Key Highlights

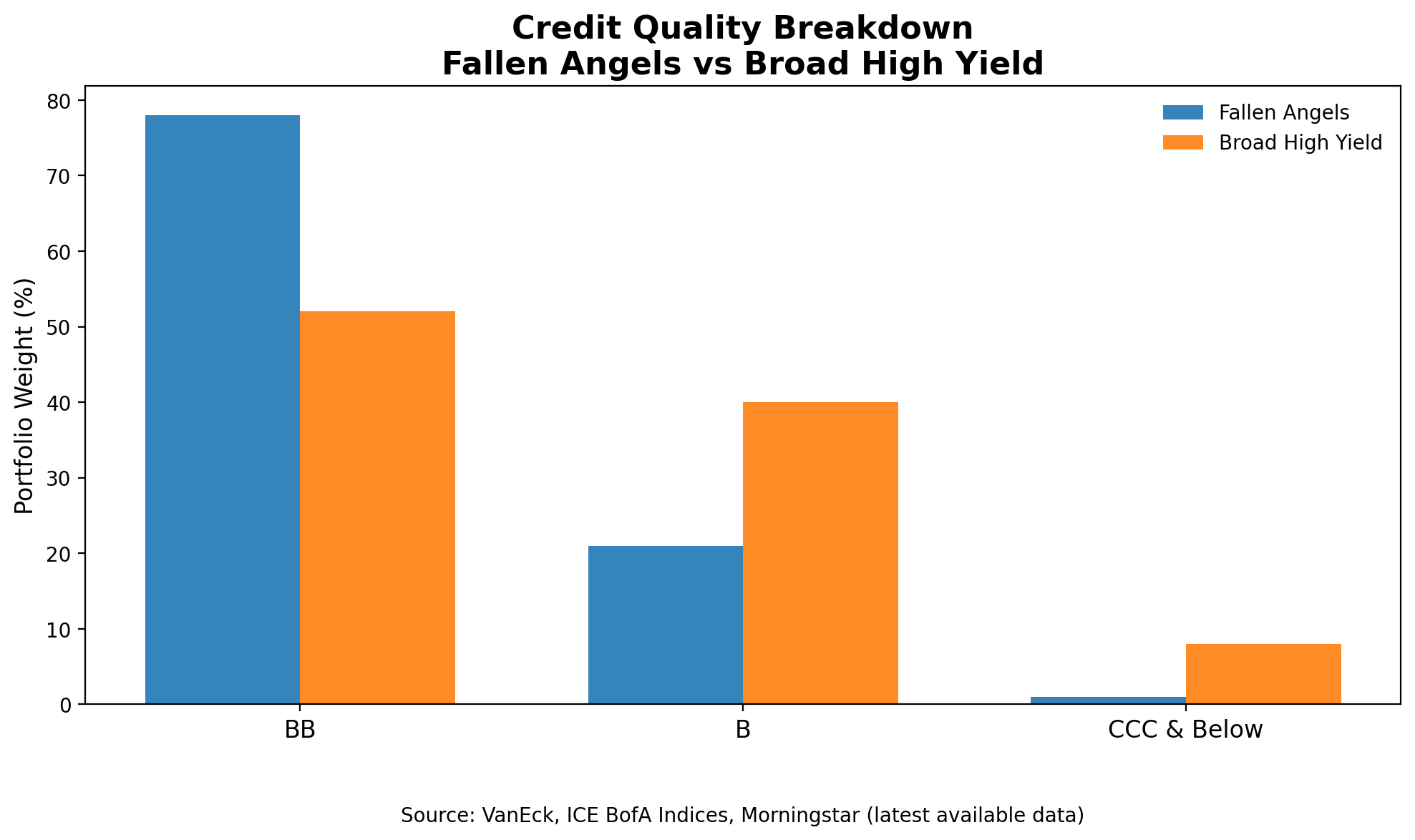

Fallen angels occupy the highest tier of the high-yield market, with roughly three-quarters of the portfolio concentrated in BB-rated bonds, materially reducing exposure to the most speculative segments of junk credit.

