The one consistent thing about the bond market over the past year has been volatility. In April, the 10-year yield got above 4.7%. By September, it was down to 3.6%. Earlier in January, it hit 4.8%. Long story short, the market is having a tough time trying to figure out the path of the economy, the Fed and inflation.

This seems to be a good time to review what we think we know and what that could mean for the rest of 2025.

A Bear Steepening Signals Recession

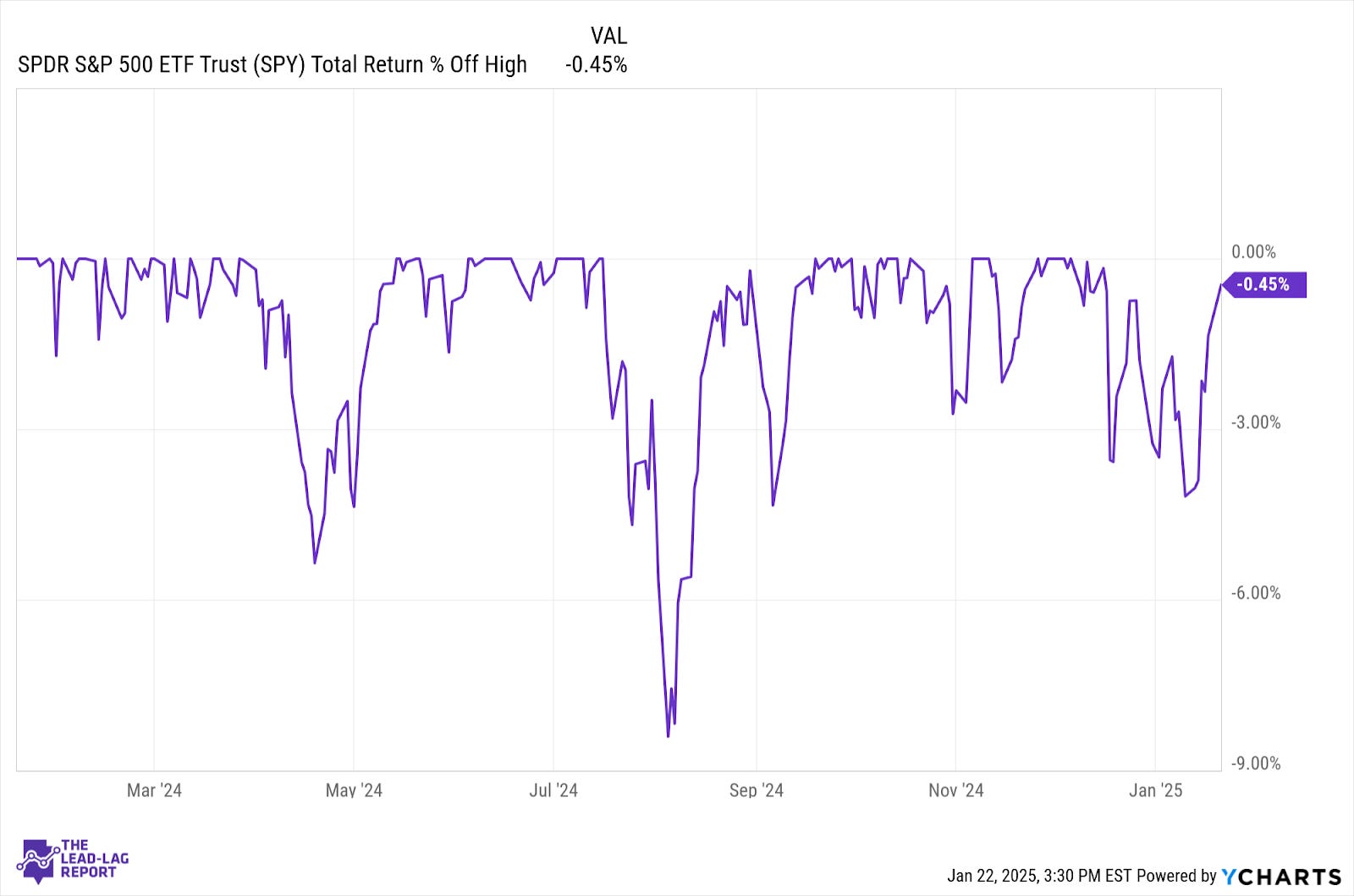

Despite evidence that credit conditions are deteriorating, inflation is rising and international economies are vulnerable, investors seem satisfied that a generally healthy U.S. economy and a tight labor market are enough to put a floor under stock prices. It’s fair to say that U.S. stocks, at least the S&P 500, have demonstrated resilience over the past year.

