Trump’s One Big Beautiful Bill has been signed into law and we’ve seen the impact to the financial markets already. Cyclicals got the biggest boost, led by materials and financials, in what the markets believe might be an economic expansion as a result. Tech was an outperformer again as more liquidity in the market should help the mega-caps with earnings growth. As growth shows signs of slowing, there’s a possibility that this bill helps mitigate some of that decline and supports the soft landing narrative. Tariffs and geopolitics have been headwinds over the past six months that threatened the economy with recession, but the OBBB may help the economy avoid that before expanding again later.

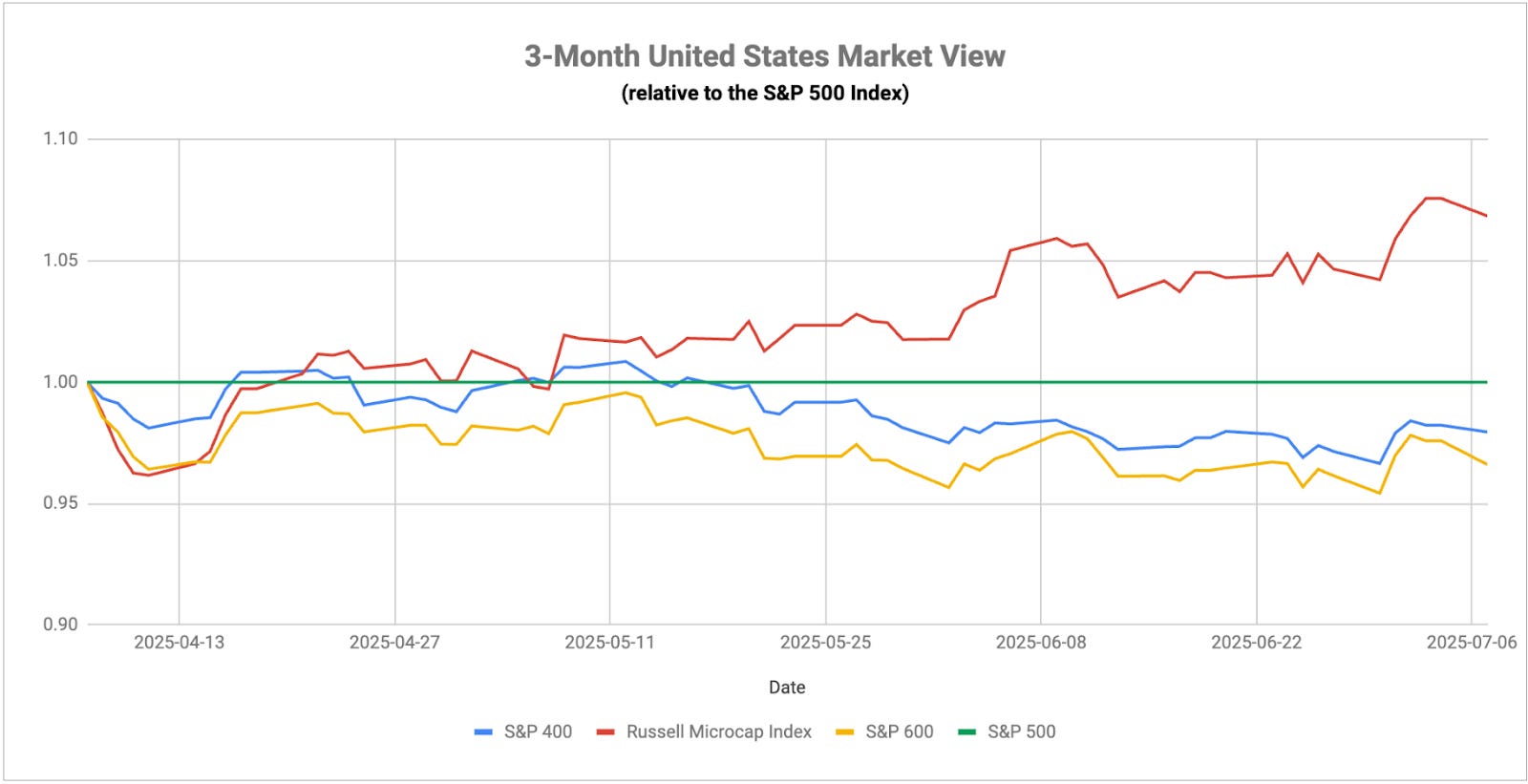

Another group that got a big tailwind (one that I’ve been waiting for for some time) was small-caps. Intuitively, this makes sense because smaller companies 1) have more cyclical exposure as opposed to the top-heavy mega-cap dominated large-cap indices and 2) are more reliant on debt to finance growth opportunities. Both of those factors got a big boost, the latter in particular because we’re likely to see more liquidity flooding the system with more Treasury issuance to fund the tax cuts. This could potentially be the longer-term catalyst that finally fuels a sustainable stretch of outperformance for small-caps.

