The 12% Monthly Paycheck That the IRS Can't Touch Until You Sell

NEOS S&P 500 High Income ETF (CBOE: SPYI) — $10 Billion in Assets, 12% Yield, and a Tax Structure That Changes the Income Equation

Special Announcement

The Relative Sentiment Tactical Allocation ETF is a flexible, multi-asset fund that invests across stocks, bonds, commodities, precious metals, and currencies. Its approach is guided by a research-based factor called relative sentiment—which tracks how optimistic or cautious professional investors are compared to individual investors. Studies show professionals tend to have an edge over time, and this ETF seeks to capture that insight by increasing exposure to areas where institutions are more optimistic and reducing exposure where they’re more cautious. Relative sentiment often complements trend-following strategies, helping create portfolios that may be more balanced and less prone to sharp swings.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. This and other important information is contained in the prospectus, which may be obtained by following the links Prospectus and SAI or by calling +1.215.882.9983. Please read the prospectus carefully before investing.

Investments involve risk. Principal loss is possible.

The Fund is distributed by PINE Distributors LLC.

ETFAC-4976143-11/25

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Relative Sentiment. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Relative Sentiment. and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Last week, we profiled JEPI — JPMorgan’s $45 billion covered call ETF — as the dominant force in options-based income investing. This week, I want to introduce you to the fund that has been quietly eating JEPI’s lunch.

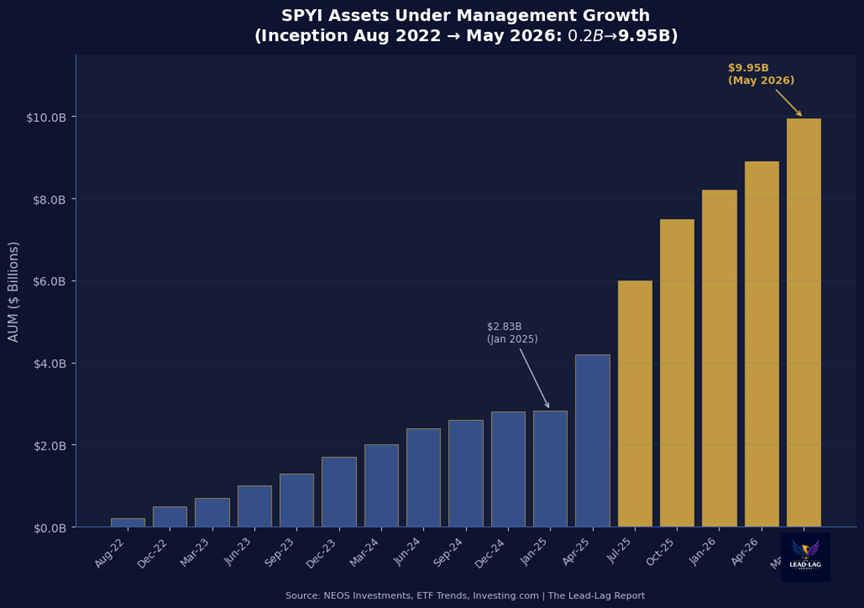

The NEOS S&P 500 High Income ETF (CBOE: SPYI) launched in August 2022 with a structure so deliberately different from every covered call ETF before it that it took the market two full years to notice. By January 2025, SPYI had $2.83 billion in assets. By May 2026, it crossed $10 billion. That is a 3.5x increase in 16 months — the kind of asset growth that happens when a product solves a genuine problem the market had been ignoring.

The problem it solves is taxes. And the solution is elegant enough that it deserves a full examination.

Fund Background

SPYI is an actively managed ETF that holds all 500 constituents of the S&P 500 Index in full replication, and overlays a call spread strategy using SPX index options — not options on individual stocks, not equity-linked notes, not synthetic derivatives. Plain index options, written on the index itself.

That structural choice is not cosmetic. It is the entire reason SPYI works the way it does.

