$FMKT: Why Investors Should Treat Deregulation as a Structural Trend, Not a Fad

Key Highlights

Deregulation is re-emerging as a structural policy shift, driven by court rulings, executive action, and economic conditions rather than short-term political cycles.

A 2024 Supreme Court decision limiting regulatory authority has fundamentally reshaped the balance of power between federal agencies and the judiciary.

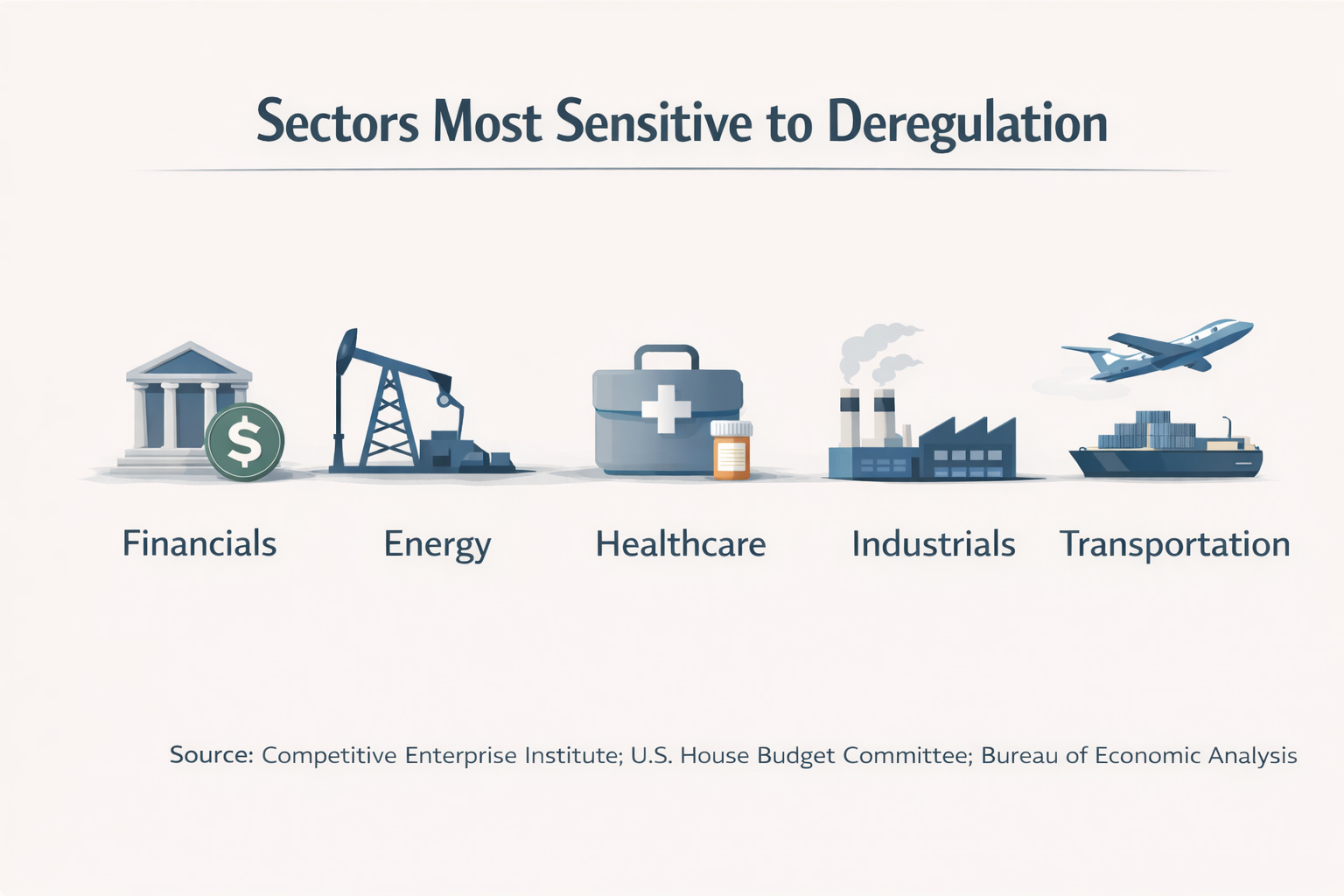

Industries with historically high compliance costs such as financials, energy, healthcare, and industrials may benefit disproportionately from sustained regulatory relief.