The labor market, however, could pose some problems. While the non-farm payroll report suggests resilience, the ADP report, which measures just private sector activity, showed a loss of 33,000 jobs, the first negative print since early 2023 and the third straight month of decline. Digging further into the NFP report, we found that the job losses were largely constrained to small companies, while large companies added jobs. This kind of disparity is a negative for longer-term sustainable growth. Small companies are easily the largest employers in the U.S. on an aggregate basis and a contraction in hiring here likely signals underlying weakness in the labor market that might not be apparent in the higher level reports.

Treasury bonds and the dollar may have a tougher time moving forward. Yields will be pressured to move lower due to the imminent Fed rate cutting cycle, but the large Treasury issuance that’s likely coming in the months ahead will probably pressure rates higher in order to get the market to absorb all of the new supply. The dollar is probably in trouble too for similar reasons. More supply in the market devalues existing dollars in the system. That’s not even mentioning the fact that global corporations and central banks are looking to diversify away from their dollar exposures.

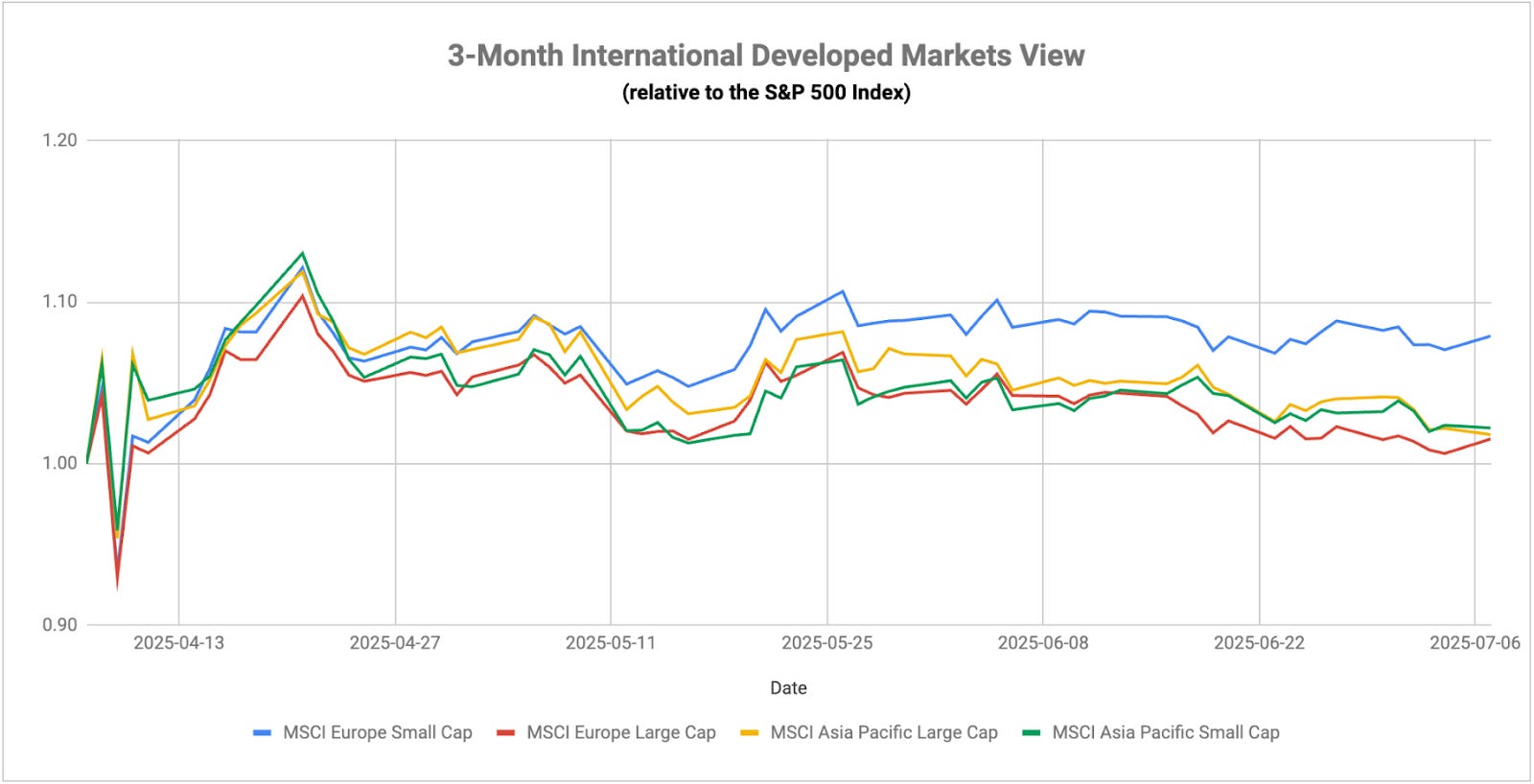

Eurozone inflation ticked up slightly in June, but remained at the ECB’s 2% target. With core inflation down to 2.3%, the central bank may now seek to balance out conditions and let the story play out for a while. It likely won’t want to cut rates too far and threaten to reignite inflation, but it also wants to build momentum for the region’s nascent yet tepid recovery. I think we’ll see a period where the ECB holds rates and allows time to see where the data leads now that trade tensions have eased and since it takes time for stimulative efforts to begin showing up in the system.