It's Getting More Serious

What Happens Next In The Global Trade War?

It looks like the global trade war might be starting to get a little more serious. While the tariff threats targeted at Colombia, Mexico and Canada were more politically driven (the latter two clearly with the aim of addressing border issues), the latest appear to be more economically driven. The 10% tariff on China had leveled the playing field until the 15% retaliatory tariff imposed by China on select products undid some of that. The 25% tariff on steel and aluminum imports have more of a protectionist tone to them given they don’t target any one country or region specifically. I think this raises the odds somewhat of long-term inflation risk, but the trade environment remains so fluid and is changing so often that it still seems silly to make longer-term projections with such a small sample size.

U.S. stocks still seem mostly resilient to the rhetoric. In the lead-up to through the days following Trump’s inauguration, large-caps fell by 5% and small-caps by 10% as the markets tried to price in the tariff threat. Since then, the equity market’s reactions to trade developments have been pretty muted, suggesting that investors know the rhetoric is likely to keep changing over time. Treasury yields, however, have predictably moved higher, although the overall downtrend doesn’t seem to be broken yet. The 10-year yield is up by about 12 basis points from last week’s low, but it’s just meeting its trendline again. Any further move higher in yields could, from a technical perspective, be viewed as an end to the downtrend and a potential sustainable move back higher again.

Supporting this is also Powell’s recent comments that the Fed is in no hurry to lower interest rates. This is consistent with what we’ve heard in the recent past, but there seems to be a groundswell of support for making no further cuts at all from a few Fed members. I think there’s certainly enough economic data available (labor market/unemployment, GDP growth, inflation) and subjective risk (trade war) to support the idea, although I think the Fed is also cognizant of 1) how such a move might impact the financial markets and 2) how Washington wants to push rates lower for debt relief if nothing else. Either way, higher for longer rates will likely act as a headwind for equity prices and could damage sentiment longer-term.

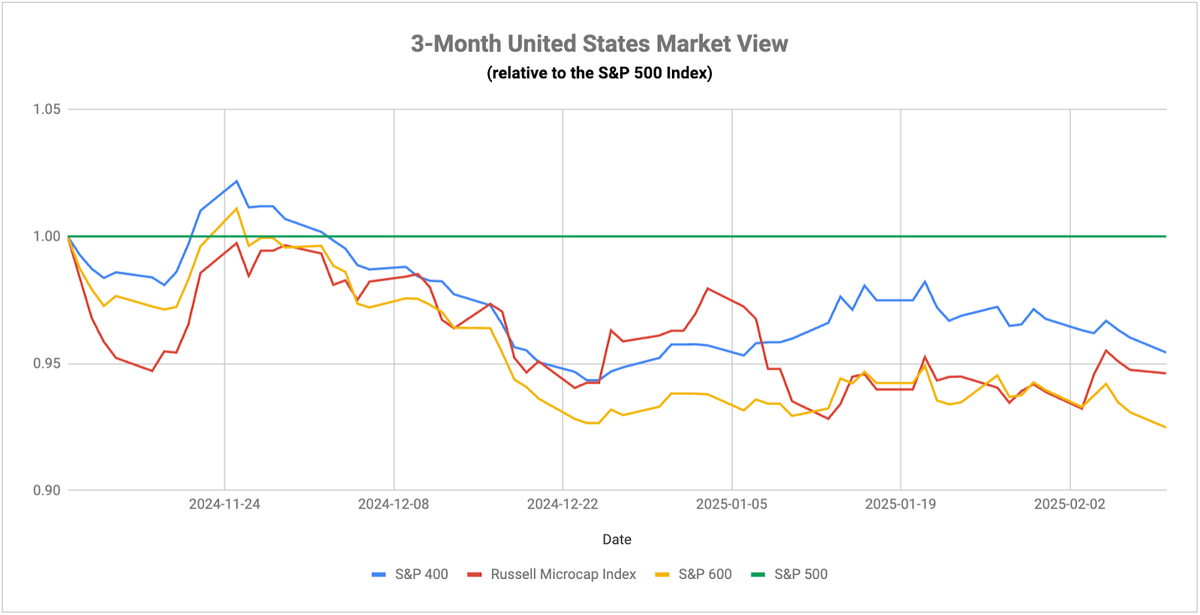

Small-caps are looking like an increasingly interesting play coming out of the Q4 earnings season. Small-caps have been beating earnings and revenue estimates at a higher rate than large-caps have, yet are still trading at roughly a 40% valuation discount. Small-caps clearly need some type of economic optimism to unlock some of the value that exists in their comparatively cyclical-heavy tilt, but at some point this group is getting too cheap to ignore. If you’re worried about the impact of a trade war, consider that small-caps are much more likely to be domestically based, mitigating some of the risk of higher import prices.