Policymakers increasingly view deregulation as a non-inflationary growth lever, particularly as inflation pressures moderated in 2025.

FMKT (Free Markets ETF) reflects this backdrop by seeking exposure to U.S. companies believed to benefit from a lighter regulatory environment, treating deregulation as an investable theme rather than a passing narrative.

Few phrases generate more frustration in the business world than “red tape.” For many companies, regulatory compliance represents a persistent drain on time, capital, and productivity. That tension was put on public display in 2017, when policymakers staged a White House event featuring towering stacks of paper symbolizing the growth of federal regulations over time. The moment was theatrical, but the underlying message resonated: regulation had expanded significantly, and pressure was building to reverse course.

Several years later, deregulation has returned to the center of economic policy discussions, not as symbolism, but as a deliberate strategy. After a prolonged period of crisis-driven rulemaking, the policy pendulum has begun to swing back. What distinguishes the current environment is the growing perception that this shift is structural rather than cyclical. Across Washington and financial markets, deregulation is increasingly viewed as a long-term force with implications for economic growth, corporate profitability, and asset allocation.

Policy Signals Point to a Durable Shift

The renewed momentum behind deregulation has been driven by concrete institutional changes rather than rhetoric alone. A pivotal moment came in June 2024, when the U.S. Supreme Court overturned the Chevron doctrine, a longstanding precedent that had granted federal agencies broad discretion in interpreting congressional statutes. By curtailing that authority, the Court fundamentally altered how regulations are likely to be written and challenged going forward. The ruling signaled that expansive rulemaking would face greater judicial scrutiny, reshaping the regulatory landscape in a lasting way.

Political developments soon reinforced that legal shift. In early 2025, a new administration entered office with an explicit mandate to reduce regulatory burdens. One of its first executive actions instructed federal agencies to eliminate ten existing regulations for every new rule introduced. Framed as an effort to stimulate growth by removing bureaucratic friction, the order represented one of the most aggressive rollback initiatives in modern regulatory history.¹

What initially appeared to some observers as political theater began to translate into tangible policy changes. By late 2025, multiple federal agencies had slowed the pace of new rulemaking and launched reviews aimed at simplifying compliance frameworks. These efforts extended across financial services, infrastructure development, labor markets, and energy production.²³ Rather than fading after the initial announcement, the deregulatory push broadened in scope.

The energy sector illustrates this trend clearly. In late 2025, federal officials moved to reverse prior restrictions on oil and gas leasing in Alaska, citing the need to unlock domestic production and reduce regulatory barriers. Similar reasoning supported efforts to streamline environmental permitting for infrastructure projects and revisit labor classifications in the gig economy. The consistent message was that market forces should play a larger role in allocating capital and labor.

Economic conditions have also played an important role. As inflation pressures eased in 2025 following an extended tightening cycle, policymakers sought growth-oriented strategies that would not risk reigniting price instability. Deregulation re-emerged as a favored tool. Unlike fiscal stimulus or aggressive rate cuts, regulatory relief does not require new public spending and is often framed as a supply-side reform.⁴⁵⁶

Importantly, deregulation is not confined to one political ideology. History shows that both parties have embraced it at different moments, from airline deregulation in the late 1970s to telecommunications reform in the 1980s. What makes the current phase distinctive is its breadth and the degree to which it challenges the legal foundations of the modern regulatory state. For investors, this raises the possibility that regulatory conditions across multiple industries may be structurally different in the years ahead.

Economic Tailwinds and Sector Implications

Regulatory compliance functions as an implicit cost on economic activity. Estimates suggest that federal regulations impose more than $2 trillion in annual costs on U.S. businesses and consumers, an amount equivalent to a meaningful share of national output. Even incremental reductions in this burden can influence margins, investment decisions, and productivity.

The benefits of deregulation, however, are not evenly distributed. Industries with historically high compliance costs stand to gain the most. Financial institutions remain a prominent example. Since the global financial crisis, banks have operated under stringent capital requirements, stress testing regimes, and reporting obligations. Adjustments to these frameworks could reduce operating costs and expand lending capacity, particularly for regional banks.

Energy producers face a different but equally consequential regulatory environment. Lengthy permitting processes and environmental reviews often delay projects and raise development costs. Faster approvals and greater access to federal lands can materially alter investment timelines and cash flow dynamics. Healthcare companies encounter similar challenges. Drug developers and medical device manufacturers navigate complex approval pathways that can stretch over many years. Streamlining those processes may bring products to market sooner while reducing development expenses.

