For as much as investors are focused on the big returns they’ve enjoyed since last week’s election, there’s one risk that seems to be flying under the radar. Again. That’s the reverse yen carry trade.

If it sounds familiar, it should. This is the event that knocked about 9% off of the S&P 500 and 14% off of the Nasdaq 100 over the course of about three weeks back in July & August. This is the event that sent the VIX above the 65 level, the third highest reading ever for the volatility barometer after only the COVID pandemic peak and the financial crisis.

And it looks like we could be headed for a repeat.

First, a little background.

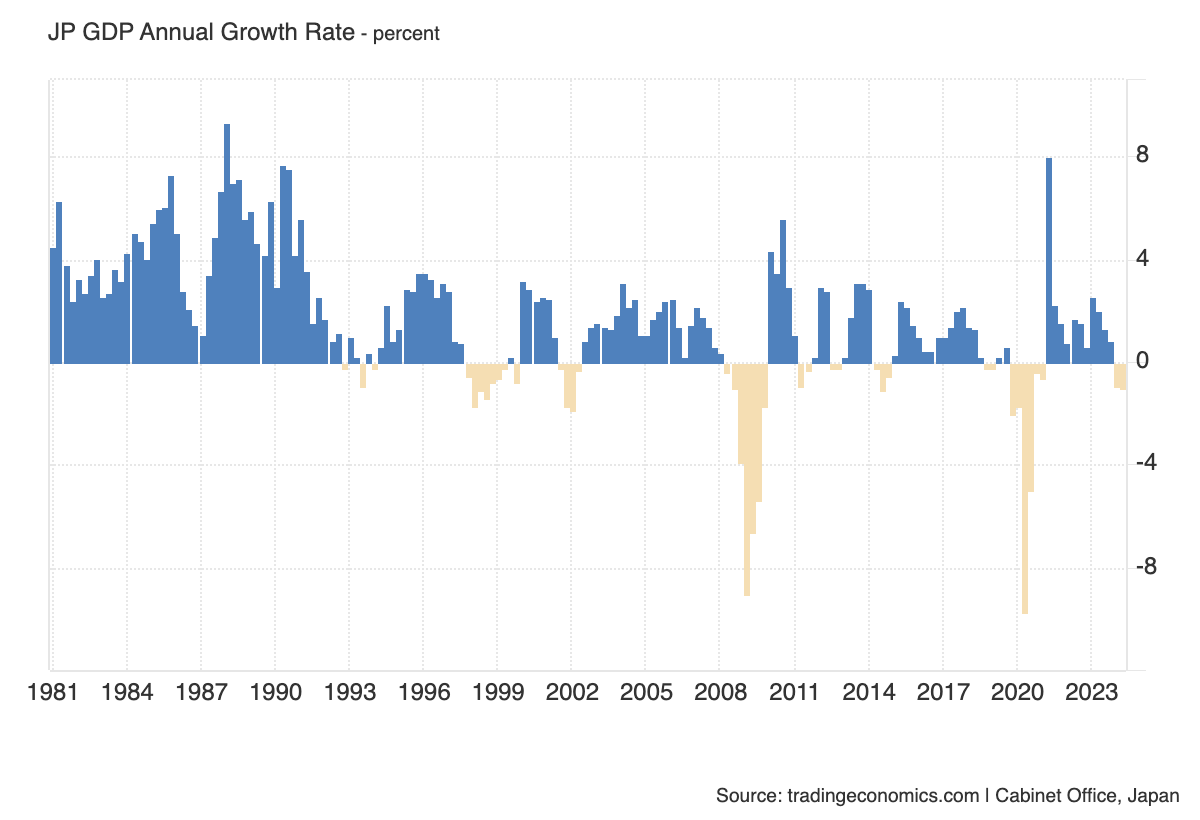

For years, the Japanese government has kept monetary conditions ultra-loose in order to ignite an economic revival. For the most part, it’s failed to deliver any consistent results. The economy has had its periods of ups and downs, but you’d have to go back to the early- to mid-2000s to find a time when the economy was consistently growing at a 2% rate. Before that, you’d have to look at the ‘80s and ‘90s.

