The BDC Bubble Hiding in Plain Sight

Yield as Sedation: How a 13% Coupon Silences the Questions Consensus No Longer Wants to Ask

Today’s Lead-Lag Report post is sponsored by Evoke

The future is highly uncertain, with potential challenges in growth, inflation, and geopolitics, making diversification crucial.

Most investors are unknowingly underdiversified. A traditional 60/40 portfolio is 98% correlated to the stock market, potentially exposing investors to more risk than they realize. The S&P 500 historically experienced extended periods of underperformance, including:

1. Underperforming cash from 1966 to 1982 during inflationary times

2. A 0% average return from 1929 to 1949

3. A lost decade prior to the recent 15-year bull market

Historical bear markets often started with high valuations. Given current high valuations, we may be on the verge of another challenging period for U.S. equities.

Risk parity seeks to offer a more diversified allocation than conventional mixes. By spreading risk across global equities, Treasuries, TIPS, and commodity producers and gold, investors can maintain a low-cost, tax-efficient passive mix seeking:

1. Equity-like long-term expected returns

2. Lower risk than stocks

3. Reduced risk of a lost decade

To learn more about the RPAR Risk Parity ETF, visit rparetf.com.

Before investing you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. This and other information is in the prospectus. A prospectus may be obtained by clicking here. Please read the prospectus carefully before you invest.

Investing involves risk. Principal loss is possible.

Distributed by Foreside Fund Services, LLC.

Data source: Bloomberg.

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Evoke Advisors. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Evoke Advisors and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

The BDC Bubble Hiding in Plain Sight

A yield does one thing better than any other number on a page. It sedates. Show an income investor a steady double-digit coupon and a chart of net asset value that barely moves, and the questions stop. Where does the cash actually come from. What is the collateral worth if it has to be sold rather than modeled. What happens to the marks when the credit cycle turns and the buyer of last resort is also the seller. Business Development Companies have spent five years answering none of those questions, because the yield answered them first. That is the function of sedation. It is not that the questions have been resolved. It is that the coupon made them feel impolite to ask.

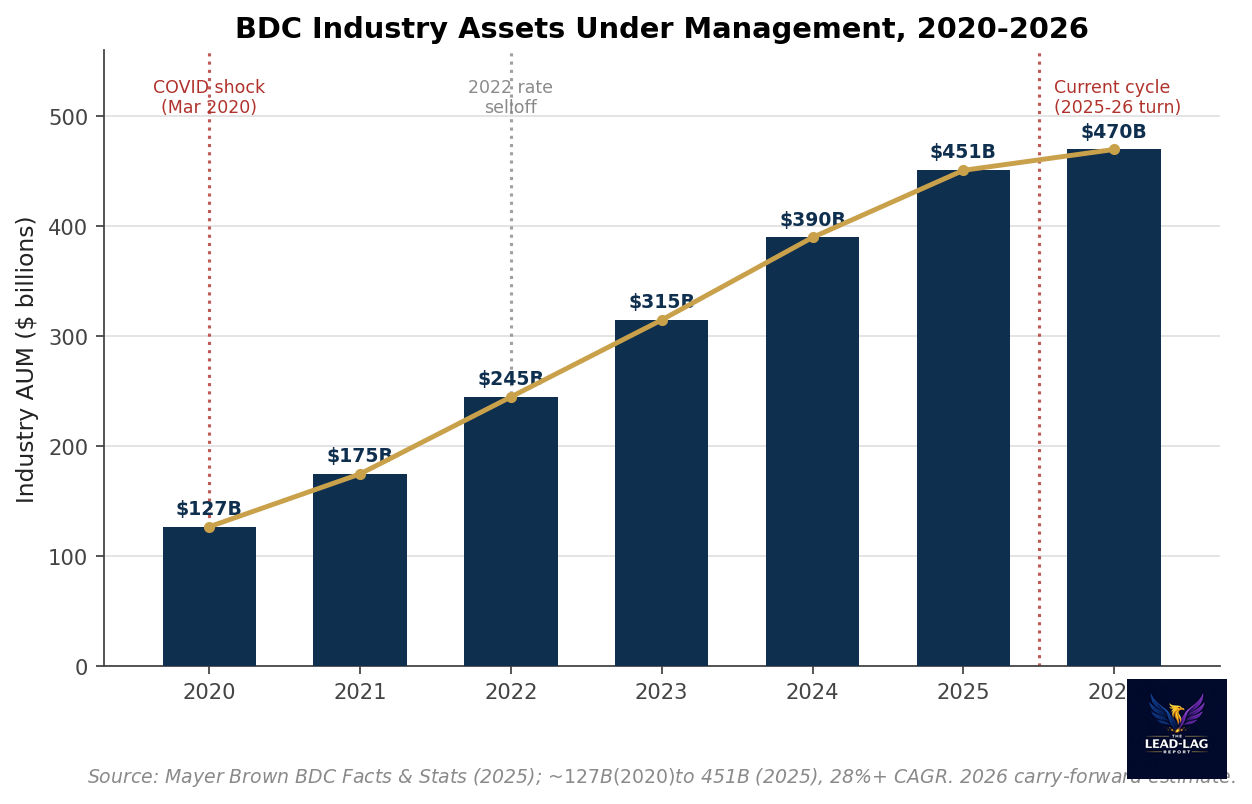

The asset class has grown into the role. Industry assets under management for BDCs expanded from roughly $127 billion in 2020 to approximately $451 billion in 2025, a compound annual growth rate north of 28 percent.[1] The broader private credit market it feeds is now estimated above $1.7 trillion.[2] That growth did not happen because middle-market lending suddenly became safer. It happened because the yield was loud enough to be marketed as a Treasury substitute, and quiet enough about its risks to be slotted into the income sleeve of advisor portfolios alongside short-duration government paper. This piece is not about whether any single BDC is mispriced. It is about the regime, and about what a 13 percent yield is actually compensating you for at this point in the cycle.

KEY HIGHLIGHTS

• BDC industry AUM grew from ~$127B (2020) to ~$451B (2025), a 28%+ CAGR, while the underlying asset is the same late-cycle leveraged loan it always was.

• BXSL carries an ~11.7% yield on NAV and trades near or below book value; MAIN trades at roughly 1.6x NAV with a far lower headline price yield. The dispersion itself is the signal.

• The Houlihan Lokey BDC Monitor put the publicly traded BDC non-accrual rate at 1.4% as of Q4 2025, with PIK income at large BDCs near 8.2% of investment income in Q1 2026 and rising.

• High-yield OAS closed near 2.78% in late June 2026, within a hair of the 2007 record low, while leveraged loan default measures are inflecting higher — the exact configuration BDCs are most exposed to.

• In 2008-2009 the BDC sector saw assets shrink 30%+ and roughly 80% of surviving BDCs cut or suspended distributions; in March 2020 the sector fell ~50% in three weeks before NAVs were marked down a quarter later. The pattern is the point.