While the financial markets focus on whether or not central banks will continue cutting rates, wondering where inflation is headed next or the impact of a global trade war, there’s one risk to the economy that’s never really gone away - the U.S. housing market.

I was reminded of it when I recently came across this post on Twitter/X.

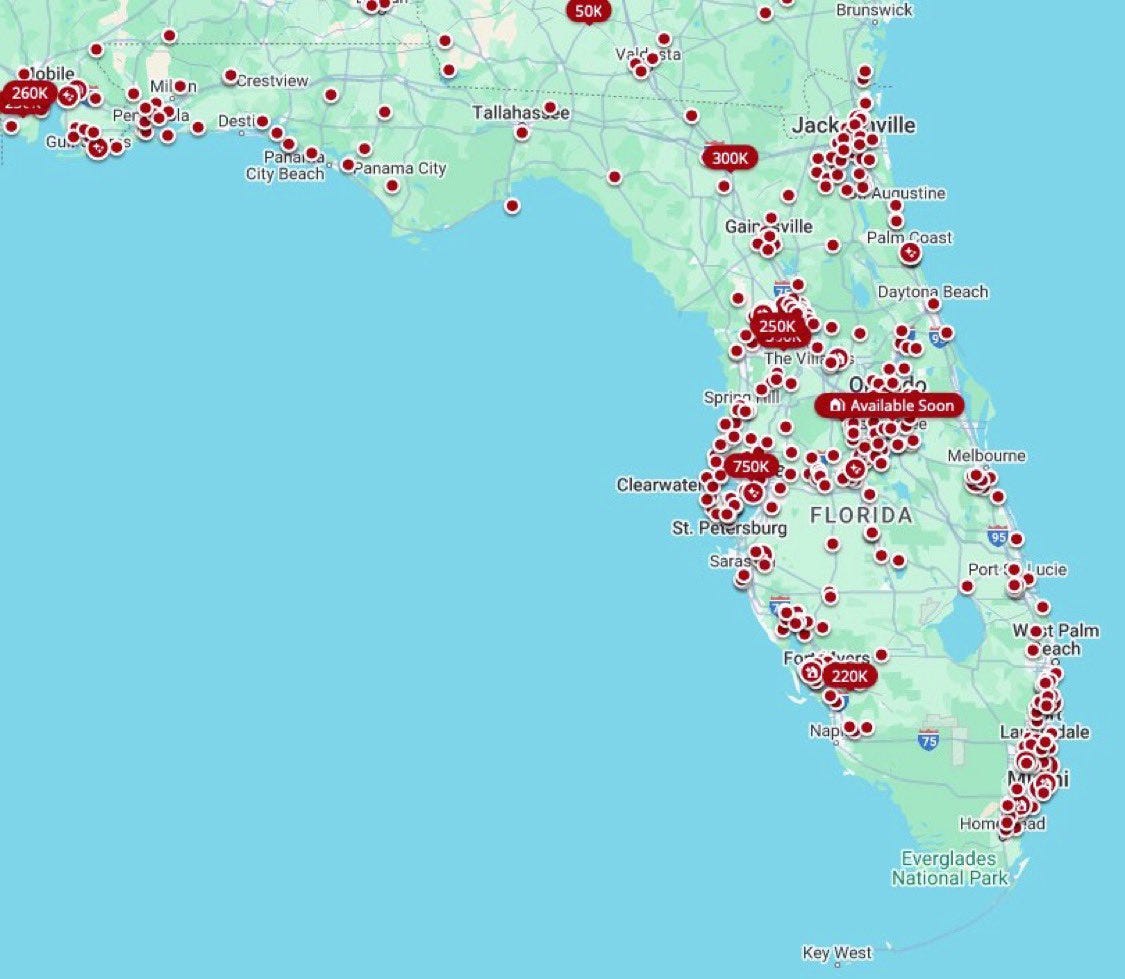

It’s a dot plot graph showing the concentration of homes for sale in Florida, whose number continues to grow. We know a lot of this is coming from the AirBnB bust, people who bought up houses for the purpose of renting them out and are now struggling to find renters. These folks could be getting crushed under a mountain of debt, especially if they bought multiple properties, and are scrambling to get out from under it.

