No Collapse, No Cut Panic

Labor steadiness complicates the easing narrative even as inflation cools.

Key Highlights

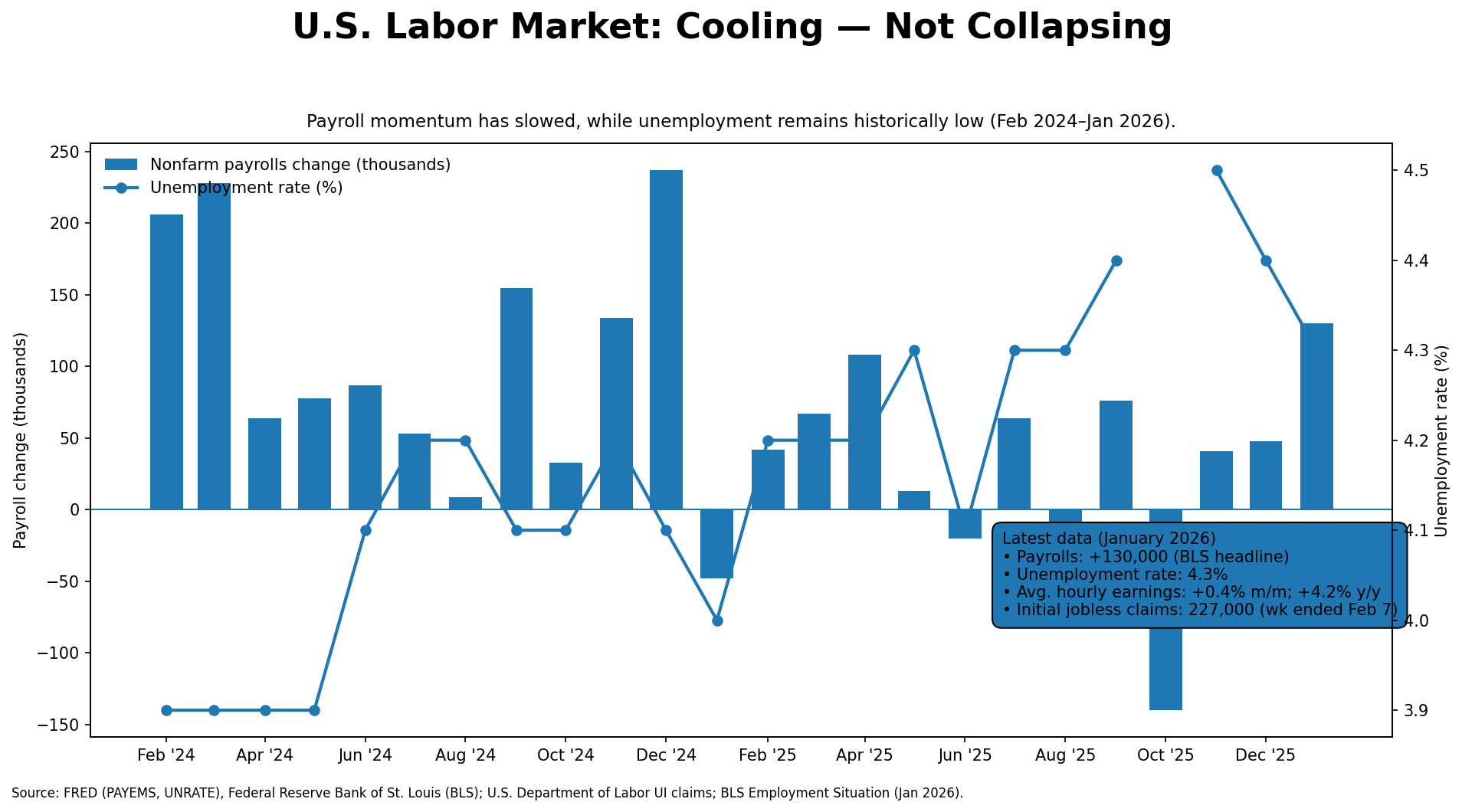

January payrolls rose 130,000 and unemployment dipped to 4.3%, reinforcing a growth floor rather than signaling labor stress.¹