Higher quality has not meant lower returns. Over full market cycles, fallen-angel strategies have delivered stronger cumulative total returns than broad high-yield benchmarks, driven by fewer default losses and recovery-driven price appreciation.

Drawdowns still occur, but the source of risk is different. Fallen angels tend to experience stress during liquidity shocks and rapid rate hikes, not because of widespread credit failures but due to greater interest-rate sensitivity.

Yield is competitive, not maximal. Current income sits modestly below the broad high-yield market, reflecting a deliberate trade-off: slightly less yield in exchange for higher credit quality and more stable issuers.

Duration, not defaults, is the primary risk factor. Compared with lower-quality junk, fallen angels carry longer duration, making them more responsive to changes in Treasury yields while remaining structurally insulated from the riskiest credit tail events.

Investor demand for income remains elevated as yields sit near multi-year highs. After widening sharply during the 2022 rate shock, high-yield spreads peaked near 450 basis points amid late-2024 recession fears before tightening again as growth proved resilient.¹ Defaults have remained contained, with recent rates hovering near historical averages and forward estimates still consistent with a “soft landing” scenario rather than a deep downturn.²

At the same time, interest-rate risk has reasserted itself as a dominant driver of bond performance. The drawdowns in high-yield ETFs during 2022 occurred despite limited credit stress, underscoring how sensitive fixed income remains to policy tightening.³ As inflation moderates and markets look ahead to eventual Fed easing, investors are increasingly focused on how to generate income without taking on excessive late-cycle credit risk.

This environment has renewed interest in fallen angels—a segment of the high-yield market that sits at the intersection of yield, quality, and potential recovery.

Fallen Angels Explained: The Case for Quality Within High Yield

The VanEck Fallen Angel High Yield Bond ETF (ANGL) offers exposure exclusively to bonds that were originally issued with investment-grade ratings but later downgraded to high yield.⁴ Unlike traditional junk bonds, these securities come from issuers that previously met higher credit standards and often retain sizable balance sheets, established market positions, and access to capital.

When bonds are downgraded from investment grade, forced selling by constrained mandates often drives prices below fundamentals. Once included in the fallen-angel universe, issuers frequently work to stabilize operations and repair balance sheets in an effort to regain their former ratings—turning fallen angels into potential rising stars.⁵

ANGL tracks an ICE BofA fallen-angel index that caps issuer exposure and removes bonds once they are upgraded back to investment grade.⁶ The result is a rules-based strategy that systematically captures bonds at a point of maximum pessimism while avoiding the lowest-quality segments of the junk market.

Portfolio Characteristics: Higher Quality, Different Risks

The defining feature of ANGL is its credit-quality tilt. Roughly three-quarters of the portfolio is typically rated BB, the highest tier of high yield, with minimal exposure to CCC-rated debt.⁷ By comparison, the broader high-yield market carries substantially more exposure to lower-rated issuers. This structural difference has important implications for default risk, volatility, and long-term outcomes.

That quality bias does come with trade-offs. Fallen angels often retain longer maturities from their time as investment-grade issuers, giving ANGL a duration profile closer to intermediate-term bonds than to traditional junk.⁸ As a result, the fund tends to be more sensitive to interest-rate movements than higher-coupon, shorter-dated speculative bonds.

Sector exposure can also differ meaningfully from broad high-yield benchmarks. Because inclusion is driven by downgrades rather than issuance, ANGL’s weights reflect where stress has occurred rather than where issuance is most active.⁹ This dynamic can add a contrarian element to returns but also introduces episodic concentration risk.

Performance History: Recovery Alpha, Rate Sensitivity

Over full market cycles, fallen-angel strategies have historically outperformed traditional high-yield benchmarks. Over the past decade, ANGL has delivered higher annualized total returns than broad junk bond ETFs, driven by a combination of lower default losses and price appreciation following credit improvement.¹⁰