Relief Rally, Fiscal Shadow

Can risk assets celebrate lower tariff pressure if the bond market insists on repricing fiscal risk?

Key Highlights

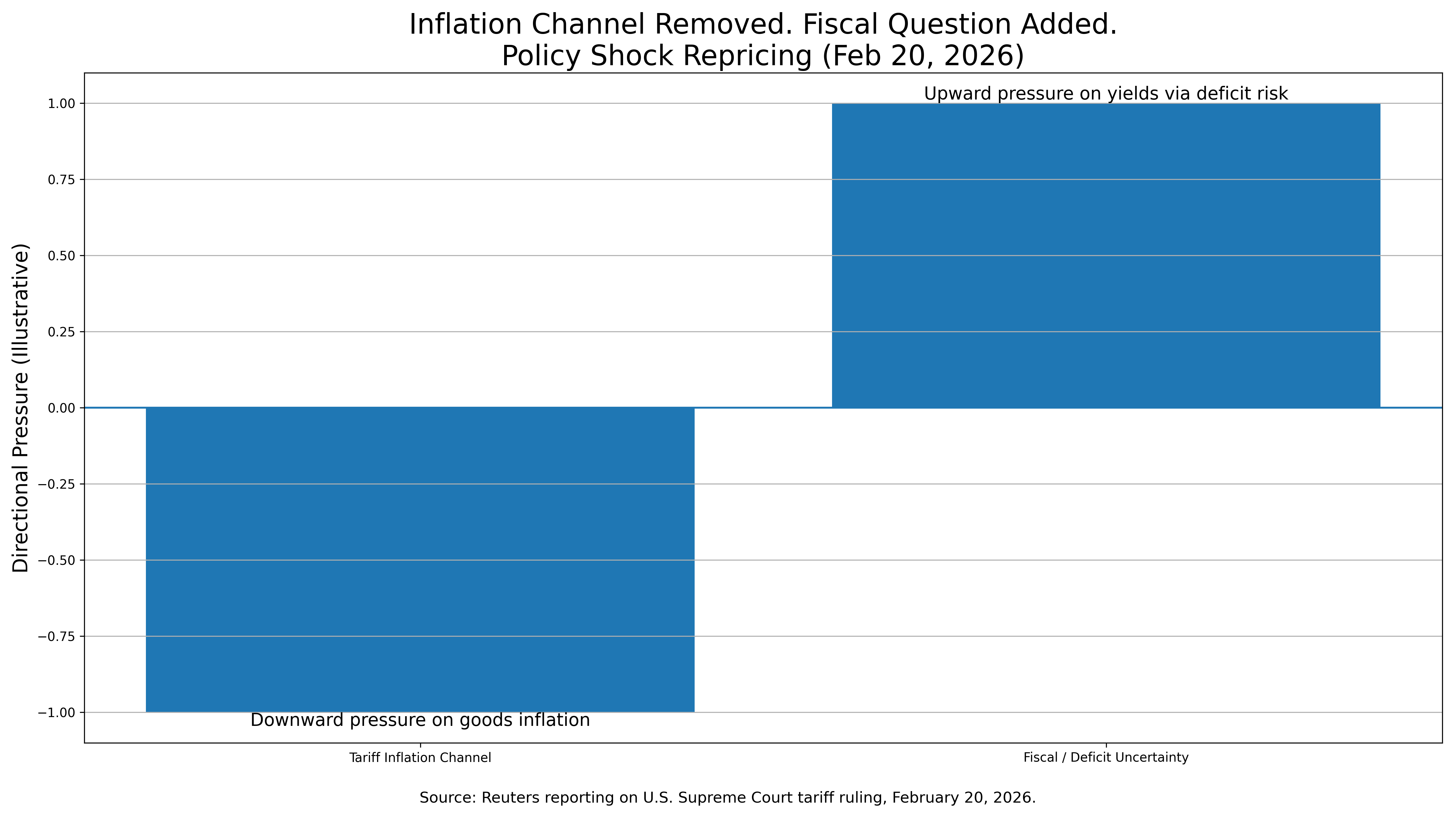

The U.S. Supreme Court struck down broad Trump-era tariffs, easing one inflation channel but raising fiscal uncertainty around potential refunds and deficit math.¹