There’s the other little issue of many homes in Florida becoming uninsurable due to natural disasters and the impact of climate change. The cost of homeowners insurance (for those that can get it) is skyrocketing and that’s leading to crushing affordability issues, especially in Florida, but in many other places across the country.

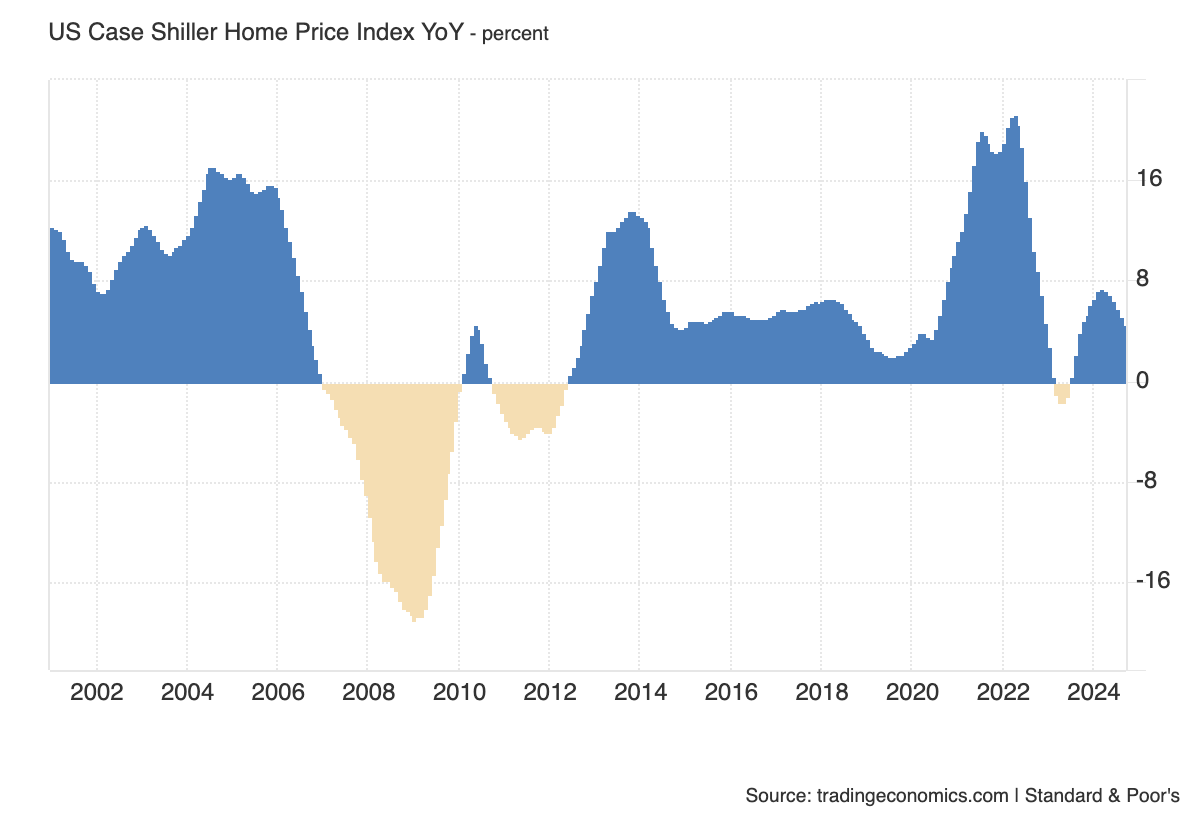

Now, if you look at the Case Shiller Home Price Index, things look just fine if you’re an existing homeowner and not interested in selling anytime soon.

While they’ve come way down from their post-pandemic peaks, home price growth is still running at about 4% year-over-year. That’s likely to come down a bit over the next few months as price growth was negative in both August and September. There’s a seasonality factor at play here, so declining prices heading into the end of the year aren’t necessarily unusual, but it’ll be important to see a rebound after we move into 2025.

