JOJO: Bombs In The Middle East Could Be The Catalyst That Wrecks The Junk Bond Market

The U.S. targeted bomb strike on Iranian military infrastructure is sparking fears of a wider conflict in the Middle East. How far oil prices spike will depend on Iran's response and the impact of shipping in the Strait of Hormuz. Regardless, geopolitical risks are likely to rise and that could ultimately drag all risk asset prices lower.

There’s a larger issue also forming in the credit markets. Credit spreads could finally get sharply wider.

And that could be a good environment for my tactical bond ETF, the ATAC Credit Rotation Fund (Ticker: JOJO)

The U.S. strike has already reignited geopolitical risk premium in a part of the world that still supplies a major piece of the global oil market. While Iran isn’t a big direct exporter to the U.S., its proximity to the Strait of Hormuz matters. If Iran retaliates or tries to close off that waterway, it could choke off supply chains and push oil prices even higher.

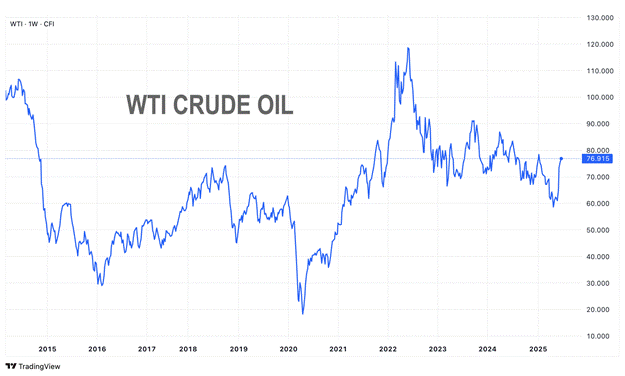

Could oil prices spike above $100? It's not out of the question if Iran makes a more aggressive response. It's the speed of the move that could be what rattles the markets. Volatility tends to wake up under-the-radar risks and one of those risks is credit.

When oil prices rise quickly, it's like a tax on the global economy. Gas gets more expensive, shipping costs rise and input costs for businesses, especially those that rely heavily on energy, start to erode margins. For corporations, it hits the balance sheet and it raises questions about their ability to service their debts on time.

That’s where credit spreads come in. We’re already seen some widening in high yield credit spreads as investors demand higher premiums to hold bonds from companies with more subpar credit profiles, especially in energy-related subsectors, such as transportation, manufacturing and retail. It’s not panic, but it’s a shift from the calm we’ve seen for a good chunk of 2025.

If this situation escalates further, the pressure builds even more. Companies with large debt loads, especially those with lower credit profiles, may find it harder and/or more expensive to refinance. That could lead to rising defaults, tighter lending standards and the credit spreads that govern the bond market start to widen.

It's important to point out that shocks like this don’t always lead to recession. They do, however, often result in tighter financial conditions. Higher oil prices correlate with higher inflation risk. That can delay rate cuts or even start talk of rate hikes. Then we run the risk of stagflation: slower growth combined with rising prices. That’s a very dangerous combination for corporate credit.

Moments like these can actually create opportunities. That's why the ATAC Credit Rotation ETF (JOJO) could be the perfect middle ground. It examines risks within the credit markets by looking at inter-asset relationships in order to assess whether the portfolio should be risk-on or risk-off. Times look turbulent? It shifts into Treasuries. Conditions calm down? It pivots into high yield bonds. By doing this, it aims to produce better risk-adjusted returns, limit downside risk and smooth out what could at times be a volatile ride.

It reinforces the case for keeping some balance in your portfolio. When geopolitical risk flares up, the market doesn’t necessarily move in expected ways. Bonds prices might go up even as credit weakens. Gold may rally. Utilities could outperform. It's a good time to make sure your portfolio isn’t overexposed to just one narrative.

As geopolitical risks rise, the markets could quickly turn volatile and credit spreads could widen quickly. It could be a good time to manage some of that risk with a time-tested credit rotation strategy.

Consider JOJO as part of your bond allocation strategy. Not because I developed the strategy and I’m the portfolio manager of the fund. Consider it because there are no gurus, only cycles. And the cycle may finally be here for it.

Michael A. Gayed, CFA

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The WTI Crude Index, a benchmark for U.S. oil prices established at Cushing, Oklahoma, serves as a critical financial barometer that measures the spot price of West Texas Intermediate light sweet crude oil—prized for its low sulfur content and excellent refining qualities—which is extensively used in futures contracts on the New York Mercantile Exchange to facilitate risk management and price discovery across global energy markets.

The VIX index, often called the "fear gauge" of Wall Street, is a real-time market index that measures the market's expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

JOJO is distributed by Foreside Fund Services, LLC.

Learn more about $JOJO at https://atacfunds.com/jojo/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.