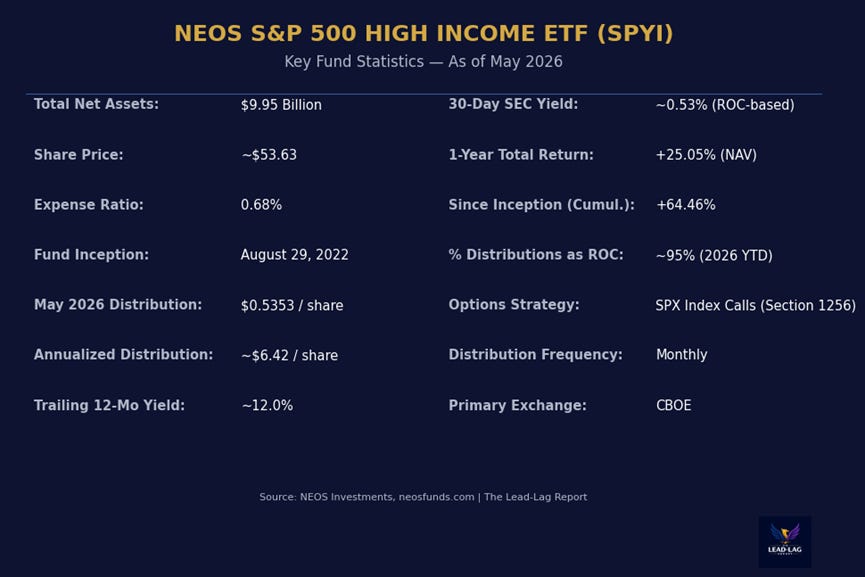

Fund Name: NEOS S&P 500 High Income ETF

Ticker: SPYI (CBOE)

Fund Inception: August 29, 2022

Total Net Assets: $9.95 Billion

Share Price: approximately $53.63

Expense Ratio: 0.68%

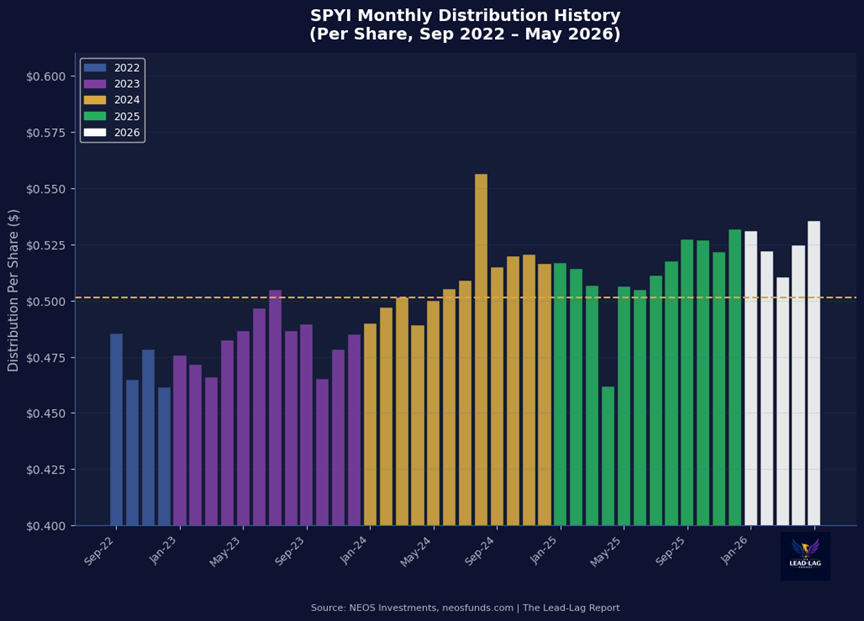

Monthly Distribution (May 2026): $0.5353 per share

Annualized Distribution: approximately $6.42 per share

Trailing 12-Month Yield: approximately 12.0%

30-Day SEC Yield: approximately 0.53% (low because most income is classified as return of capital)

Distribution Frequency: Monthly

Primary Exchange: CBOE

Options Strategy: SPX Index Call Spreads (Section 1256 Contracts)