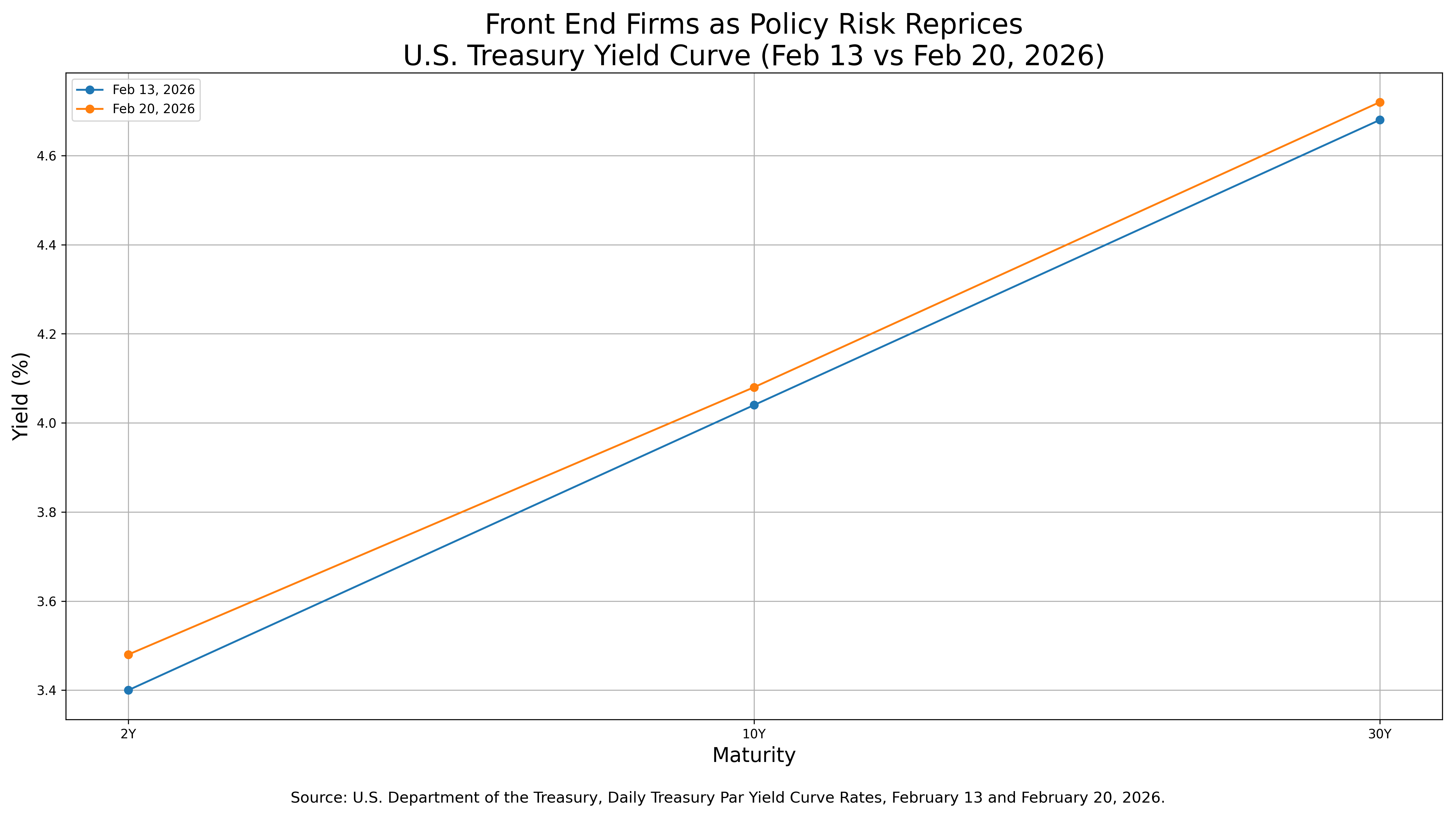

Treasury yields rose modestly, with the 2-year up more than the 10-year, reinforcing that the bond market is not pricing a clean disinflation pivot.²

Real GDP slowed to 1.4% annualized in Q4 2025, while inflation gauges in the same report remained firm.³

Fed minutes emphasized two-sided rate risks and explicitly tied tariffs to elevated core goods inflation.⁴

Equities rallied and volatility fell, but higher yields alongside the rally suggest fiscal repricing rather than pure policy relief.²

Surface Relief, Structural Tension

The headline was simple: markets rallied because tariff pressure appeared to ease.

The U.S. Supreme Court invalidated sweeping tariffs imposed during the Trump administration, a decision that in theory removes a direct inflationary channel.¹ Equities welcomed the news. Volatility fell. The tone shifted toward relief.

But Treasurys did not celebrate.

Yields drifted higher through the shortened holiday week. The front end rose more than the long end.² That subtle flattening matters. If this were purely a disinflation celebration, yields would likely have fallen across the curve.

Instead, the bond market focused on the second-order effects.

Reuters reporting highlighted concerns about potential tariff refunds and the fiscal implications if large revenue streams suddenly unwind.² Even as Treasury officials suggested alternative authorities could preserve tariff revenue, uncertainty itself became a premium embedded in yields.²

That is the shift.

A market can rally on the removal of a distortion while simultaneously demanding compensation for fiscal ambiguity. This week looked less like “inflation is gone” and more like “policy math is getting complicated.”

The macro backdrop added to the unease. Real GDP grew at just 1.4% annualized in Q4 2025, confirming a clear downshift in momentum.³ Yet inflation measures in that same report remained elevated relative to the Federal Reserve’s target.³ Slower growth with sticky price pressures is not the environment that invites an aggressive easing cycle.

The tape reflected that tension. Stocks moved higher. Rates firmed. That pairing rarely signals clean macro clarity.

The Fed’s Two-Sided Message

The Federal Open Market Committee minutes reinforced what the bond market already suspected.

Participants explicitly discussed tariffs as a contributor to higher core goods inflation.⁴ Some viewed the recent firmness in inflation as partially tariff-driven.⁴ Others cautioned that policy easing in the presence of elevated inflation could be misinterpreted as reduced commitment to the 2% target.⁴

Importantly, the minutes were not one-directional.

While some officials acknowledged disinflation progress, others raised the possibility of upward rate adjustments if inflation remains sticky.⁴ That language matters. It preserves optionality on both sides.

Markets sometimes assume that once growth slows, the Fed must cut. The minutes reject that simplicity. The rate path is conditional.

This explains why the front end of the curve rose modestly during a week of equity optimism.² Investors are not convinced that tariff removal automatically translates into easier policy.

The internal divergences tell the deeper story:

The dollar strengthened modestly during the week.²

Broad commodities rose as well.²

Credit spreads remained contained.²

The VIX closed below 20 but not at complacent extremes.²

A stronger dollar typically leans against commodity gains. Seeing both rise together hints at embedded inflation hedging. The market appears unwilling to fully abandon the inflation risk narrative.

At the same time, leadership within equities leaned cyclical. Financials and growth outperformed. Defensive utilities lagged.² That rotation is consistent with policy relief, but not necessarily with macro acceleration.