In April, large-caps pulled back 5%. Within a month, they were back to all-time highs. During the August reverse yen carry trade, the S&P 500 fell 9%. By the end of the month, it recovered almost all of that loss. On January 10th, the S&P 500 was 4-5% off of its peak. As of Wednesday, it’s back to a new all-time high.

Investors simply haven’t been willing to give up their enthusiasm for stocks no matter what the evidence is. Any dip is quickly being bought up. I suppose it’s fair for investors to be confident given this kind of history, but some of the indicators aren’t lining up. Perhaps the biggest one is bond yields.

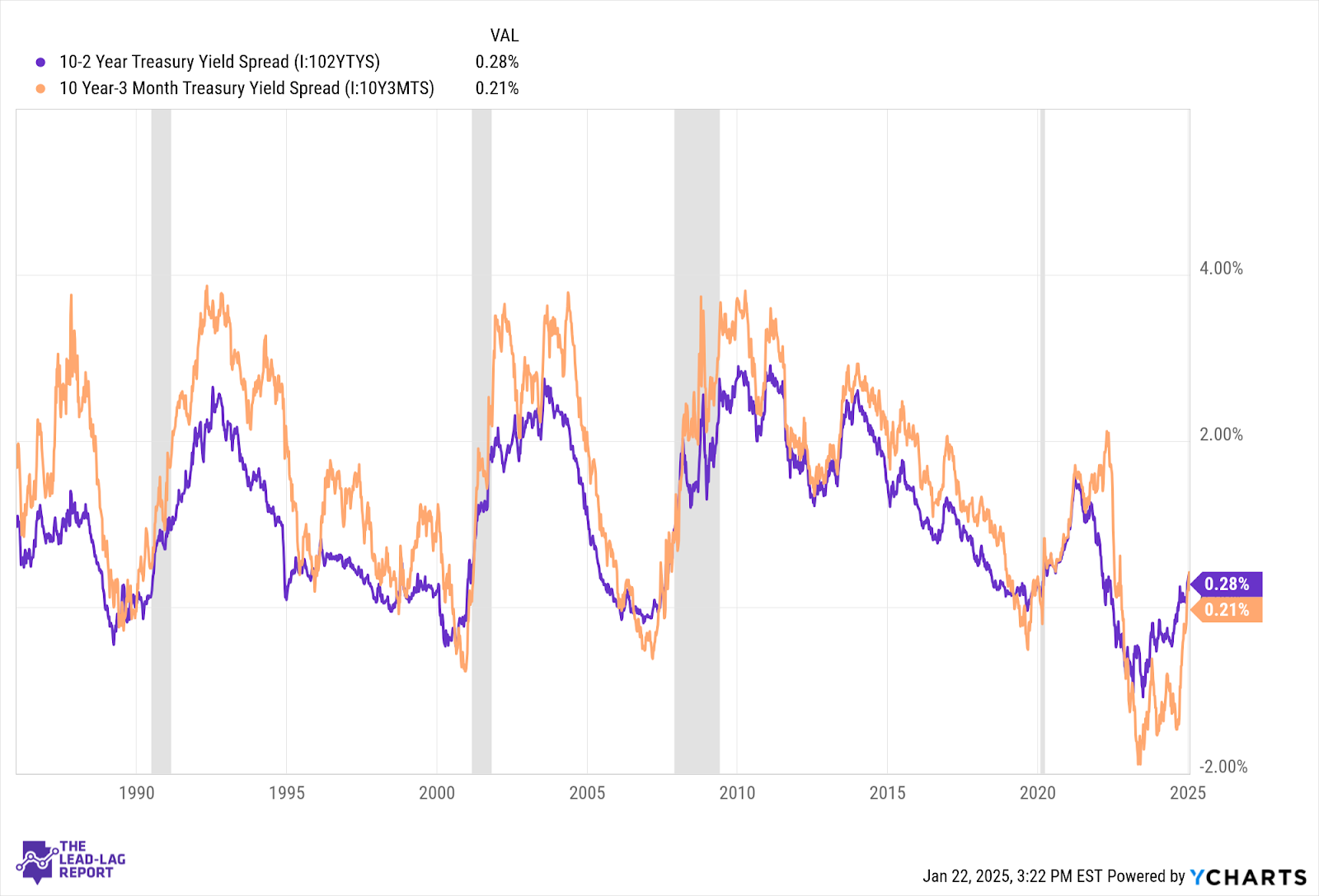

For more than two years, we saw the 10Y/2Y Treasury spread and the 10Y/3M Treasury spread inverted. It was the longest stretch in negative territory for these spreads in four decades. Now, both spreads are positive again and that’s not a good sign.

In the past four recessions, the yield curve uninverting has started the clock on recession watch. Each situation is unique, of course, but the one commonality is that a recession officially started within a year of these Treasury spreads turning positive. The 10Y/2Y spread first turned positive in late August, but the 10Y/3M spread didn’t turn positive until December. Even if you want to be a little generous in timing, based on historical precedent, that means recession is likely coming sometime in 2025.

