Credit Is Calm Again — That’s Exactly When Rotation Matters (JOJO)

KEY HIGHLIGHTS

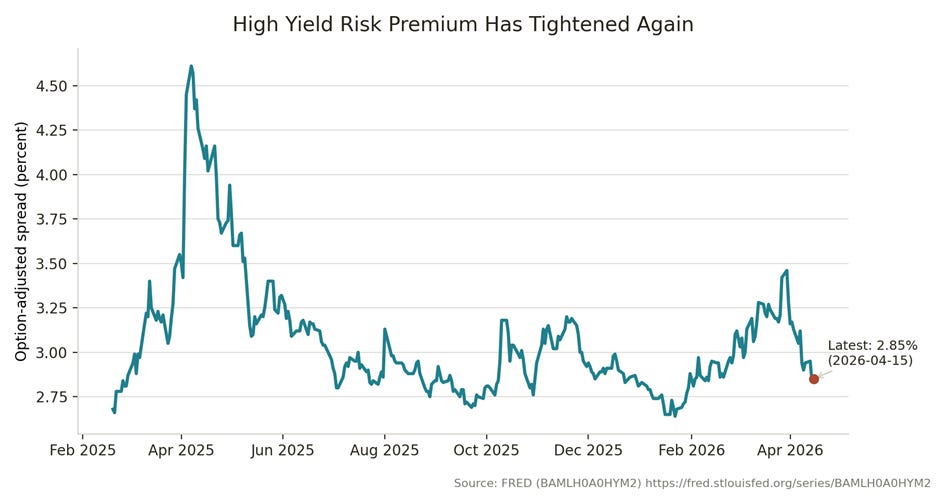

· High yield’s risk premium has compressed back toward cycle lows, with the ICE BofA US High Yield Option-Adjusted Spread at **2.85% (Apr 15, 2026)**.[1]

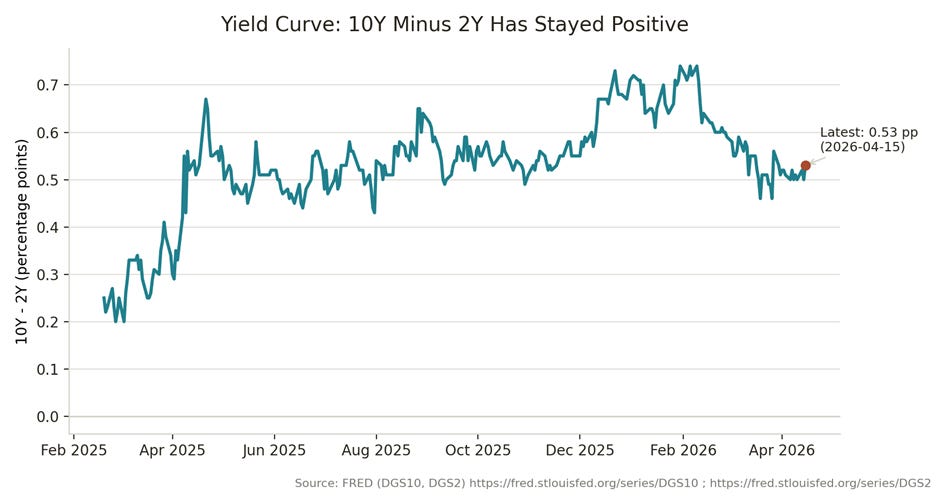

· The yield curve remains positively sloped, with the 10-year minus 2-year Treasury spread at **0.53% (Apr 15, 2026)** — a backdrop that often *looks* constructive even as credit takes on late-cycle characteristics.[2]

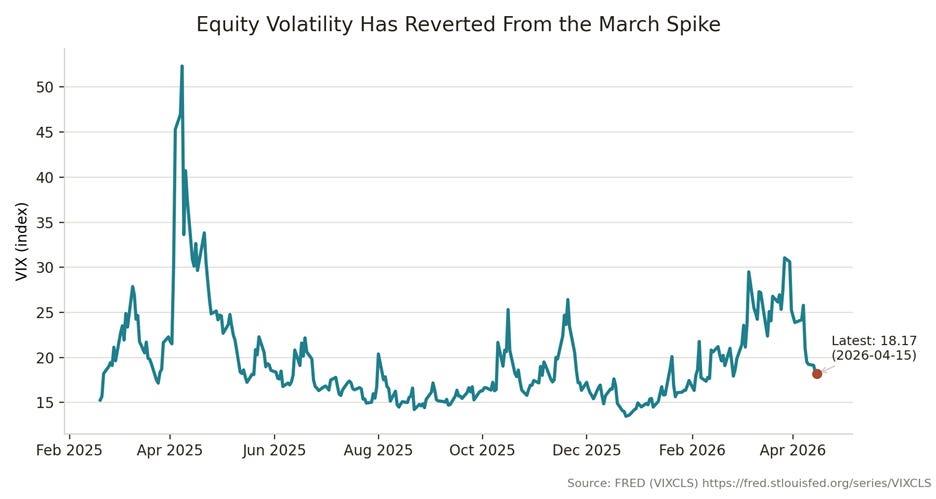

· Equity volatility has cooled, with the VIX at **18.17 (Apr 15, 2026)** after a March spike — but volatility regimes tend to change fastest when investors are most confident.[3]

· In my view, the most dangerous moments in credit are not when spreads are already wide — they’re when spreads are tight, liquidity feels abundant, and investors forget that drawdowns in high yield tend to be fast.

