Key Highlights

A multi-year global rearmament cycle is underway, driven by active wars, renewed great-power rivalry, and depleted military inventories.¹

Defense spending growth is increasingly structural rather than cyclical, with record budgets and long-dated procurement commitments.¹²

Market pricing remains uneven, leaving several strategically critical aerospace and defense firms trading at discounts to intrinsic value.⁶

Opportunities span the full defense stack, from legacy missile and propulsion leaders to drone warfare and rapid-development specialists.¹⁰¹¹

The primary risk for investors may be under-allocation as markets focus on short-term execution issues instead of long-duration demand visibility.¹⁸

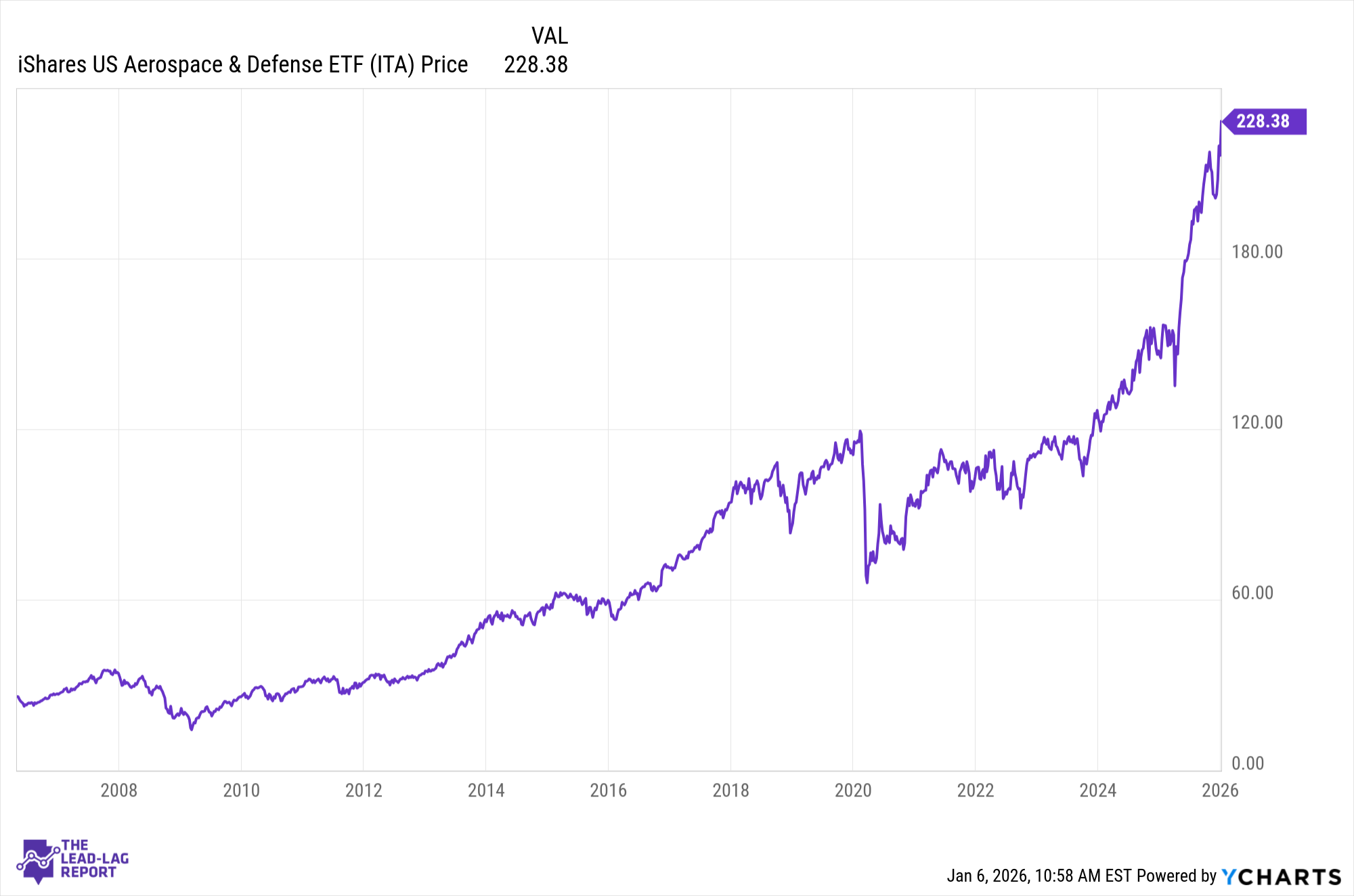

A Sector Re-Entering a Strategic Cycle

Geopolitics has entered a decisively different phase. Russia’s invasion of Ukraine, persistent conflict in the Middle East, and intensifying rivalry among major powers have accelerated a new global arms race. Military spending across NATO and allied nations is rising at its fastest pace in decades, reversing years of post–Cold War underinvestment.¹

That shift is already visible in market performance. U.S. defense equities outperformed the broader market in 2025, with smaller, technology-focused firms often leading gains.² The divergence reflects more than investor enthusiasm; it signals a change in how wars are fought and how militaries procure equipment. Unmanned systems, loitering munitions, missile defense, and networked command platforms have moved from experimental concepts to battlefield necessities.¹³

The U.S. fiscal-year 2026 defense budget request underscored this transition, directing a disproportionate share of incremental funding toward drones, counter-drone systems, and advanced missiles while deemphasizing traditional platforms.² This reallocation has also exposed weaknesses in the defense industrial base, prompting renewed emphasis on domestic production capacity and supply-chain security.⁷

Against this backdrop, several aerospace and defense stocks remain mispriced relative to their strategic relevance and long-term earnings power.