Manufacturing, transportation, and industrial firms also operate under dense regulatory frameworks covering emissions, labor practices, and workplace safety. Modest regulatory relief in these areas can translate directly into improved efficiency and competitiveness. On a global scale, lighter domestic regulation may enhance the relative position of U.S. companies competing with peers in more heavily regulated jurisdictions.

Market sentiment has begun to reflect these dynamics. Business confidence indicators have improved in sectors where regulatory rollbacks have been announced, suggesting that executives are incorporating expectations of a more favorable policy environment into strategic planning. Still, deregulation is not without trade-offs. Reduced oversight can introduce uncertainty and, in some cases, elevate risks that regulations were designed to mitigate. The broader point is that deregulation represents a multi-year macro theme rather than a narrow sector story.

Investing in a Freer Market Environment

For investors, the return of deregulation introduces a new analytical lens. Beyond interest rates and earnings trends, regulatory trajectories are increasingly shaping how opportunities are evaluated. Companies with historically high compliance costs may experience disproportionate benefits if those burdens ease.

This perspective has begun to influence product design. In mid-2025, the Free Markets ETF (FMKT) launched with the explicit objective of capturing potential beneficiaries of a lighter regulatory regime. The actively managed fund draws from across the U.S. equity market, targeting firms in sectors such as financials, energy, healthcare, and technology where deregulation could materially affect business outcomes. Its approach reflects the view that regulatory policy itself has become an investable factor.

Whether accessed through a dedicated vehicle or incorporated into broader portfolio construction, deregulation is increasingly part of the investment conversation. Investors may view it as a tailwind when assessing sector allocations or individual companies, particularly those constrained by regulatory complexity in prior years.

At the same time, caution remains warranted. Regulatory cycles can reverse, legal challenges can delay implementation, and reduced oversight can expose firms to operational or reputational risks. A change in political leadership or a major economic shock could slow or halt the deregulatory momentum. As with any thematic strategy, diversification and disciplined analysis remain essential.

Conclusion

Deregulation’s resurgence is neither accidental nor superficial. Legal rulings, executive actions, and economic conditions have converged to position regulatory restraint as a long-term policy tool rather than a short-lived initiative. For investors, this represents both opportunity and responsibility. The potential for lower costs and improved efficiency is real, but so are the risks associated with policy uncertainty and reduced safeguards.

Treating deregulation as a structural trend acknowledges its growing influence on markets while avoiding the assumption that fewer rules guarantee better outcomes. In an environment where policy shifts increasingly shape investment landscapes, recognizing the durability of deregulation may prove as important as recognizing its limits.⁵⁶

Footnotes

Reuters, “U.S. Administration Orders Agencies to Cut Regulations,” January 23, 2025.

U.S. House Budget Committee, Regulatory Reform and Economic Growth, October 12, 2025.

Lead-Lag Report, “How Deregulation Is Re-Entering the Policy Toolkit,” December 4, 2025.

Reuters, “Inflation Pressures Ease as Growth Concerns Rise,” September 18, 2025.

Competitive Enterprise Institute, Deregulation and Long-Term Economic Output, August 7, 2025.

Businesswire, “Market Implications of Regulatory Rollbacks,” November 15, 2025.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-994-4004 or visiting www.freemarketsetf.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

FMKT is distributed by Foreside Fund Services, LLC.

Find full holding details and learn more about FMKT at

http://www.freemarketsetf.com.

Holdings are subject to change.

Deregulation Strategy Risks.The Fund’s strategy of investing in companies that may benefit from deregulatory measures entails significant risks, including those stemming from the unpredictable nature of regulatory trends. Deregulation is influenced by political, economic, and social factors, which can shift rapidly and in unforeseen directions. Changes in government priorities, political leadership, or public sentiment may result in the reversal of existing deregulatory policies or the introduction of new regulations that could adversely affect certain industries or companies. Further, while the Fund invests in companies expected to benefit from deregulatory initiatives, not all of these companies may achieve the expected advantages, whether fully, partially, or at all. The actual impact of deregulatory measures may vary widely depending on a company’s specific operational, financial, and competitive circumstances. Companies may also face challenges adapting to new regulatory environments, or their competitive positioning may be undermined by other market factors unrelated to deregulation. These risks could negatively affect the performance of the Fund’s portfolio.

