The Credit Market Has a Fear Problem Right Now. This 10% Yielder Is Built for It.

Ares Dynamic Credit Allocation Fund (NYSE: ARDC) — When the World's Largest Credit Manager Runs Your CEF

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

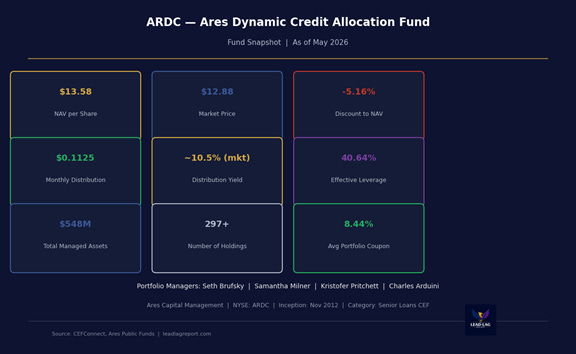

ARDC Fund Snapshot — As of May 2026 | Source: CEFConnect, Ares Public Funds

────────────────────────────────────────────────────────────

The credit markets in May 2026 are a study in contradictions. Tariff uncertainty, recession whispers, and a Fed that has cut rates cautiously but not boldly enough to reassure anyone — and yet spreads are still relatively contained, corporate defaults remain manageable, and floating-rate income is still paying well. In this environment, the question for income investors is not whether to own credit. It is which credit manager to trust with your money.

That question has a compelling answer: Ares Management. With over $622 billion in AUM globally and a credit investment team of 560+ professionals covering roughly 4,000 portfolio companies, Ares is not just a large credit manager — they are one of the architects of the modern leveraged credit market. When they run a closed-end fund, they do it with information and access that a typical retail credit investor simply cannot replicate.

The fund in question this week is the Ares Dynamic Credit Allocation Fund (NYSE: ARDC), currently trading at a -5.2% discount to NAV and yielding approximately 10.5% at market price. The setup is interesting: a wide discount, a strong management platform, and a portfolio actively rotating across senior secured loans, high yield bonds, and CLO securities to navigate exactly the kind of uncertain credit cycle we are in right now.

────────────────────────────────────────────────────────────

Fund Background

ARDC launched in November 2012 with a mandate to “seek an attractive risk-adjusted level of total return, primarily through current income, and secondarily through capital appreciation.” What makes this fund different from a static credit CEF is in its name: dynamic allocation. Ares rotates the portfolio actively across four credit buckets — senior secured loans, corporate bonds, CLO debt, and CLO equity — based on where the risk/return tradeoff is most favorable at any given time.

As of January 2026, the portfolio breakdown was: loans (41.8%), corporate bonds (33.3%), CLO debt (18.1%), and CLO equity (10.5%). The short effective duration of 1.24 years is striking — this is not a fund taking big duration risk. The floating-rate component (63.2% of the portfolio) means the fund benefits from elevated short-term rates and is insulated from rate volatility in ways a traditional high-yield bond fund is not.

NAV per Share: $13.58

Market Price: $12.88

Discount to NAV: approximately -5.2%

Monthly Distribution: $0.1125 per share

Annualized Distribution Yield (market): approximately 10.5%

Annualized Distribution Yield (NAV): approximately 9.94%

Effective Leverage: 40.64%

Total Managed Assets: $548 million

Number of Holdings: 297+

Average Portfolio Coupon: 8.44%

Effective Duration: 1.24 years

Total Expense Ratio (including leverage costs): 5.26%

Inception Date: November 27, 2012

Portfolio managers: Seth Brufsky (35 years experience), Samantha Milner (25 years), Charles Arduini (25 years), Kristofer Pritchett (17 years).

— PAYWALL —

Why This Fund, Why Now

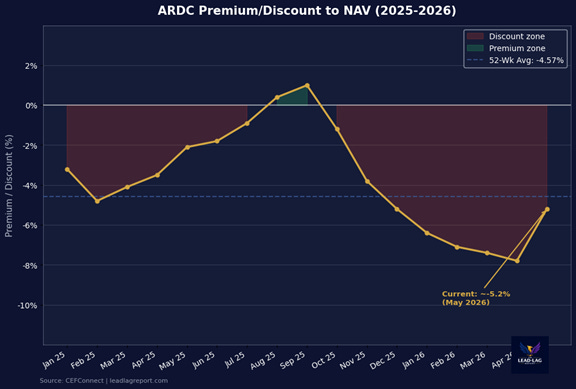

The credit cycle is at an inflection point. We have had two years of strong credit performance — ARDC posted +19.44% NAV return in 2023 and +11.80% in 2024 — riding the tailwind of elevated rates and tight spreads. But 2025 told a different story: NAV returned +6.79% while the price fell -3.07%. YTD 2026 through March, both are negative (-4.54% NAV, -6.14% price). The credit market has repriced risk, and ARDC’s discount has blown out from a 52-week high of +1.64% premium to the current -5.2% discount.

This is where it gets interesting. A -5.2% discount on a fund managed by the Ares credit platform — one of the most respected credit organizations in the world — is not a sign of a broken fund. It is a sign of a market that is pricing fear into everything with credit exposure.

The case for ARDC right now is not momentum. It is mean reversion and income. The 52-week average discount is -4.57%, and the widest it has traded is -11.18%. At current prices, you are buying below the 52-week average and collecting $0.1125 every month while you wait.

ARDC Premium/Discount to NAV 2025-2026 | Source: CEFConnect

Portfolio Composition

The portfolio is built around diversification across credit instruments and issuers, with an average position size of just 0.31%. The top holdings as of January 2026 include Freeport LNG Investments (1.87%), Ensemble Health (1.77%), Charter Communications (1.04%), Ford Motor Credit (0.94%), and Sunoco LP (0.98%) — a mix of energy infrastructure, healthcare, telecom, and financial issuers.