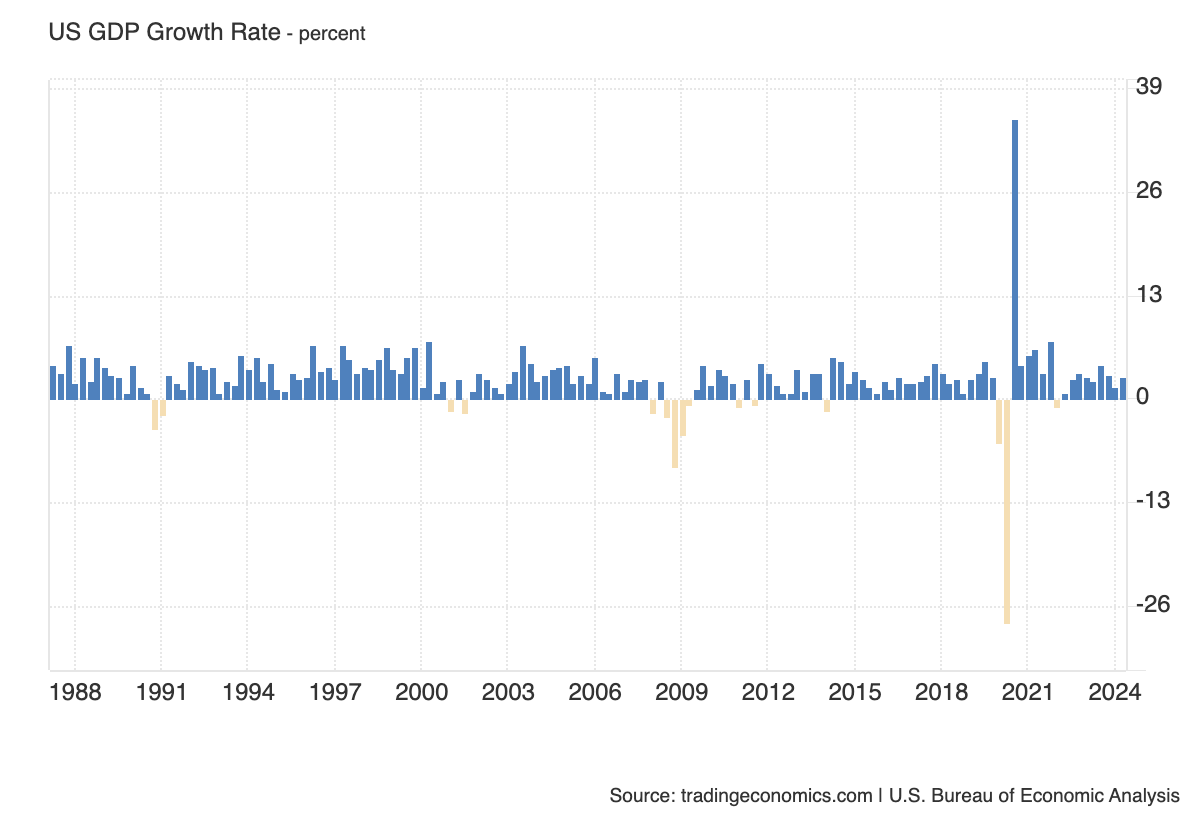

Your immediate argument might be that recession in the U.S. can’t be anywhere in our near future given how strong GDP growth is right now. Fair point, but keep in mind that GDP growth was also looking pretty good in the quarters leading up to the last four recessions.

So don’t discount the possibility that the economy could turn relatively quickly. Credit conditions, Japan and possibly inflation could be the catalysts.