When credit spreads are tight and volatility has settled down, the temptation is to assume the risk is behind us. I’ve learned the hard way that this is often when risk is quietly building. The bond market rarely rings a bell at the top — it just stops compensating you for risk.

THE SETUP: A “GOOD NEWS” TAPE THAT CAN TURN QUICKLY

A compressed spread environment is not “bad” in isolation — it’s a statement about pricing. With high yield option-adjusted spreads sitting in the high-2% range,[1] investors are essentially being told that default risk and liquidity risk are manageable, and that the market expects benign conditions to persist.

That’s often true… until it isn’t.

The problem is that credit does not reprice gradually the way most investors imagine. Credit reprices through *liquidity*. When the marginal buyer steps away, the spread can move far more than fundamentals suggest, because the marketplace is not built to absorb one-way flows. High yield is, structurally, an instrument that can feel stable right up until it gaps.

This is why I focus less on whether spreads are “tight” or “wide” and more on whether the market is shifting toward a risk-off posture before spreads expand. Historically, that shift tends to show up first in equity leadership and sector behavior — particularly Utilities.

WHY THE YIELD CURVE CAN BE MISLEADING FOR CREDIT INVESTORS

A positively sloped yield curve is usually treated as a sign of improving growth expectations. And with 10s–2s around 0.5%,[2] it’s easy to tell a clean narrative: the cycle is normalizing, policy is less restrictive, and risk assets should benefit.

But the key question for credit investors is not whether the curve is positive — it’s what’s driving the slope.

If the curve steepens because the front end falls faster than the long end (often in anticipation of easier policy), risk assets can rally and spreads can compress… even while the macro outlook becomes more uncertain. That creates a fragile “Goldilocks” environment: credit looks safe because prices say it’s safe.

The irony is that the most violent credit events often occur after the market has been conditioned to believe the curve is giving it an all-clear.

VOLATILITY REGIMES: THE QUIET BEFORE THE REPRICING

The VIX is not a credit spread, but it’s a useful proxy for the market’s tolerance for uncertainty. When the VIX is in the teens (currently 18.17),[3] investors often assume that portfolio-level risk is contained.

But volatility is path-dependent. Volatility can remain low for long stretches — and then rise sharply with only modest fundamental deterioration. When that happens, it tends to coincide with widening spreads, forced deleveraging, and a sudden reduction in liquidity across risk assets.

This is why I’m skeptical of the idea that “low volatility equals low risk.” Low volatility often means risk is being warehoused somewhere else — typically in crowded positions, leverage, or assumptions about continuous liquidity.

THE UTILITIES SIGNAL: WHY I WATCH “DEFENSIVE LEADERSHIP” AS A CREDIT WARNING

Utilities are not a credit market asset, but they are a *risk appetite* asset. Utilities tend to outperform when investors prefer stability and dividend-like cash flows — a subtle shift toward defensiveness.

My core thesis — and the foundation for **ATAC Credit Rotation ETF (Ticker: JOJO)** — is that Utilities’ relative performance versus the S&P 500 has historically acted as a leading signal for rising volatility in risk assets. When Utilities begin to lead, it’s often because institutions are quietly de-risking.

And because there is a well-established relationship between equity volatility and credit spreads, that defensive turn can matter for high yield investors.

Put differently: credit spreads do not have to be widening *yet* for the environment to be deteriorating.

WHAT JOJO IS DESIGNED TO DO (AND WHAT IT IS NOT)

JOJO is not a call on interest rates. It is not a forecast that a recession is imminent. And it is not an attempt to trade every wiggle in the bond market.

Instead, JOJO is built around a single behavioral observation: when the market begins to prefer defense (as indicated by Utilities leadership), the probability of spread expansion and risk-off credit conditions rises.

So the fund rotates between high yield bond ETFs when the environment is risk-on, and long-duration Treasury ETFs when the environment is risk-off.

In a world where spreads can stay tight until they suddenly don’t, the ability to rotate away from credit risk *before* the repricing is the whole point.

THE PRACTICAL INVESTOR TAKEAWAY

If you own high yield for income, you are implicitly short volatility and long liquidity. The carry is real — but it’s also the compensation for bearing risks that can show up all at once.

With spreads near cycle lows,[1] the margin of safety is thin. That doesn’t mean “sell everything.” It means you should be honest about what you are being paid to take risk.

My view is that systematic credit rotation is a way to avoid the most common behavioral error in fixed income: staying exposed to credit risk right up until the market forces you out at the worst possible time.

I ask you to consider a simple framing: if spreads are tight and volatility is calm, the value of a risk-management process is *higher*, not lower.

Michael A. Gayed, CFA

ENDNOTES

1. Federal Reserve Bank of St. Louis, “ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2),” FRED, accessed April 17, 2026, https://fred.stlouisfed.org/series/BAMLH0A0HYM2

2. YCharts, “10-2 Year Treasury Yield Spread,” accessed April 17, 2026, https://ycharts.com/indicators/10_2_year_treasury_yield_spread

3. Federal Reserve Bank of St. Louis, “CBOE Volatility Index: VIX (VIXCLS),” FRED, accessed April 17, 2026, https://fred.stlouisfed.org/series/VIXCLS

DISCLOSURES

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the “fear gauge” of Wall Street, is a real-time market index that measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

JOJO is distributed by Foreside Fund Services, LLC.

Learn more about $JOJO at https://atacfunds.com/jojo/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.