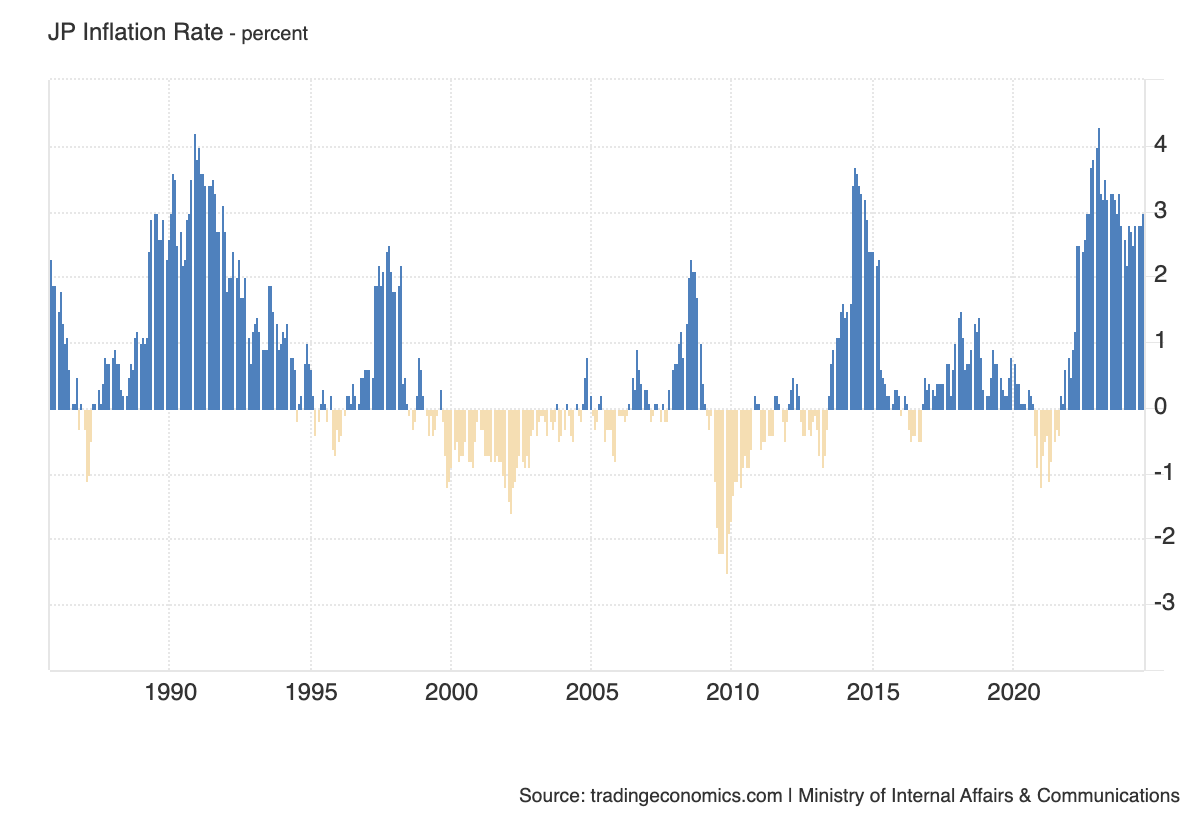

While growth has been very hit or miss, the Bank of Japan has been able to keep interest rates ultra-low because inflation hasn’t really been a threat.

Today, however, that dynamic is changing. The annualized inflation rate in Japan has been consistently running north of 2.5% since early 2022, including a peak of more than 4% in early 2023. This would mark the longest stretch of sustained high inflation since the late 1980’s and into the early 1990s.

This presents a big problem for the BoJ, although one that’s familiar to other global central banks - do you adjust policy to try to improve economic growth or to contain inflation?