The Bounce, the Barrel, and the Bet Nobody Wants to Make

Can a Market Rally Survive When the Price of Oil Is Still the Price of Everything?

Key Highlights

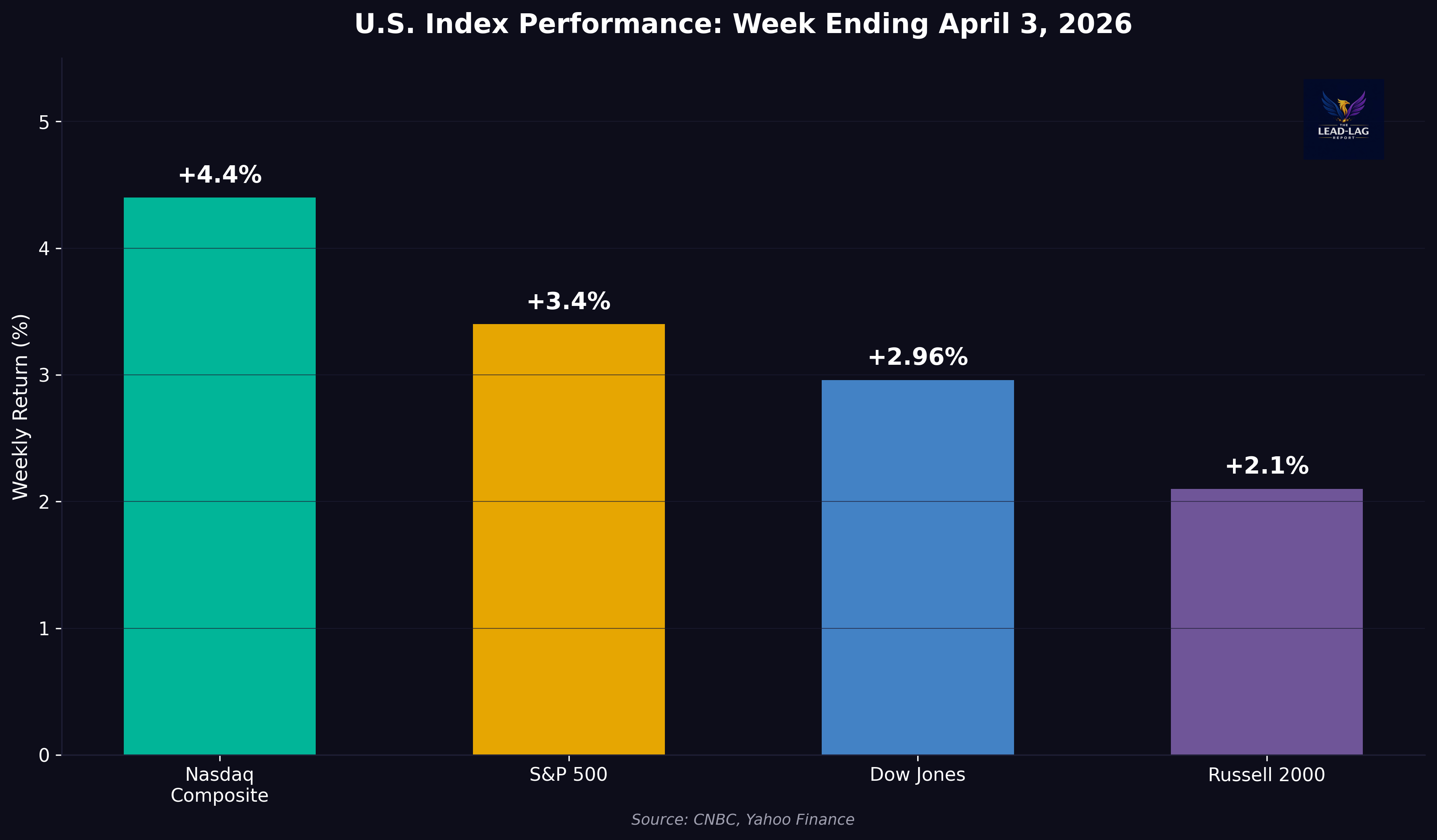

The S&P 500 surged 3.4% for the week, snapping its five-week losing streak in the best weekly performance since May, while the Nasdaq rallied 4.4% and the Dow gained nearly 3%.