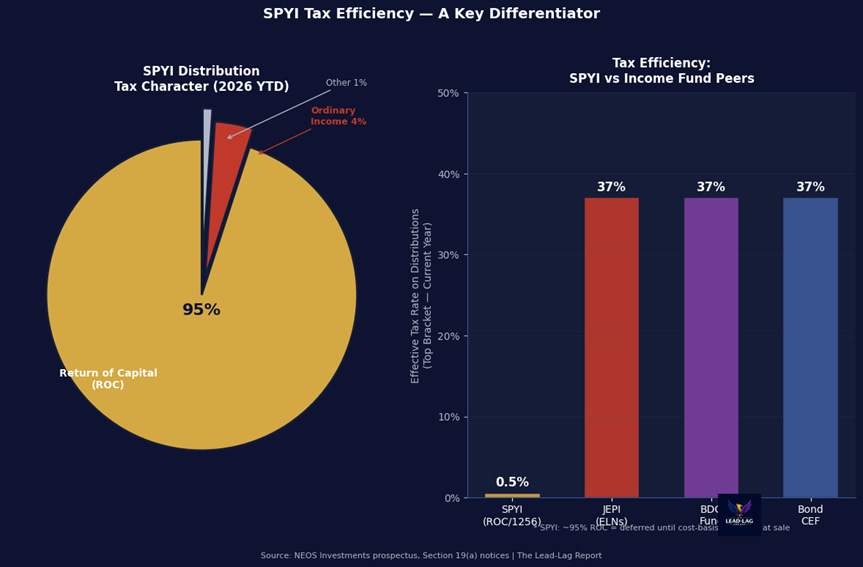

% of 2026 YTD Distributions as ROC: approximately 95%

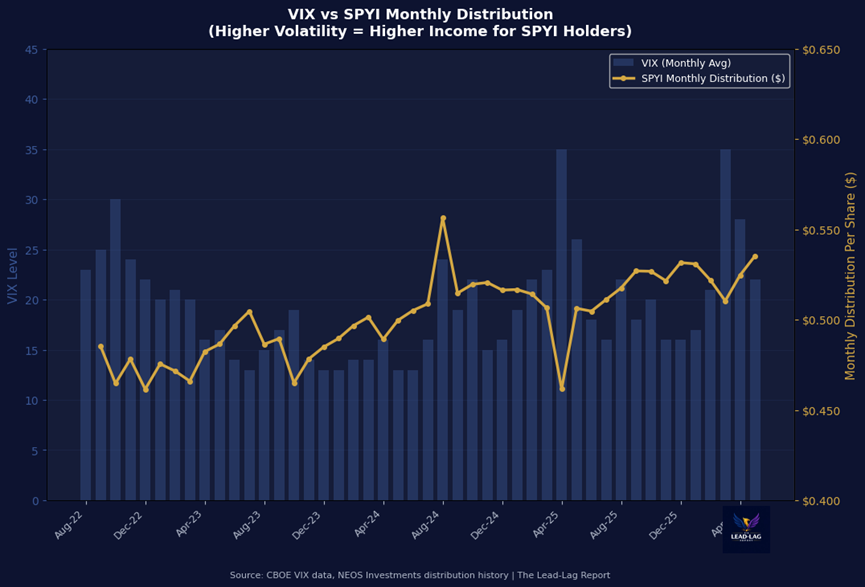

The strategy works as follows. NEOS purchases all the stocks in the S&P 500. Then it writes out-of-the-money call options on the S&P 500 index (SPX) — not on the individual stocks it holds — collecting a premium. It takes a portion of that premium and purchases even further out-of-the-money calls, creating a call spread. The net credit from that spread becomes the primary source of SPYI’s distributions. Because the options are written on the index rather than individual positions, they qualify as Section 1256 contracts under the IRS tax code.

Section 1256 contracts receive favorable tax treatment: any gains are treated as 60% long-term and 40% short-term, regardless of how long the positions were held. NEOS then actively harvests losses within the equity portfolio throughout the year, which has allowed the fund to classify approximately 95% of its 2026 year-to-date distributions as return of capital.

What’s Actually in the Portfolio

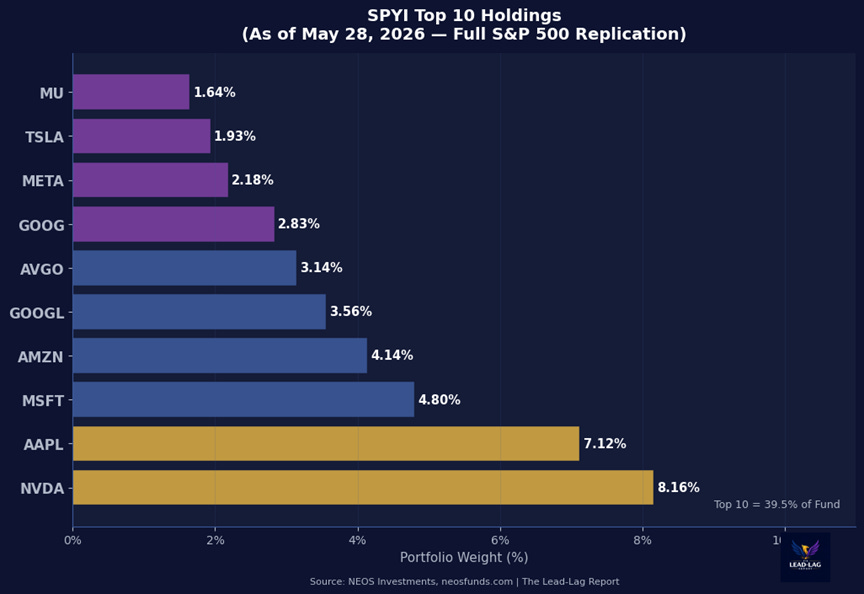

SPYI holds all 503 companies in the S&P 500, weighted by market capitalization. There is no stock selection, no factor tilt, no low-volatility screen. The equity sleeve is pure index replication.

Technology accounts for approximately 33% of the fund, financials approximately 12.6%, and communication services approximately 10.3%. The top ten holdings represent 39.5% of fund assets.

