On Wednesday, the Fed will announce its latest policy rate decision, which will almost certainly involve a quarter-point cut. The more interesting thing to watch will be what they say about 2025. The market is still pricing in 2-3 rate cuts next year, but Powell has also been very cognizant of inflation risk. With inflation moving higher again and the possibility of Trump tariffs throwing gas on the fire, I think it’s reasonable to think that the Fed will take a hawkish approach so as to try to avoid a 2nd inflation wave like the one the economy experienced in the stagflation 1970s.

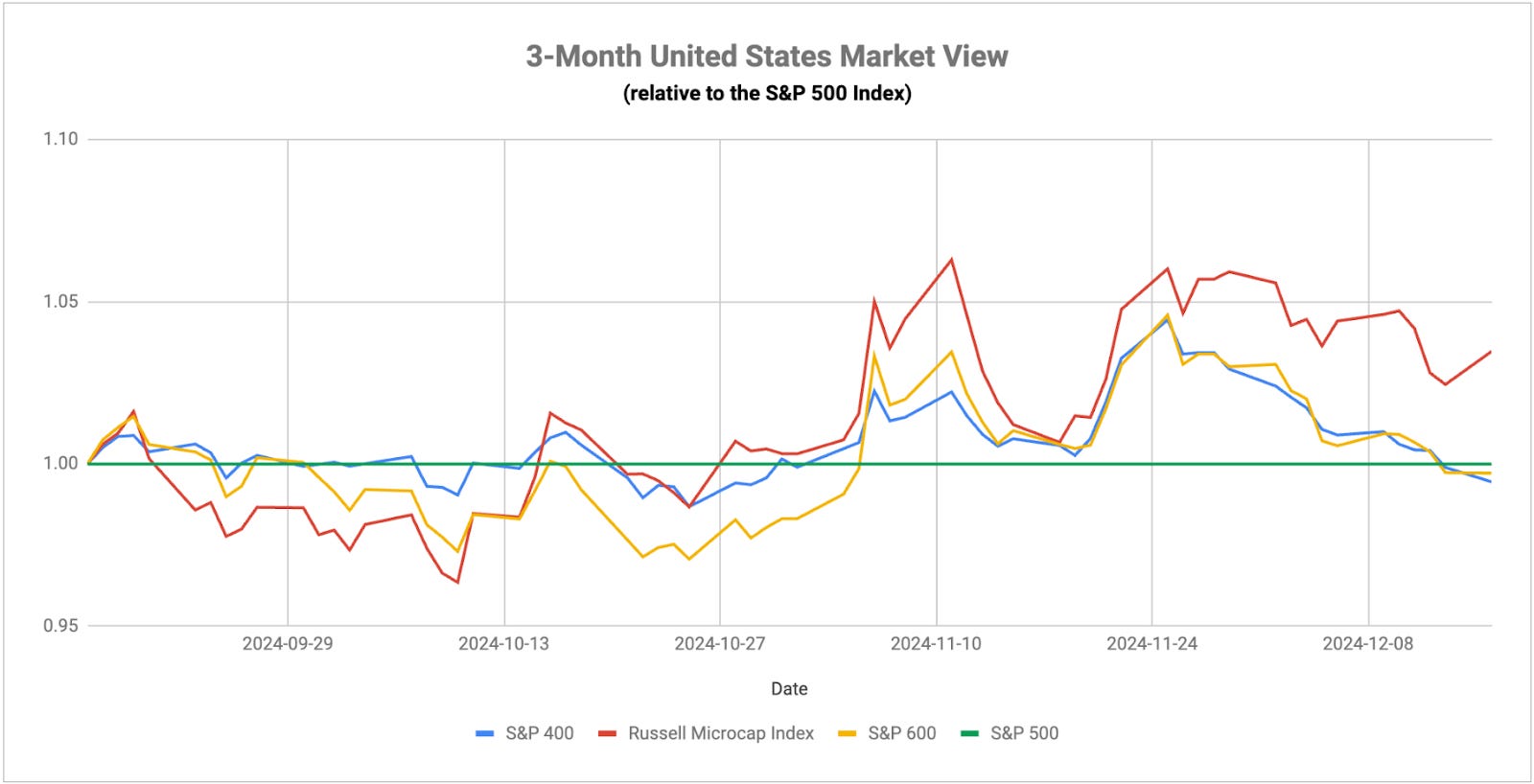

As it stands right now, the U.S. equity market looks like it’s set for a low risk ride into the new year, but the Bank of Japan rate decision this week could be the wild card that upends it. Over the past 2-3 weeks, however, low volatility hasn’t meant further gains for stocks. This has been another magnificent 7 driven rally that’s left most other groups behind. This group collectively is up more than 10% and that’s helped lift the Nasdaq 100 to a 5% for December thus far. That’s helped the S&P 500 stay flat, but the equal weight version of the index and small-caps are both down about 4%. Utilities are down 7%. The mag 7 has emerged almost as a safety valve for when investors want to exercise some degree of caution, but don’t want to rotate all the way into defensive sectors. The inflation problem still looms, but economic growth and the labor market still look healthy, so investors may be leaning towards mega-cap tech as almost a hedge. This trend could continue into the first part of next year as these two forces compete.

While the soft landing in the U.S. appears to be intact for now, the question for 2025 becomes whether earnings growth can continue to reaccelerate off of its recent trough and extend the soft landing bounce or if rising inflation turns growth into stagnation. These are typically slow boats to turn and it’s unlikely we’d see any meaningful changes to the economic cycle until at least the 2nd half of the year. Domestic stocks seem to have gotten used to the idea of a 3% inflation rate even if the economy can’t get back to the Fed’s 2% target. The bond market, however, continues to display a level of uncertainty. The bond rally this summer was predicated on the idea that inflation was still moderating and the Fed would be able to accelerate its pace of rate cuts. Since the September low, the 10-year yield is now higher by 80 basis points as inflation risk and a lack of Fed action gets baked back in. That and the resilience of gold prices suggest that there is a level of trepidation still present in certain areas of the market.

I’ve had the December Bank of Japan policy meeting at the top of my list of things to watch for weeks and we’re finally here. Right now, the market has priced in a roughly 1-in-3 chance of a rate hike this week, which qualifies a potential move as unlikely but certainly possible. The market seems to believe that the central bank will hold for another meeting, but signal its next cut for sometime in Q1. The decision may come down to which factor - slowing growth or rising inflation - they prioritize more and whether they see urgency on either front. On the economic side, Japanese wage growth is easing, consumption has slowed and the possibility of tougher global trade conditions all favor a pause. On the other hand, inflation is starting to creep uncomfortably above where the BoJ would like it, while global trends and the possibility of tariffs would likely make the situation even worse. If the central bank sees the economy as losing control of rising price pressures, they could opt to hike sooner than later. If they take a “it’s still OK for now” view, it strengthens the case for giving it another month or two to get a little more data.