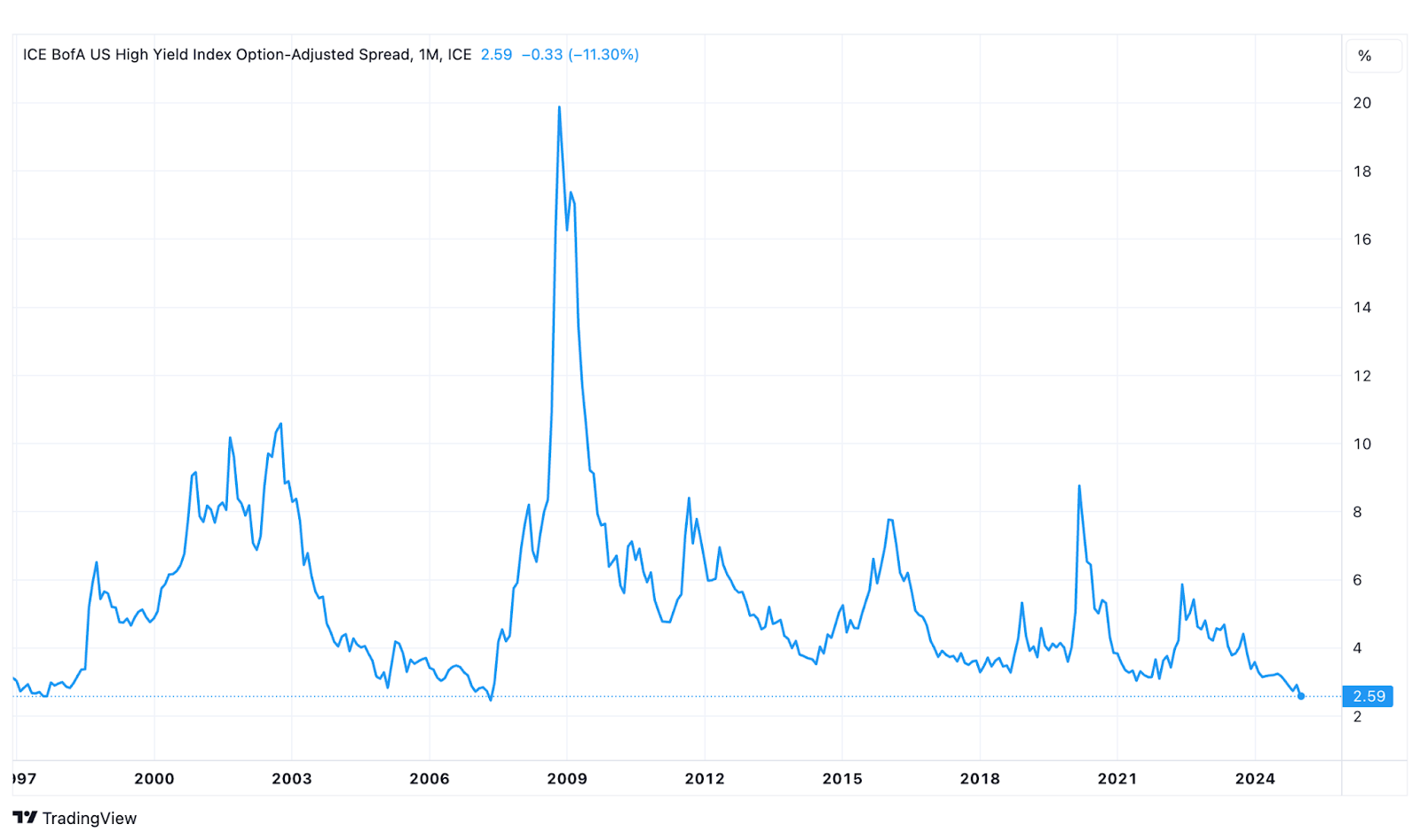

High Yield Spreads Are Severely Underpricing Risk

You probably know that this has been a sore spot for me. Delinquency rates are on the rise. Default rates are on the rise. The use of “buy now, pay later” schemes has skyrocketed. Some of these rates are at 10+ year highs. All of these point to increasing tensions in the bond market that have historically, on occasion, blown up spectacularly with the little forewarning.

Investors, however, don’t see those risks. Or they do and they’re choosing to ignore them. They’re not just underpricing risk either. They’re historically underpricing it.

Just this week, the high yield credit spread touched 2.59%. The last time it hit this level? June 20, 2007. Just a few months later, the S&P 500 would hit an all-time high for the last time before the S&P 500 plunged more than 50% during the financial crisis. In case you don’t think this can happen quickly…

Special Announcement

Where Sophisticated Investors Access Private Markets

For individual investors, sourcing and vetting high-quality, sub-scale private market opportunities poses challenges – information asymmetry, adverse selection, insufficient resources, etc.

Enter 10 East.

10 East, led by Michael Leffell, allows qualified individuals to invest alongside private market veterans in vetted deals across private credit, real estate, niche venture/private equity, and other one-off investments that aren’t typically available through traditional channels.

Benefits of 10 East membership include:

Flexibility – members have full discretion over whether to invest on an offering-by-offering basis.

Alignment – principals commit material personal capital to every offering.

Institutional resources – a dedicated investment team that sources, monitors, and diligences each offering.

10 East is where founders, executives, and portfolio managers from industry-leading firms diversify their personal portfolios.

Join with complimentary access at 10east.co

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of 10 East. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of 10 East and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

Investors Anticipate Rate Cuts In 2025; Treasuries Say Not So Fast

There are all sorts of ways to interpret what Treasury bond yields are telling us, but there is a generally accepted rule when it comes to what different points on the curve mean:

