The CLO Income Play That Doesn't Blow Up

How the Panagram BBB-B CLO ETF delivers a 7.5% yield with a floating-rate profile that thrives in a higher-for-longer world.

SPECIAL ANNOUNCEMENT

Today’s Lead-Lag Report is brought to you by our friends at Alexis Investment Partners — the father-daughter RIA and ETF issuer behind the Practical Tactical framework and the NASDAQ-listed Alexis Practical Tactical ETF (LEXI).

High valuations and an aging secular bull market threaten to re-assert sequence of returns risks that can ravage retirement income plans. Practical Tactical was built for this — a multi-asset, model informed framework managed by Jason Browne and Alexis Browne Roberts, seeking to add value through market cycles by:

• Participating more in up than down markets

• Pursuing leading sectors and regions and minimizing exposure to laggards

• Incorporating a broader range of asset classes and strategies than traditional balanced portfolios

That framework is wrapped in an ETF — a tax efficient tactical allocation sleeve advisors can use to complement strategic portfolios.

To learn more about the ETF, visit www.lexietf.com. Access AIP’s media content, monthly newsletter and learn more about practical tactical investing at www.alexisinvests.com.

Before investing carefully consider the fund’s investment objective, risks, charges, and expenses contained in the prospectus available at www.lexietf.com. Please read the prospectus carefully.

Investing involves risk including possible loss of principal.

Distributor: Foreside Fund Services, LLC

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Alexis Investment Partners. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Alexis Investment Partners and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

The CLO Income Play That Doesn't Blow Up

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Macro and Market Context

A few weeks ago, this column profiled Eagle Point Credit Company, and the response was overwhelming. Readers are clearly hungry for collateralized loan obligation income, and for good reason. The CLO market offers some of the most attractive risk-adjusted yields available anywhere in fixed income. The problem is that most retail vehicles reaching for the highest headline yields do so by owning the riskiest slice of the capital structure, and when the cycle turns, that slice gets devastated. There is a smarter way to own CLO exposure, and it is what sophisticated institutional credit investors actually hold.

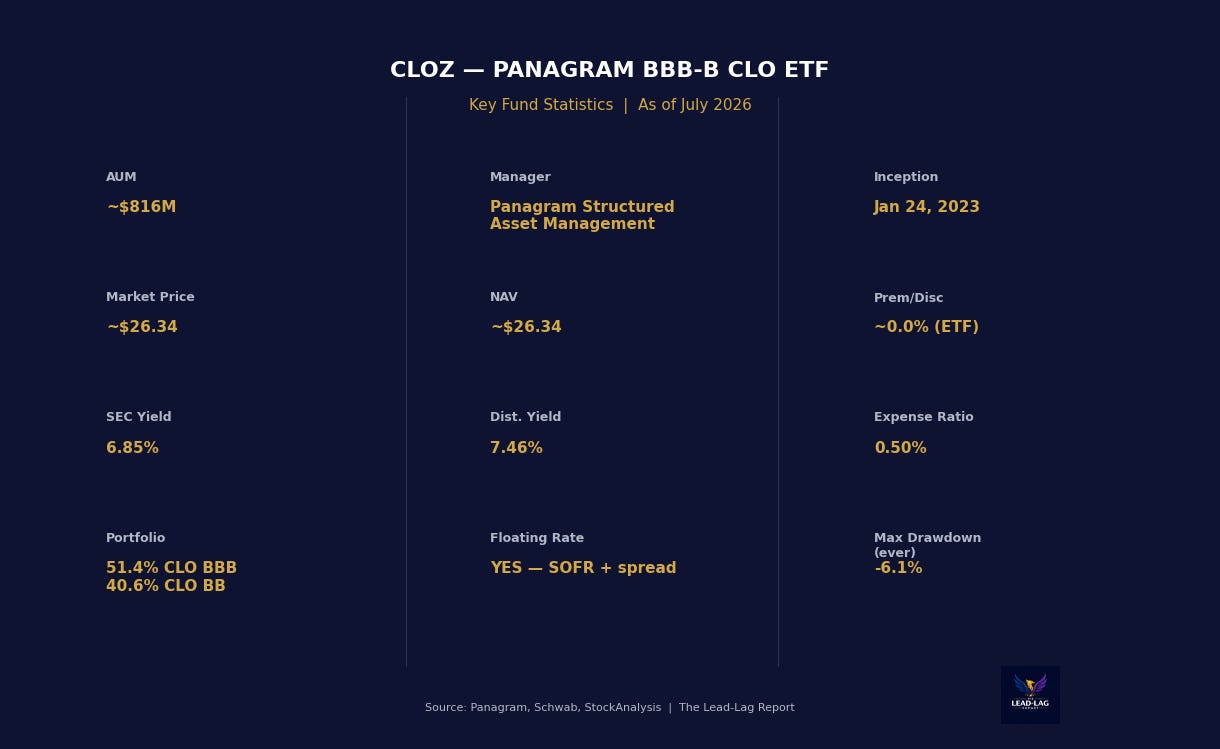

The Panagram BBB-B CLO ETF (CLOZ) is built around that exact idea. Rather than chasing the equity tranche of a CLO, which sits at the very bottom of the waterfall and absorbs the first dollar of loss, CLOZ owns the BBB and BB rated mezzanine tranches. These sit higher in the structure, are protected by layers of subordination beneath them, and still pay a floating coupon of SOFR plus a spread. The result is a fund that currently distributes roughly 7.5% while carrying a maximum historical drawdown of just 6.1%. That is a rare combination in the income world.

The macro backdrop makes this fund especially interesting right now. With Kevin Warsh at the helm of the Federal Reserve, the rate trajectory is genuinely uncertain, and the higher-for-longer scenario remains very much alive. For most income vehicles, that is a threat. For CLOZ, it is a tailwind. Because the fund’s holdings pay a floating rate tied to SOFR, a Fed that holds or hikes actually means more income flowing to shareholders, not less. This is the mirror image of the rate-sensitive REIT and preferred-stock funds that suffer when the Fed stays restrictive. CLOZ is the fund that benefits from the same environment that hurts them.

Fund Background

Full name: Panagram BBB-B CLO ETF, formerly the Eldridge BBB-B CLO ETF.

Ticker and exchange: CLOZ, listed on NYSE Arca.

Structure: An actively managed exchange-traded fund, not a passive index tracker and not a closed-end fund, so it trades at or very near net asset value rather than at a persistent premium or discount.

Manager: Panagram Structured Asset Management, a specialist in structured credit.

Inception: January 24, 2023, giving the fund roughly three and a half years of track record.

Assets under management: Approximately 816 million dollars across 203 individual CLO tranches.

Expense ratio: 0.50%.

Benchmark: The JP Morgan CLO High Quality Mezzanine Index.

Price and NAV: The shares recently traded around 26.34 dollars, essentially flat to NAV, within a 52-week range of 25.23 to 26.95 dollars.

Yield: A 30-day SEC yield of 6.85% and a distribution yield of 7.46%, paid through monthly distributions of roughly 0.171 dollars per share, or about 2.02 dollars annually on a trailing basis.

Rate profile: Floating rate, SOFR plus spread, which means effectively no duration risk.

- Paid Subscriber Content -