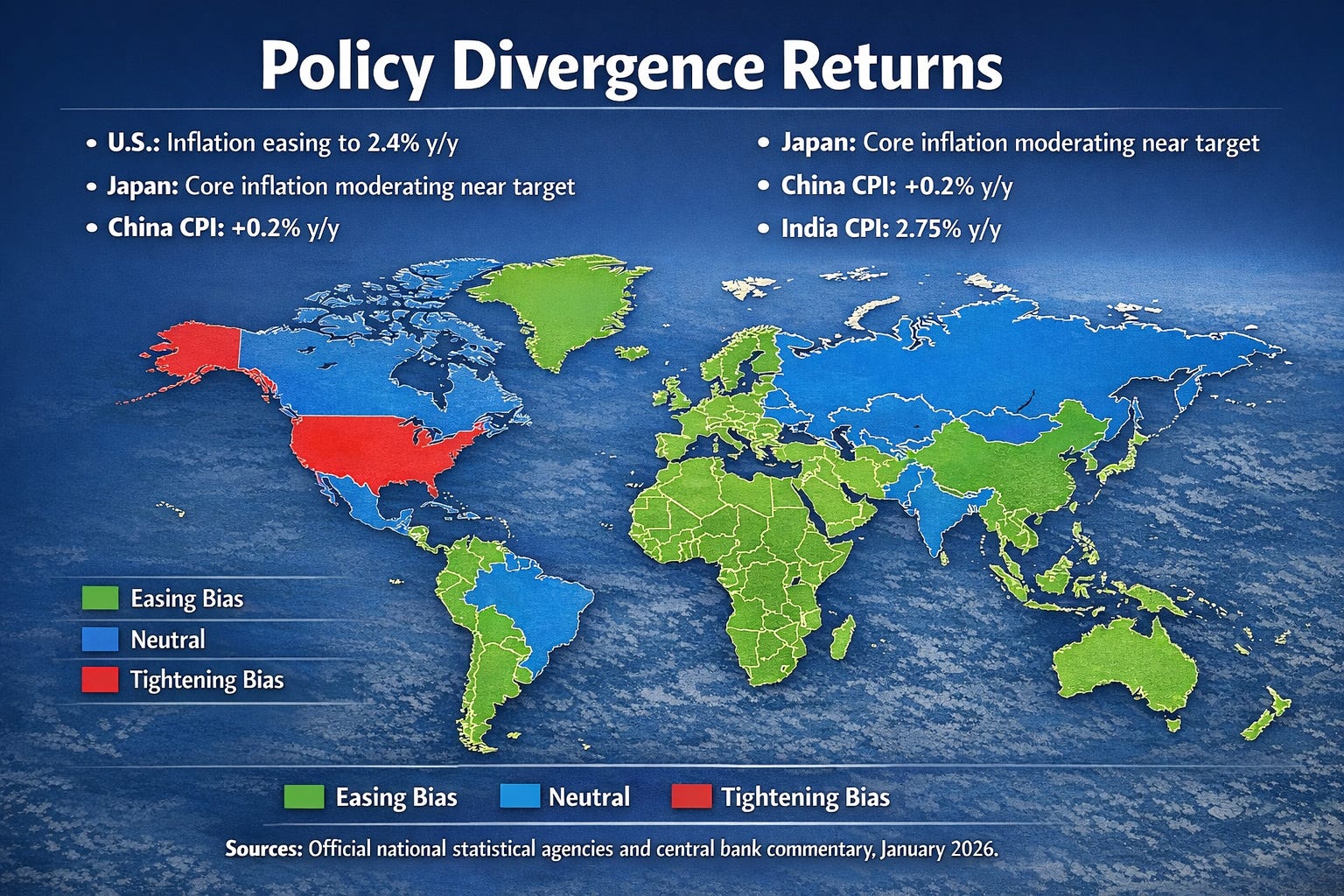

CPI cooled to 2.4% year over year, reopening the path to potential mid-year easing without validating aggressive near-term cuts.²