In other words, the very companies that make the S&P 500 nerve-wracking to hold passively — the ones that spike and crash on AI earnings, regulatory news, and capex announcements — are actively working to fund SPYI’s distributions. The volatility you dread as an equity investor becomes the raw material SPYI converts into monthly income.

Historical Performance

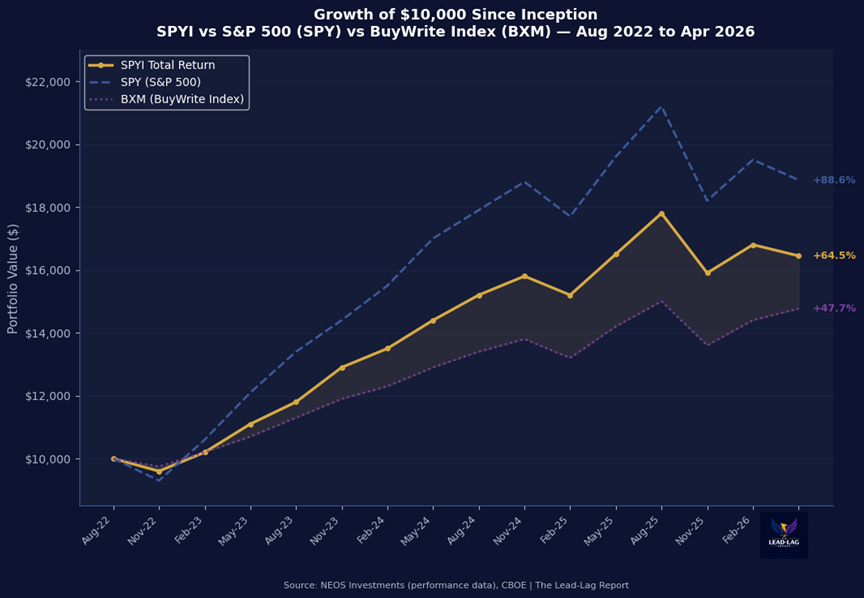

SPYI’s since-inception cumulative total return through April 30, 2026 was 64.46%, versus the S&P 500’s 88.57% over the same period. That is the explicit cost of the income overlay — the fund underperforms pure index exposure during bull markets, particularly during the straight-up rallies of 2023 and 2024.

But the comparison changes materially in choppy and volatile markets. Over the six months ending April 2026 — a period defined by tariff uncertainty, geopolitical tension, consumer confidence deterioration, and range-bound equity action — SPYI delivered 5.42% total return versus the S&P 500’s approximately 4.6%.

Over the trailing twelve months through April 2026, SPYI delivered a 25.05% total return — ahead of JEPI’s approximately 14% and substantially ahead of the CBOE BuyWrite Monthly Index’s 17.52%. SPYI also significantly outperformed in 2025, delivering approximately 16.6% total return versus JEPI’s approximately 8%.

Distribution Policy

SPYI pays a monthly distribution on a fixed schedule, declared mid-month for payment at month-end. The distribution amount is variable — it moves with the options premiums the fund collects, which move with VIX. This is not a fixed payout promise.

The May 2026 distribution of $0.5353 annualizes to $6.4236, producing a trailing twelve-month yield of approximately 12% at the current share price of $53.63. Since inception, distributions have drifted upward from $0.46/month to $0.53/month — a 15% increase — with no significant cuts even during sharp market declines.

Tax Efficiency — The Real Story

When JEPI pays you $0.44 per share per month, that payment is taxed as ordinary income in the year you receive it. For an investor in the 37% federal bracket, that effective tax drag is 37 cents per dollar distributed. On $12,000 in annual distributions from a $100,000 position, you owe $4,440 in federal income tax in the year you receive the income.

When SPYI pays you $0.5353 per share per month, approximately 95% of that payment is classified as return of capital. You owe no federal income tax on the return of capital portion in the year you receive it. On the same $12,000 in annual distributions, your current-year federal tax bill is approximately $60.

NEOS’s own data confirms this: the one-year after-tax return on distributions through March 2026 was 14.80% versus the 16.35% pre-tax return — a drag of only 1.55 percentage points. JEPI’s equivalent tax drag is approximately 3-4 percentage points per year.

Advantages

SPYI delivers approximately 12% monthly income from an S&P 500 portfolio while utilizing a tax structure that allows most shareholders to defer federal income tax on their distributions until they sell. The combination of high yield and tax efficiency is structurally unusual — most high-yield instruments are also high-tax instruments.

The call spread architecture preserves some equity upside. Unlike traditional covered call ETFs that fully cap participation above the call strike, SPYI’s purchased upper calls allow shareholders to benefit when the S&P 500 rallies strongly. During the 2025 AI-driven recovery, SPYI participated meaningfully while XYLD holders watched from behind a capped ceiling.