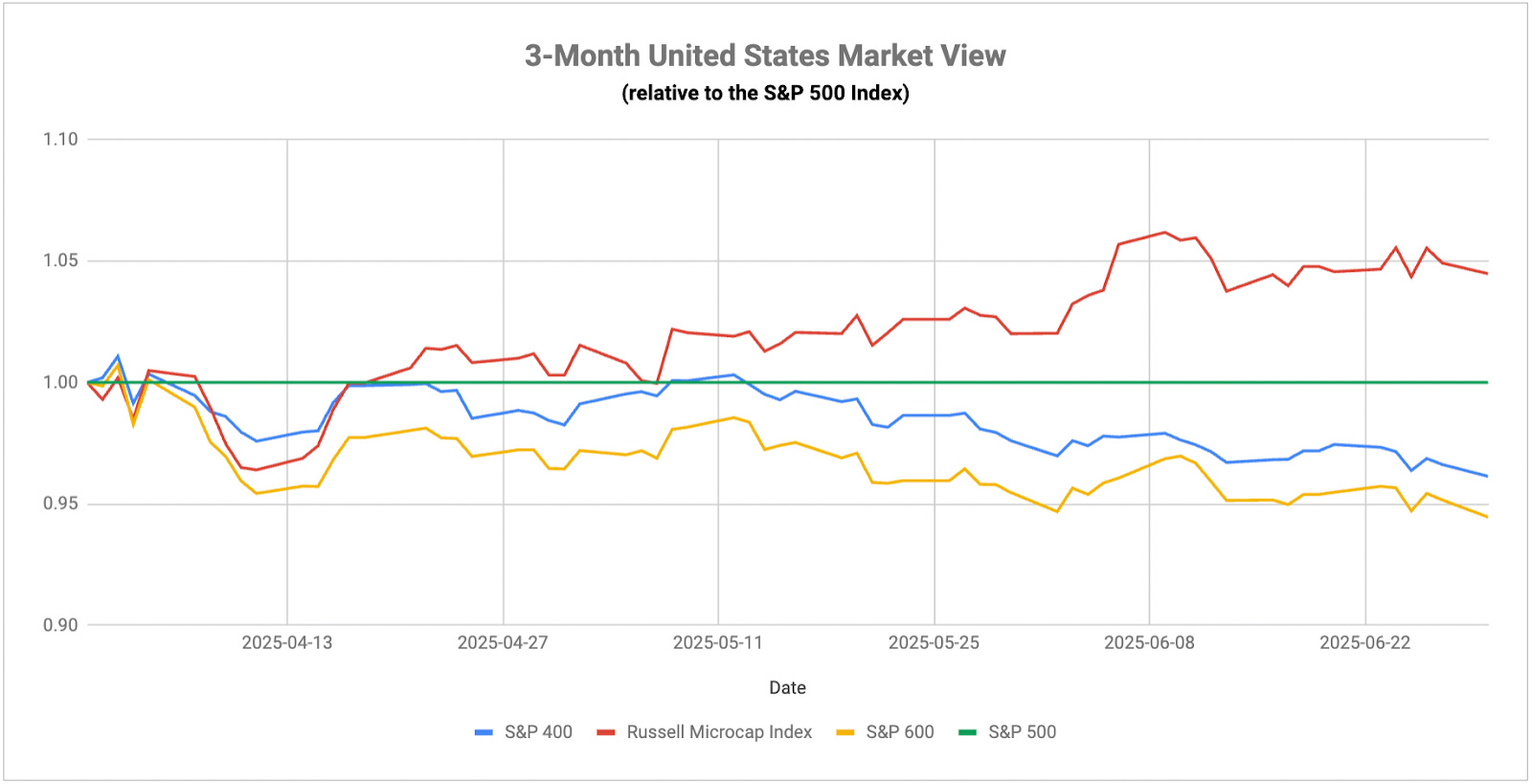

The above chart has become really interesting. We know that in isolation interest rate cuts should benefit smaller companies because they tend to be more reliant on financing for growth. In the post-Liberation Day environment, small-caps have consistently trailed large-caps, even when the Fed began signaling a greater likelihood that rate cuts would be coming soon. Small-caps and mid-caps continue to lag, but micro-caps have actually been steadily outperforming the S&P 500. Is this a sign that small-caps actually are outperforming? The outperformance trend did start right around the time that investors began getting more optimistic about rate cuts. Most view this as a large-cap driven market. Perhaps, it’s really a barbell.

The Senate has narrowly managed to pass Trump’s “Big Beautiful Bill” after much late-night wrangling. Now it’s headed back to the House where it needs to get through a chamber that looks like it doesn’t have the votes to pass in its current iteration. The market continues to weigh the impact of what could ultimately be a multi-trillion addition to the nation’s deficits. Given the bullish trend over the past couple weeks and modest volatility, it feels like the bill’s fiscal risks are priced in. It seems likely that some version of this bill will eventually and, while it might not necessarily result in a swift crash in equities, it should accelerate the ongoing concerns that U.S. debt is unsustainable and the dollar, in particular, is vulnerable to a further correction.

Short-term attention now pivots to Jerome Powell, the Fed and the next meeting at the end of July. As it stands right now, the market is pricing in just a 21% chance of a rate cut at this meeting, but a 92% chance of one by September. It’s also pricing in a 60% chance of 3+ rate cuts by the end of this year. Rate cut bets have picked up significantly ever since Powell changed his tone and acknowledged that the central bank could be closer to feeling it has the justification to normalize monetary conditions with inflation relatively subdued. That’s been the driving factor of the S&P 500’s push to new highs. The longer-term bull catalyst from the Fed is the proposed reduction to the SLR, which could free up hundreds of billions of dollars to be put to work by the big banks. Deregulation has been one of the biggest potential tailwinds for risk assets throughout the Trump presidency. It looks like the first of these major deregulatory efforts is already in process with more likely on the way.

The Eurozone inflation rate for June is back to 2%, officially hitting the ECB’s target level, while the core rate came in only slightly higher at 2.3%. While the rent and services inflation rates are still hovering around the 3% level, it’s pretty clear that inflation is for the most part under control in Europe. In May of last year, the ECB’s benchmark rate was 4.5%. Today, it’s at 2.15%. With the headline rates falling back to target, it seems like an ideal stopping point for the central bank’s rate cutting cycle for now. The recovery in Europe is still in a tenuous spot and it’ll be interesting to hear the rhetoric around where Lagarde and company see the economy headed over the next 12 months. Any hints at further rate cuts from here could be viewed as an implicit admission that macro conditions could be deteriorating.