3M yield - reflects where Fed policy rates are right now

2Y yield - reflects where the market thinks Fed policy is heading

10Y yield - reflects economic sentiment

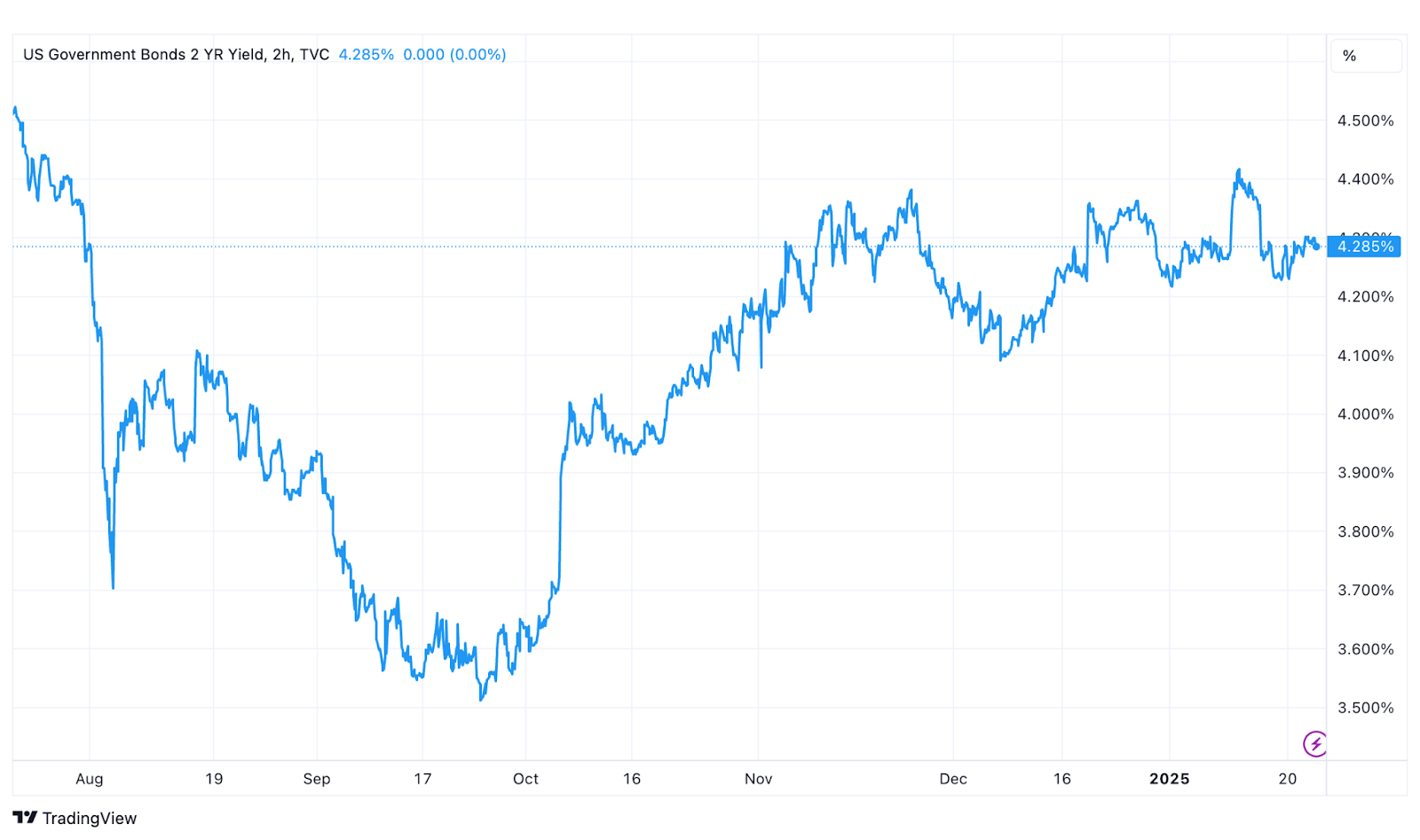

Even though a lot of the market’s more dovish expectations have been priced out of the futures market, it’s still pricing in 1-2 more rate cuts by year-end with the first potentially occurring mid-year. But if you look at the 2-year Treasury yield, it doesn’t agree.

On the day after election day, the 2-year yield was around 4.25%. As I write this, the 2-year yield is at 4.28%. In other words, it’s not seeing any rate cuts at all. In fact, it’s tilting slightly in the direction of a rate hike.

That would be consistent with some of the inflation data we’re seeing right now. Despite the fact that the December CPI report came in 0.1% below expectations, many inflation measures, both in the United States and overseas, are showing inflation trending higher again. If Trump decides to enact some of his tariff policies over the next month, figure that the pressures will only increase more. If inflation starts to spiral higher again, it’s not out of the question that the Fed decides to pivot mid-year and consider another hike to try to bring conditions back under control.

When the bond market is pricing in an historically low level of credit risk despite evidence pointing to the contrary and is also suggesting that the Fed won’t be able to cut in the way the market thinks it does, it becomes vulnerable to a sharp repricing of yields higher that creates volatility and puts stocks at risk.

Final Thoughts

A lot of people will read this and call me a permabear. I’m simply looking at what the data and the evidence are telling us. As I’ve often said, the bond market is right more often than the stock market. Right now, it’s saying that there is more risk looming than the market thinks.