WTI crude jumped 12% on Thursday alone after Trump's primetime address offered no plan to reopen the Strait of Hormuz, closing the week near $112 per barrel.

Nonfarm payrolls surprised to the upside at 178,000 in March, nearly triple the consensus estimate of 59,000, though the three-month average has slowed to just 68,000.

High-yield BB spreads tightened sharply to 1.98%, their lowest level since before the war began, even as Brent crude touched $112 and the April 6 deadline for Iranian energy strikes remained in force.

The Surface Narrative

For the first time in six weeks, the Dow Jones Industrial Average closed higher for the week. The S&P 500 gained 3.4%, its best weekly return since May, while the Nasdaq Composite surged 4.4%. The rally was concentrated in the first half of the holiday-shortened week, fueled by a sequence of diplomatic signals that briefly convinced markets the U.S.-Iran war might be approaching some form of resolution. On Tuesday, an unverified report suggested that Iran’s President Pezeshkian was amenable to ending the conflict under certain conditions. On Wednesday, Trump stated publicly that U.S. forces could withdraw within “two to three weeks.”

The optimism was short-lived. Trump’s Wednesday evening primetime address was filled with escalatory language, offering no concrete plan to reopen the Strait of Hormuz and vowing more aggressive action against Iran in the coming weeks. WTI crude, which had been declining earlier in the week, surged 11.4% on Thursday in response. Brent settled near $112 per barrel. For the four-day trading week, oil recorded its sixth positive week in seven, rising nearly 12%. The market opened sharply lower on Thursday morning, with the Dow falling more than 600 points, before staging an unlikely recovery on reports that Iran and Oman had agreed to a protocol for monitoring transit through the Strait. The S&P 500 and Nasdaq both closed marginally higher that day, a move that Jim Cramer called “stunning, surreal” given where oil ended.

The Friday jobs report capped the week with another surprise. Nonfarm payrolls rose 178,000 in March, nearly triple the Dow Jones consensus estimate of 59,000. Health care added 76,000 positions, reflecting the return of Kaiser Permanente nurses from a February strike. Construction added 26,000. The unemployment rate ticked down to 4.3%. But the headline number masked a more important trend: the three-month average has slowed to just 68,000, federal government employment is down 355,000, or 11.8%, from its October 2024 peak, and February’s figure was revised further into negative territory at minus 133,000.

Figure 1: The S&P 500, Nasdaq, and Dow all posted their strongest weekly gains since May, snapping a five-week losing streak.

The Real Catalyst

The real catalyst for last week's rally was not peace. It was the market's decision, however tentative, to stop pricing for the worst-case scenario and begin pricing for ambiguity. That is a meaningful distinction. Pricing for ambiguity means accepting that oil could go to $150 or fall to $85, that the Strait could reopen this week or remain closed through summer, and that the correct response is not maximum defensiveness but something closer to neutral positioning. The fact that stocks rallied even as oil surged on Thursday is the strongest evidence that this shift in psychology has taken hold.

The 10-year Treasury yield offered confirmation. After hitting 4.44% on March 27, its highest level since July 2025, the yield retreated to 4.31% by midweek. That 13 basis point decline in a single week, occurring against the backdrop of rising oil prices, suggests the bond market is beginning to differentiate between a permanent inflation shock and a temporary supply disruption. Whether that distinction holds will depend on the March CPI data due this Friday, which will be the first to capture any war-related effects. FactSet consensus estimates project headline CPI at 3.1% year-over-year and core at 2.4%.

The credit market was even more decisive. BB-rated high-yield spreads tightened to 1.98% on April 2, down from 2.22% just three days earlier and their tightest level since before the war began on February 28. This is a remarkable signal. Credit markets are not naive. They are, historically, better predictors of economic stress than equity markets. When credit says the fundamentals are intact even as equities panic, credit is usually right. The current tightening suggests that despite oil at $112, institutional fixed income investors do not see a meaningful increase in default risk.