Nine Green Weeks. One Hawkish Whisper.

When does record euphoria become a setup, not a celebration?

Special Announcement

The Relative Sentiment Tactical Allocation ETF is a flexible, multi-asset fund that invests across stocks, bonds, commodities, precious metals, and currencies. Its approach is guided by a research-based factor called relative sentiment—which tracks how optimistic or cautious professional investors are compared to individual investors. Studies show professionals tend to have an edge over time, and this ETF seeks to capture that insight by increasing exposure to areas where institutions are more optimistic and reducing exposure where they’re more cautious. Relative sentiment often complements trend-following strategies, helping create portfolios that may be more balanced and less prone to sharp swings.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. This and other important information is contained in the prospectus, which may be obtained by following the links Prospectus and SAI or by calling +1.215.882.9983. Please read the prospectus carefully before investing.

Investments involve risk. Principal loss is possible.

The Fund is distributed by PINE Distributors LLC.

ETFAC-4976143-11/25

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Relative Sentiment. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Relative Sentiment. and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

Nine Green Weeks. One Hawkish Whisper.

Key Highlights

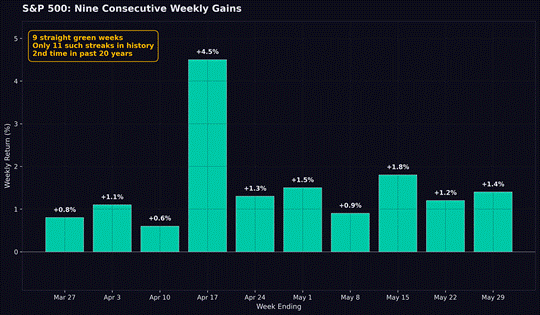

● The S&P 500 closed its ninth consecutive weekly gain, a feat seen only eleven times in market history and just twice in the past two decades.

● Dell Technologies posted its best single-day stock performance ever after raising AI server guidance to $60 billion for the fiscal year.

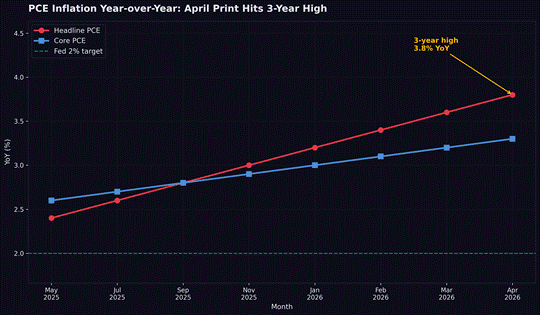

● April PCE inflation hit 3.8% year-over-year, the highest reading since May 2023, with the Fed’s own minutes admitting rate hikes are now on the table.

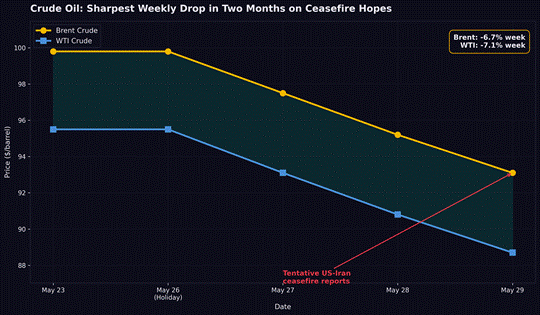

● Oil collapsed below $90 on tentative US-Iran ceasefire negotiations, even as high-yield credit spreads sat at 2.72%, near multi-decade tights.

The Surface Narrative

Markets ended May with a flourish that would have been hard to imagine in February. The S&P 500 logged its ninth straight weekly gain, finishing the month up roughly five percent.1 The Nasdaq climbed about eight percent on the month, and all major indexes printed record highs by Thursday. Dell Technologies stole the week, surging more than thirty percent in a single session after blowing past earnings expectations and raising guidance.2 Oil tumbled below ninety dollars a barrel as US and Iranian negotiators reportedly inched toward a sixty-day ceasefire extension that would clear mines from the Strait of Hormuz.3 On the surface, this was a celebration of disinflation, peace, and artificial intelligence.

The headline tape supports that read. A nine-week winning streak in the S&P 500 has happened only eleven times since reliable weekly index data began. Just two of those occurrences fall inside the last twenty years. Streaks of this length are rare not because markets cannot rise, but because the path higher is almost always punctuated by at least one weekly setback. Nine weeks without one signals an unusual absence of selling pressure, and that absence has its own message.

Beneath the surface, the story is more uncomfortable.

Chart 1: S&P 500 nine consecutive weekly gains, the second such streak in 20 years.

The Real Catalyst

Strip away the headlines and the week’s gains came from two engines that have been doing the heavy lifting all year. The first is artificial intelligence capital expenditure, now flowing through to enterprise earnings in ways that are no longer abstract. Dell reported quarterly revenue of $43.8 billion, an eighty-eight percent year-over-year jump, with AI server revenue alone growing more than sevenfold to $16.1 billion.2 Management raised its AI server backlog to $24.4 billion and lifted the full-year revenue outlook to $167 billion. That is not a forecast about future demand. That is shipped product.

The second engine is geopolitical de-escalation, or at least the hope of it. Reports out of the negotiating channels suggested Tehran would remove mines from the Strait of Hormuz within thirty days in exchange for a gradual lifting of the US naval blockade and partial sanctions relief.3 About twenty percent of global oil and liquefied natural gas transits through that chokepoint. The mere possibility of normalization was enough to send Brent down nearly seven percent on the week, its sharpest decline in two months.4

Together those two threads flipped sentiment from defensive to offensive in the span of a few sessions. Whether they justify nine consecutive green weeks is the question worth asking. The narrative shift is real. The price action confirms it. The question is whether the underlying data confirms it as well, or whether the market has run ahead of what the macro evidence can support.

Chart 2: Brent and WTI crude oil prices, week ending May 29, 2026.

Divergences Beneath the Surface

The same week that produced fresh records also produced the highest core inflation read in three years. April personal consumption expenditures rose 3.8% on a headline basis and 3.3% on the core measure, the hottest print since May 2023.5 Energy did much of the lifting, which is the kind of inflation the Fed historically tries to look through. The problem is that the Federal Reserve published its April meeting minutes on Wednesday and the language was striking. A majority of participants signaled openness to rate hikes if inflation remains persistent.6 The committee has held the target range at 3.50 to 3.75 percent for three consecutive meetings, but the directional bias has quietly turned hawkish.

That matters because Kevin Warsh inherits this Fed at the June meeting. The incoming chair will take the gavel with inflation accelerating rather than decelerating, with energy prices subject to a binary geopolitical outcome, and with a market that has spent nine weeks pricing in the opposite scenario.

The ten-year Treasury yield finished the week near 4.45 percent.7 High-yield credit spreads closed at 2.72 percent on May 28, against a long-term average of 5.18 percent.8 That is one of the tightest readings of the current cycle. Credit markets are priced for a soft landing that the Fed minutes just suggested may not arrive. Real personal consumption expenditures grew only 0.1 percent in April, and the saving rate sits near a four-year low.5 The consumer is bending even as risk assets are pricing perfection.

Chart 3: Headline and core PCE inflation, year-over-year.

When equity valuations stretch and credit spreads compress while inflation accelerates and central bank rhetoric turns hawkish, the divergence is the signal. The week’s narrative was AI and peace. The week’s data was sticky inflation and a Fed flirting with tightening. Those two stories cannot both be right indefinitely. One will resolve into the other.