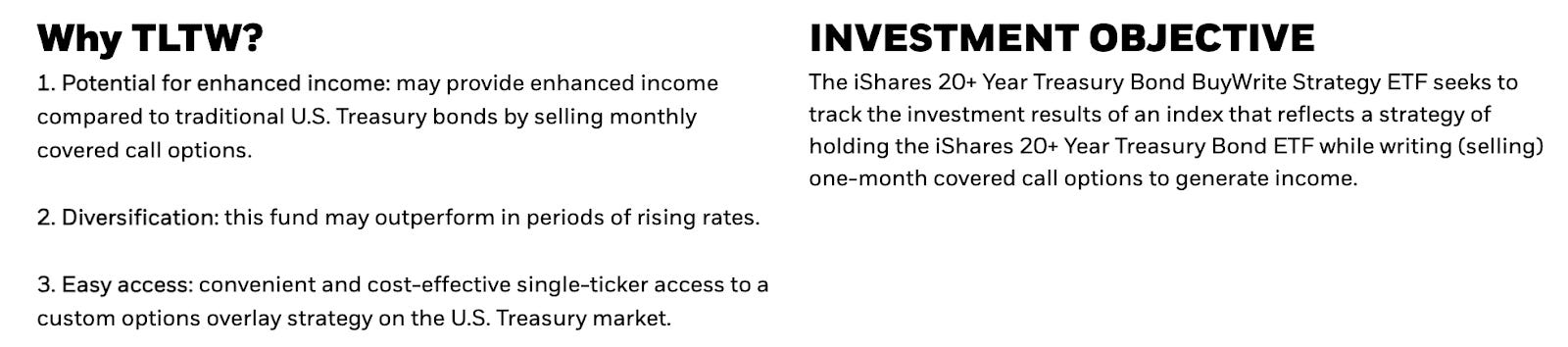

TLTW seeks to track the investment results of an index that reflects a strategy of holding the iShares 20+ Year Treasury Bond ETF while writing (selling) one-month covered call options to generate income. The index aims to use options that are approximately 2% out-of-the-money, limiting income potential somewhat but providing the opportunity for some capital growth along the way.

The primary gripe about funds using covered call strategies is that a lot of them use options that are roughly at-the-money. Those options often come with higher premiums, but it also means that capital appreciation is essentially fully capped. I prefer the 2% out-of-the-money strategy used by TLTW because it strikes a better balance, if only a modest one. Due to recent bond market volatility, TLTW isn’t having any current trouble generating income, so the flexibility that comes from using out-of-the-money options should do a little better in terms of total return potential.

What’s in the portfolio of TLTW isn’t going to be any kind of a surprise, but I’m including the graphic above to remind folks that U.S. government debt is no longer AAA-rated. It’s been downgraded or put on a negative outlook due to a combination of increasing debt loads and constant Congressional squabbles that keep threatening to shut the government down. The level of government debt is only going to continue rising at an accelerating rate and it’s probably going to surpass $40 trillion in the next 12-24 months. Don’t be surprised if we start hearing about U.S. government credit quality again.