Policy Volatility Meets Narrow Leadership: Markets Reprice Risk Without Credit Stress

A cooling but still-expanding growth backdrop is colliding with trade-policy shocks and AI-driven equity dispersion.

Key Highlights

U.S. labor data remain low-fire, but survey growth indicators are cooling toward a ~1.5% annualized pace.¹ ²

FOMC minutes reinforced a “higher for longer unless inflation reasserts disinflation” stance, with liquidity mechanics adding a subtle tightening bias.³

Treasury yields drifted modestly lower across the curve, which remains positively sloped and not recessionary.⁴

Equity index stability masks weak breadth and sharp dispersion within technology, particularly between semiconductors and software.⁵

High-yield credit spreads remain near cycle tights, signaling risk repricing without systemic stress.⁶

Late-Cycle Macro With a Data and Policy Uncertainty Overlay

The defining feature of the Feb. 18–25 window was not a single outsized data surprise, but confirmation of a late-cycle configuration: labor markets remain resilient, growth is cooling at the margin, and policy uncertainty—particularly around trade—is injecting volatility into cross-asset risk premia.

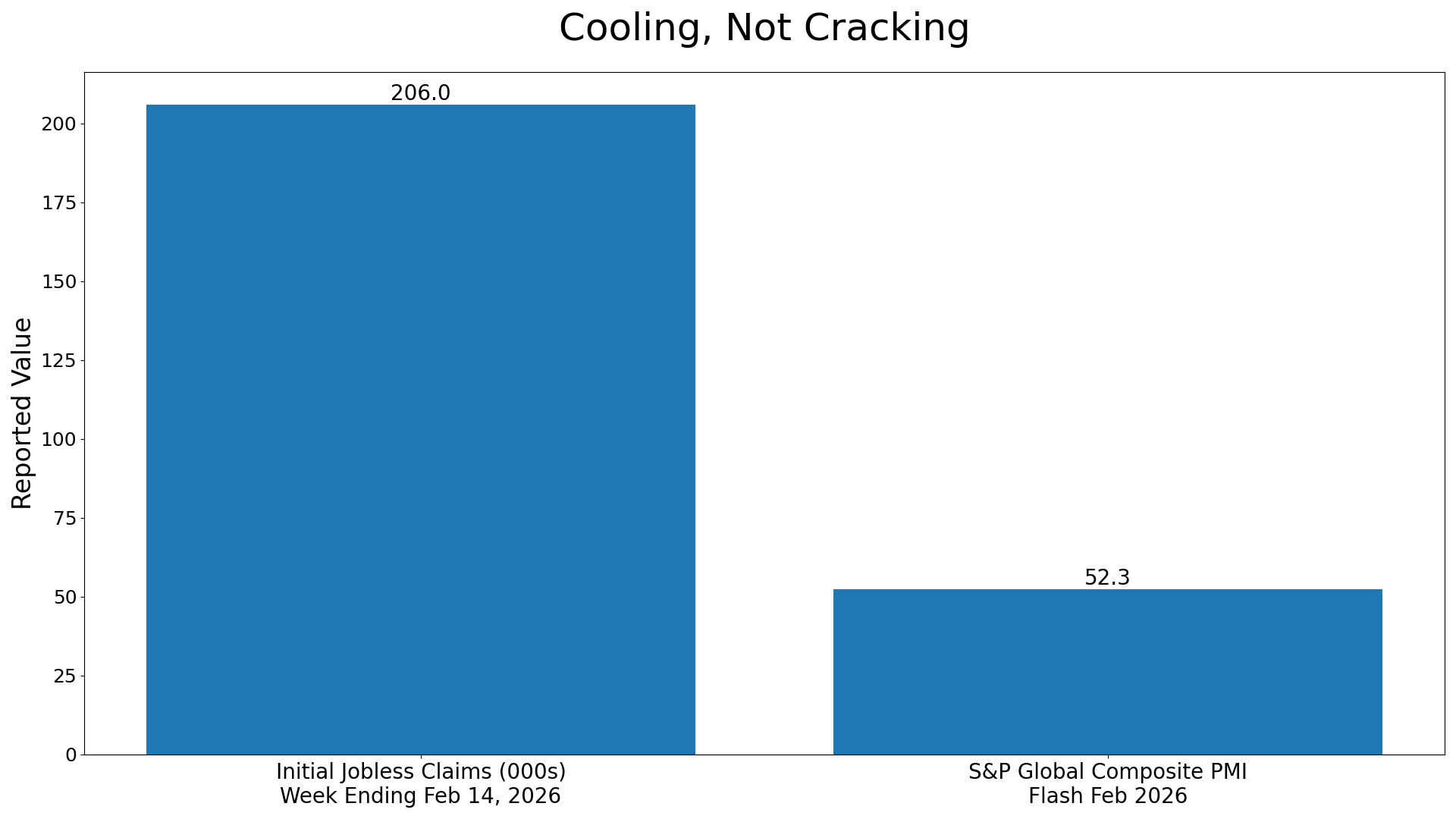

Weekly initial jobless claims fell to 206,000 for the week ending Feb. 14, underscoring that layoffs remain subdued. Continuing claims rose to roughly 1.869 million, suggesting that while separations are limited, job-finding is becoming incrementally more difficult.¹ The signal is not labor stress, but labor normalization.

Forward-looking growth data tell a similar story. The February flash S&P Global composite PMI eased to 52.3 from 53.0, still expansionary but marking the slowest pace in roughly ten months. Survey-based GDP mapping implied growth closer to 1.5% annualized early in the year, down from the stronger late-2025 cadence.² Employment components hovered near stagnation. The expansion continues—but with diminishing momentum.

Inflation did not deliver a fresh catalyst during the week. Instead, the January FOMC minutes sharpened the Fed’s reaction function. Policymakers emphasized that inflation remains “somewhat elevated” and that further easing would require clearer evidence that price pressures are sustainably converging toward 2%.³ The Committee also referenced market pricing for one to two cuts in 2026, underscoring that policy is not on a preset path.

Importantly, the minutes highlighted liquidity mechanics that can tighten or ease conditions without a change in the policy rate. Reserve management purchases, Treasury General Account flows, and tax receipts were discussed as endogenous drivers of reserve levels.³ In an environment where reserve scarcity could re-emerge, these balance-sheet dynamics matter for money markets and front-end stability.