Underlying Digital Assets ETP Risks. The Fund’s investment strategy, involving indirect exposure to Bitcoin, Ether, or any other Digital Assets through one or more Underlying ETPs, is subject to the risks associated with these Digital Assets and their markets. These risks include market volatility, regulatory changes, technological uncertainties, and potential financial losses. As with all investments, there is no assurance of profit, and investors should be cognizant of these specific risks associated with digital asset markets.

● Underlying Bitcoin and Ether ETP Risks: Investing in an Underlying ETP that focuses on Bitcoin, Ether, and/or other Digital Assets, either through direct holdings or indirectly via derivatives like futures contracts, carries significant risks. These include high market volatility influenced by technological advancements, regulatory changes, and broader economic factors. For derivatives, liquidity risks and counterparty risks are substantial. Managing futures contracts tied to either asset may affect an Underlying ETP’s performance. Each Underlying ETP, and consequently the Fund, depends on blockchain technologies that present unique technological and cybersecurity risks, along with custodial challenges in securely storing digital assets. The evolving regulatory landscape further complicates compliance and valuation efforts. Additionally, risks related to market concentration, network issues, and operational complexities in managing Digital Assets can lead to losses. For Ether specifically, risks associated with its transition to a proof-of-stake consensus mechanism, including network upgrades and validator centralization, may add additional uncertainties.

●Bitcoin and Ether Investment Risk: The Fund’s indirect investments in Bitcoin and Ether through holdings in one or more Underlying ETPs expose it to the unique risks of these digital assets. Bitcoin’s price is highly volatile, driven by fluctuating network adoption, acceptance levels, and usage trends. Ether faces similar volatility, compounded by its reliance on decentralized applications (dApps) and smart contract usage, which are subject to innovation cycles and adoption rates. Neither asset operates as legal tender or within central authority systems, exposing them to potential government restrictions. Regulatory actions in various jurisdictions could negatively impact their market values. Both Bitcoin and Ether are susceptible to fraud, theft, market manipulation, and security breaches at trading platforms. Large holders of these assets (”whales”) can influence their prices significantly. Forks in the blockchain networks—such as Ethereum’s earlier split into Ether Classic—can affect demand and performance. Both assets’ prices can be influenced by speculative trading, unrelated to fundamental utility or adoption.

● Digital Assets Risk: Digital Assets like Bitcoin and Ether, designed as mediums of exchange or for utility purposes, are an emerging asset class. Operating independently of any central authority or government backing, they face extreme price volatility and regulatory scrutiny. Trading platforms for Digital Assets remain largely unregulated and prone to fraud and operational failures compared to traditional exchanges. Platform shutdowns, whether due to fraud, technical issues, or security breaches, can significantly impact prices and market stability.

● Digital Asset Markets Risk: The Digital Asset market, particularly for Bitcoin and Ether, has experienced considerable volatility, leading to market disruptions and erosion of confidence among participants. Negative publicity surrounding these disruptions could adversely affect the Fund’s reputation and share trading prices. Ongoing market turbulence could significantly impact the Fund’s value.

● Blockchain Technology Risk: Blockchain technology underpins Bitcoin, Ether, and other digital assets, yet it remains a relatively new and largely untested innovation. Competing platforms, changes in adoption rates, and technological advancements in blockchain infrastructure can affect their functionality and relevance. For Ether, the dependence on its proof-of-stake mechanism and smart contract capabilities introduces risks tied to network performance and scalability. Investments in blockchain-dependent companies or vehicles may experience market volatility and lower trading volumes. Furthermore, regulatory changes, cybersecurity incidents, and intellectual property disputes could undermine the adoption and stability of blockchain technologies.

Recent Market Events Risk. U.S. and international markets have experienced and may continue to experience significant periods of volatility in recent years and months due to a number of economic, political and global macro factors including uncertainty regarding inflation and central banks’ interest rate changes, the possibility of a national or global recession, trade tensions and tariffs, political events, war and geopolitical conflict. These developments, as well as other events, could result in further market volatility and negatively affect financial asset prices, the liquidity of certain securities and the normal operations of securities exchanges and other markets, despite government efforts to address market disruptions.

New Fund Risk. The Fund is a recently organized management investment company with no operating history. As a result, prospective investors do not have a track record or history on which to base their investment decisions.

. Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso, Tactical Rotation Management, LLC, SYKON Asset Management, Point Bridge Capital, or ACA/Foreside.