JOJO: Getting The Signals Right

There Are No Gurus, Only Cycles

You just need the right set of conditions for a risk rotation strategy to work.

Of course, you’ll remember that 2022 was the historic anomaly. Stocks were correcting more than 20%, which should have been ideal for bonds as the “flight to safety” alternative. Instead, long-term Treasuries fell even more. The hyper-acceleration of inflation and the most aggressive rate hiking cycle in history from the Fed sent yields soaring.

In a period when investors needed bonds badly to act as a countermeasure to the downside risk of stocks, they failed. And they failed big time.

2025, however, is a different story. I’m known for repeating the line on X that “there are no gurus, only cycles.” Well - I believe the cycle has come finally for my own funds, which I arguably launched at the exact wrong time, and which may now be having their moment to shine.

Negative correlations between stocks & bonds began returning in the 4th quarter of 2024, but have really turned negative since the beginning of March. President Trump’s trade war escalation combined with a lack of Fed support on rates and genuine concerns about slowing economic growth have reinvigorated the flight to safety trade.

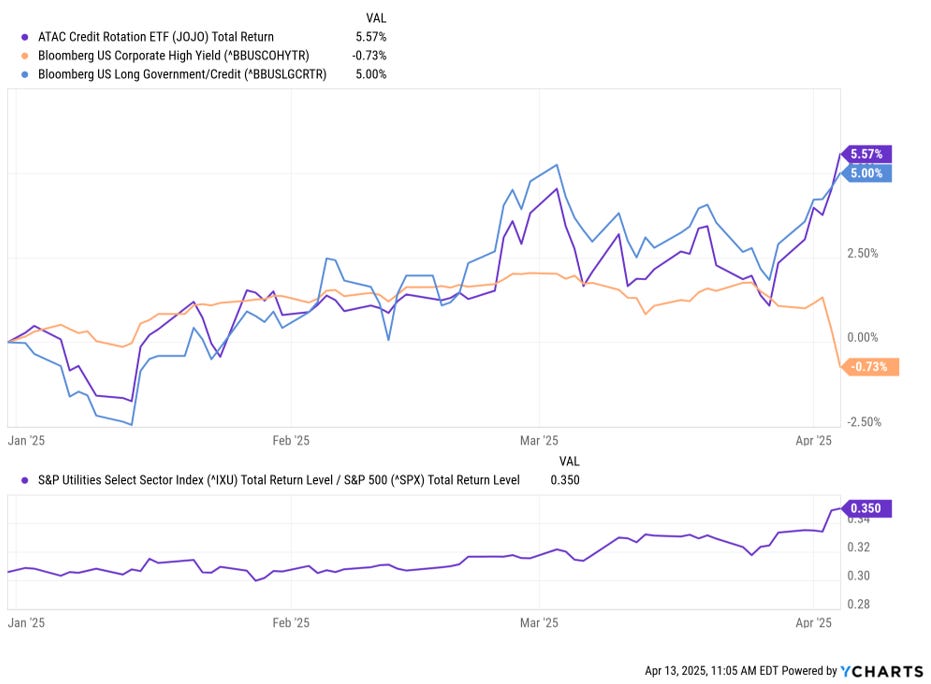

The ATAC Credit Rotation ETF (JOJO) took advantage of this shift, positioning junk-off prior to this volatility surge in all risk assets.

JOJO rotates between Treasuries and junk bonds as the risk-off/risk-on positions, respectively. The trigger for that positioning is the performance of the utilities sector relative to the S&P 500. When utilities outperform, the fund goes junk-off and vice versa.

Earlier this year, the utilities sector began outperforming consistently at the start of February. At the time, Treasuries were gaining, but so were junk bonds. Investors were generating positive returns regardless of which way the signal was leaning.

In March, junk bonds showed vulnerability as credit spreads began to widen and the markets began to get nervous about the impact of the Trump tariffs. Junk bonds, as a result, began falling, but because the utilities sector was outperforming, JOJO investors were positioned in the safety of Treasuries.

The real payoff, however, came starting in the second half of March through the tariff-fueled mini-crash in early April.

Thanks to utilities getting in front of all of this and positioning JOJO in Treasuries, investors were able to enjoy positive returns when more decisive risk-off conditions began setting in.

Most of all, however, JOJO shareholders were able to entirely avoid the early April correction in junk bonds. Because utilities had been signaling early that the threat of risk-off conditions was rising, they were able to position the fund defensively before any of this happened.

JOJO’s risk rotation strategy finally worked exactly how it was intended. And I believe deeply that we are at the start of a cycle where, as a tactical bond alternative, the credit rotation approach behind the fund may be set to shine.

As a result, JOJO was generating positive performance for investors while junk bonds were plunging.

Note: The performance data quoted above represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted above. Performance current to the most recent month-end can be obtained by calling (855-282-2386). For standardized JOJO performance https://www.atacfunds.com/jojo/. Extraordinary performance is attributable in part due to unusually favorable market conditions and may not be repeated or consistently achieved in the future.

As we can see from the volume number on this chart, the market has taken notice too. JOJO typically trades several thousand shares a day. On April 4th, the second straight day of carnage in the financial markets, JOJO traded nearly 600,000 shares.

With volatility high and a lot of uncertainty hanging over the markets today, a risk rotation strategy that accepts more risk when the skies are clear and takes risk off the table when storms are on the horizon might be worth consideration right now.

After all, JOJO just proved what it can do when conditions are just right.

And the storm clouds, I believe, have only just begun to form.

Consider JOJO as part of your bond allocation strategy. Not because I developed the strategy and I’m the portfolio manager of the fund. Consider it because there are no gurus, only cycles. And the cycle may finally be here for it.

Michael A. Gayed, CFA

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the "fear gauge" of Wall Street, is a real-time market index that measures the market's expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

JOJO is distributed by Foreside Fund Services, LLC.

Learn more about $JOJO at https://atacfunds.com/jojo/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.