Macro uncertainty is also literal. The Chicago Fed’s CFNAI publication process has flagged delays stemming from federal shutdown-related disruptions and delayed statistical releases.⁷ The FOMC minutes similarly acknowledged data delays as a forecasting challenge.³ This is a subtle but material shift: uncertainty is no longer purely economic—it is embedded in the data pipeline itself.

Overlaying this backdrop is policy volatility. On Feb. 20, the U.S. Supreme Court struck down emergency tariffs, prompting the administration to signal new levies under alternate legal authority.⁸ The macro transmission channel here is uncertainty rather than immediate price effects. Rapid shifts in trade policy elevate risk premia across equities, credit, and FX—even absent a deterioration in hard data.

In short, growth is cooling but intact, inflation remains a constraint, and policy volatility has become the dominant shock variable.

The Rates Transmission: Mild Easing, No Recession Signal

Rates markets translated this environment into modest duration support but no recession warning.

Between Feb. 18 and the latest H.15 data available during the week (through Feb. 23), the 10-year Treasury yield declined from 4.09% to 4.03%, while the 2-year fell from 3.47% to 3.43%. The curve remained positively sloped, with the 10-year minus 2-year spread narrowing only slightly.⁴ This is not inversion; it is mild flattening within an upward-sloping structure.

Real yields also eased. The 10-year TIPS yield declined from 1.80% to 1.77%.⁴ That incremental decline supports duration-sensitive equities, but it does not suggest a collapse in real-rate expectations. Markets are pricing moderation—not contraction.

Fed communication reinforced this equilibrium. Governor Christopher Waller indicated he could support holding rates steady at the March meeting if incoming labor data confirm improved momentum.⁹ That conditional stance keeps front-end expectations tightly linked to labor confirmation rather than preemptive easing.

The curve’s message is therefore consistent: growth is decelerating, but not rolling over. Inflation is moderating, but not definitively conquered. The Fed is patient, and duration is drifting lower without signaling recession.

This rates backdrop matters because it forms the discount-rate anchor for equities. With real yields stable to slightly lower and no acute credit stress, equity volatility must be interpreted through the lens of dispersion rather than systemic repricing.

Equity Dispersion and Credit Containment Define the Regime

U.S. equities exhibited two simultaneous truths during the window. Index-level resilience persisted, but participation narrowed.

From Feb. 18 to Feb. 24 closes, the S&P 500 rose modestly, and the Nasdaq gained, while the Dow and Russell 2000 declined.⁵ This divergence signals that headline stability masks underlying concentration.