The Treasury curve flattened modestly as long-end yields declined, with the 10-year falling 13 basis points over the week.³

High-yield spreads widened only slightly, suggesting repricing rather than systemic stress.⁴

The dollar weakened on the week as rate futures increased the probability of a June cut.⁵

The yen posted its strongest weekly gain in roughly a year amid renewed tightening expectations in Japan.⁶

The U.S.: A Growth Floor with Cooling Inflation

The macro sequence this week mattered more than the absolute numbers. Labor came first. January nonfarm payrolls rose by 130,000, while the unemployment rate edged down to 4.3%.¹ Wage growth remained firm at 0.4% month over month and 4.2% year over year, with the workweek ticking up to 34.5 hours.¹ Initial jobless claims declined to 227,000 for the week ended February 7, reinforcing the view that layoffs remain contained.⁷

The signal was clear: the U.S. economy is not breaking. It is slowing at the margin, but it is not rolling over.

Consumption, however, showed signs of fatigue. December retail sales were unexpectedly flat, with the Census Bureau describing activity as “virtually unchanged” from November.⁸ That nuance matters. The labor market may be stable, yet spending momentum is no longer accelerating.

Inflation then shifted the narrative. January CPI rose 0.2% on the month and cooled to 2.4% year over year.² Core CPI increased 0.3% month over month and 2.5% year over year.² Gasoline prices fell 3.2%, while several service categories reflected early-year price adjustments.⁹

The takeaway is not that inflation has vanished. Core remains sticky enough to prevent an immediate easing cycle. Yet the disinflation trend resumed. That was enough to revive the mid-year rate-cut conversation without forcing the Federal Reserve’s hand.

Markets translated the sequence into duration demand. From February 6 to February 12, the 10-year Treasury yield declined from 4.22% to 4.09%, while the 30-year fell from 4.85% to 4.72%.³ The 2-year eased modestly, producing a flattening in the 10-year minus 2-year spread.³

Rate futures responded quickly after CPI, increasing the implied probability of a June cut and adding easing expectations into 2026.⁵

Credit markets did not flash stress. The ICE BofA U.S. High Yield option-adjusted spread widened slightly from 2.87% to 2.92%.⁴ That move reflects risk repricing rather than funding pressure.

Equities behaved like a market still sensitive to rate volatility and crowded positioning. A sharp growth-led selloff midweek tied to AI-related positioning concerns was only partially repaired by Friday’s inflation relief.¹⁰ Dispersion remained elevated, with internal volatility masking headline index stagnation.¹¹

Liquidity plumbing also remained in focus. The New York Fed indicated that elevated reserve-management purchases of Treasury bills would continue into mid-April, framing the activity as operational rather than stimulative.¹² Meanwhile, the Treasury General Account remained elevated on a weekly basis, leaving near-term liquidity sensitive to bill issuance and tax flows.¹³

The dollar’s weekly decline aligned with the shift in rate expectations. Even as it stabilized into Friday, the broader move reflected markets rotating away from “higher for longer” protection.¹⁴ U.S. policy commentary describing the dollar as closer to a “more natural” trade level added to that tone.¹⁵

Developed Markets: Policy Divergence Reawakens

Europe’s story was more narrative than numeric. An ECB policymaker emphasized that Europe should prepare for a larger safe-haven role globally, highlighting the importance of liquidity backstops and institutional resilience.¹⁶ The euro held firm on the week, consistent with a softer dollar backdrop.¹⁴

The U.K. remains constrained by soft growth and persistent underlying inflation. Public reports showed marginal late-year growth, while the Bank of England’s chief economist emphasized that underlying inflation remains around 2.5% and policy must stay restrictive long enough to complete disinflation.¹⁷ Sterling traded within a tight range, reflecting cross-currents between U.S. repricing and domestic caution.¹⁸