RTX Corporation (RTX): Scale Meets Strategic Demand

RTX occupies a central role in modern defense, supplying missile defense systems, propulsion platforms, sensors, and avionics that are actively deployed in ongoing conflicts. The company entered 2025 with a record backlog exceeding $200 billion, driven by strong international demand and expanding NATO defense budgets.⁴

Despite this momentum, RTX’s valuation continues to reflect investor caution tied to manufacturing issues at its Pratt & Whitney commercial aerospace unit. Those issues triggered significant share-price weakness when first disclosed and have lingered in market psychology.⁵ The problem, however, is largely orthogonal to RTX’s defense franchises, which remain aligned with the fastest-growing areas of Pentagon and allied spending.

From a contrarian perspective, this disconnect matters. Missile defense, advanced propulsion, and integrated air-and-missile systems are core U.S. priorities, and RTX’s scale and installed base create durable competitive advantages. Morningstar continues to estimate that RTX trades at a material discount to fair value, suggesting that near-term concerns are overshadowing long-term fundamentals.⁶

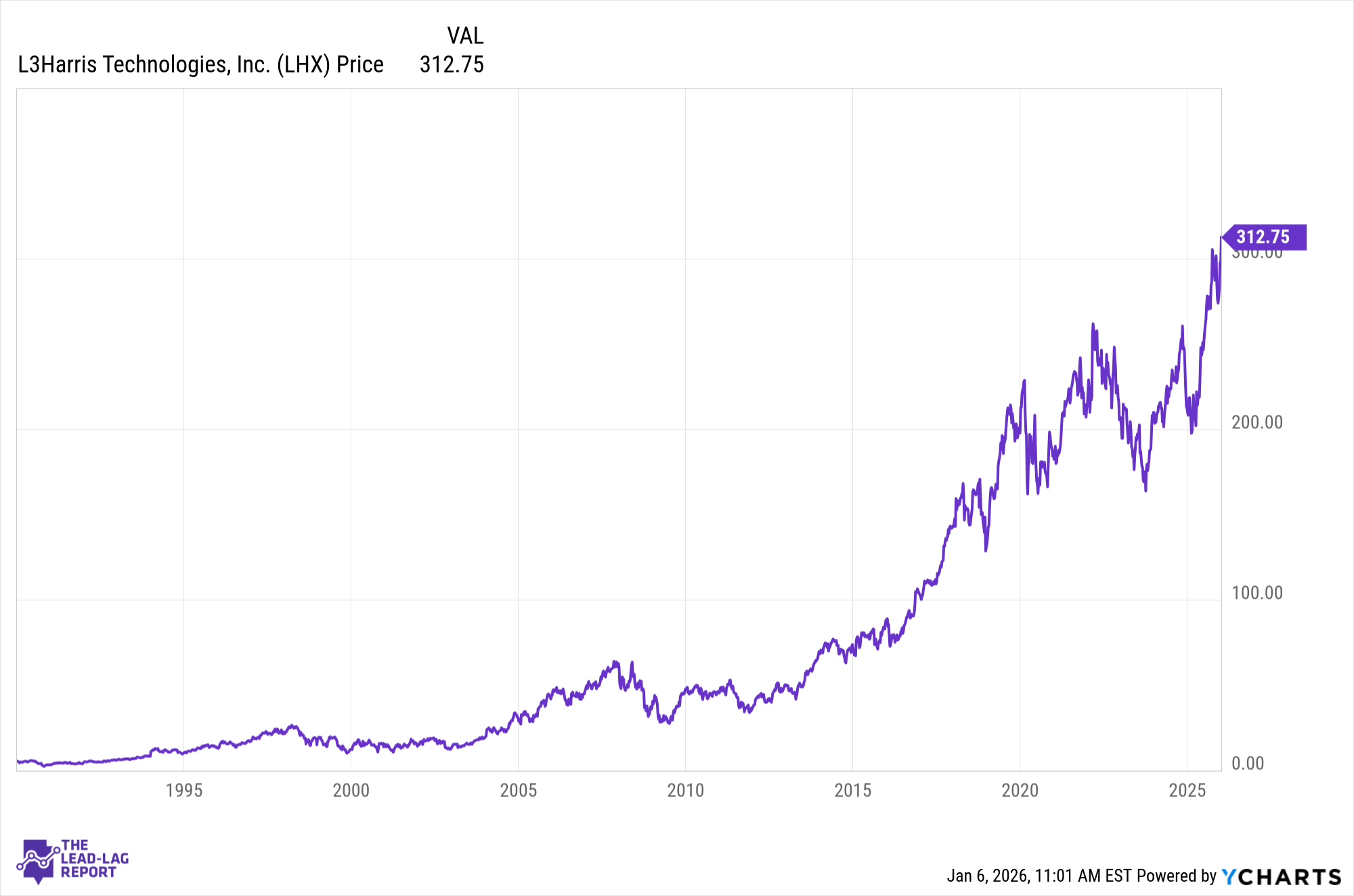

L3Harris Technologies (LHX): Infrastructure for Modern Warfare

L3Harris has quietly repositioned itself as a backbone provider for modern military operations. Through targeted acquisitions and internal investment, the company now spans secure communications, missile propulsion, space-based sensing, and classified defense programs.⁷

The acquisition of Aerojet Rocketdyne proved particularly strategic, securing a critical chokepoint in U.S. missile production at a time when demand for munitions and hypersonic systems is accelerating. Production capacity has expanded meaningfully, and new facilities are coming online to support long-dated contracts.⁷

Despite this progress, L3Harris continues to trade below intrinsic value estimates.⁶ The market appears to be discounting integration complexity while underestimating the durability of demand tied to space defense, missile modernization, and secure communications. For contrarian investors, L3Harris offers exposure to the infrastructure layer of modern warfare rather than headline weapons systems.