The sharp move higher in interest rates in 2022 also created a huge gap between buyers and sellers that has effectively kept the housing market in gridlock. Sellers who were locked into low rates didn’t want to sell because they’d need to get a new loan at a higher rate. Buyers were struggling to afford the homes they wanted with those new higher rates and they were forced to either buy a lesser house or simply wait on the sidelines until conditions improved.

I think that’s a big part of what’s driving the Case Shiller Home Index higher. Yes, the expanding economy is certainly playing a part, but the lack of buyers and sellers along with a shortage of supply is creating a lack of price discovery.

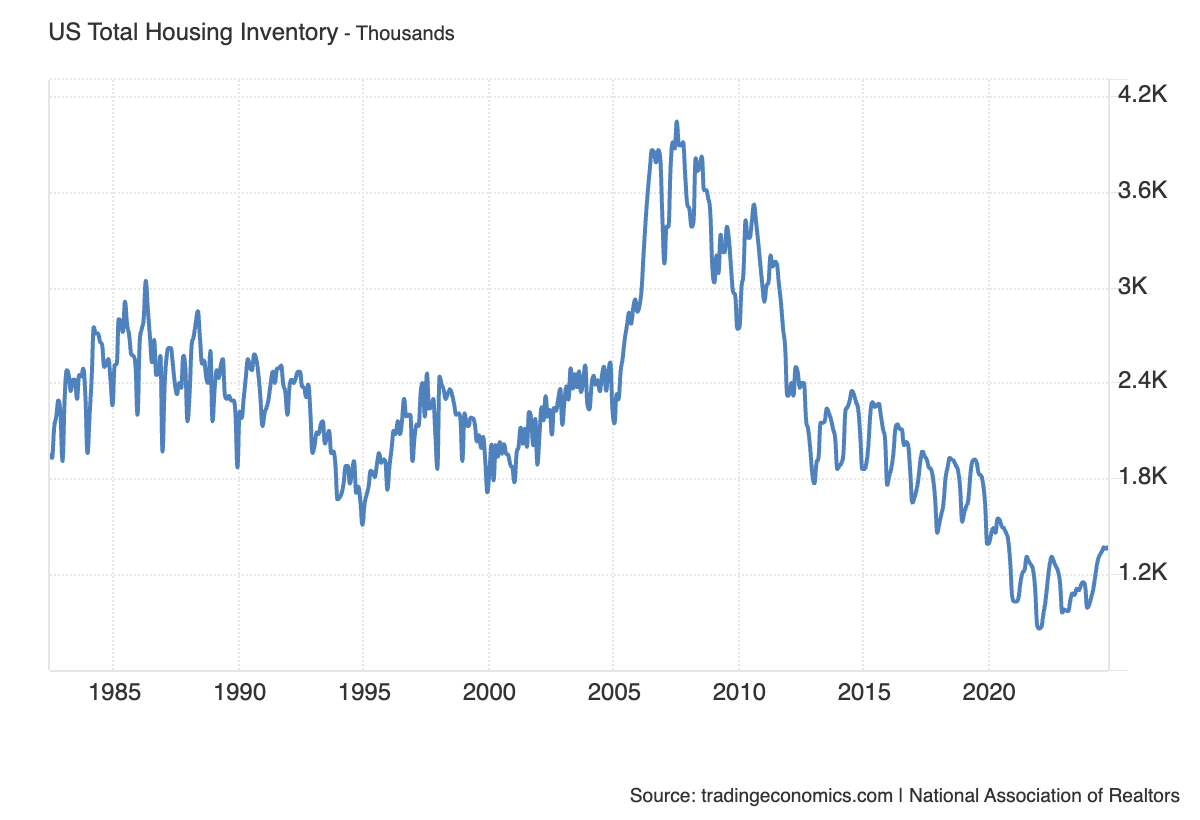

After the financial crisis in the late 2000s, housing supply returned back to historically normal levels by 2013. Once the COVID pandemic set in, a lot of people used their stimulus cash and low interest rates to either improve their existing houses or upgrade into new ones. Home prices soared and the supply of homes available for sale dropped dramatically. Supply is beginning to slowly pick up again, but it’s still got a long way to go to normalize.