The Fear Gauge Reset — But the Composition Did Not (ATACX)

The headline says calm. The composition says otherwise.

KEY HIGHLIGHTS

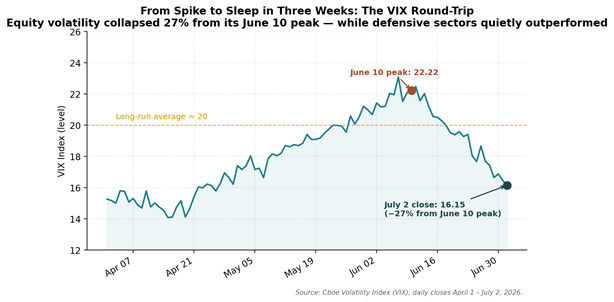

· The Cboe Volatility Index closed at 16.15 on July 2, 2026 — a collapse of roughly 27% from its June 10 peak of 22.22, and now well below its long-run average near 20.[1]

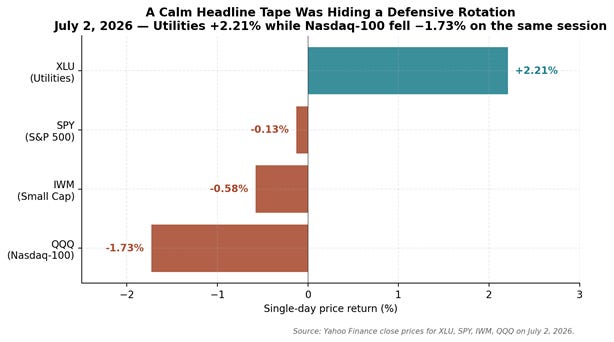

· On the same July 2 session, the Utilities Select Sector SPDR (XLU) rose 2.21% while the Nasdaq-100 (QQQ) fell 1.73% — a nearly 400 basis point single-day defensive rotation under a headline tape that closed near flat (SPY −0.13%).[2]

· Long-term inflation expectations (University of Michigan 5-year) fell from 3.9% to 3.3% in the most recent print — a meaningful decline that has arguably given the equity market permission to reprice volatility lower while core inflation held at 2.9%.[3]

· This is precisely the regime the ATAC Rotation Fund (Ticker: ATACX) was built for — a rules-based credit rotation vehicle designed to respect the shift when the equity market’s defensive composition begins to diverge from the headline vol number, rather than after credit spreads have already blown out.[4]

· In my view the more honest read is that equity volatility has reset at the index level, but the composition underneath — defensive sector outperformance under a calm tape — is not the composition of a market that has fully digested risk. It is the composition of a market that has agreed to ignore it at the headline while quietly rotating underneath.

I’ve found that the most instructive moments in the vol cycle are not the spikes — those are easy to read. The instructive moments are the collapses that come with an asterisk. The VIX round-trip from 22.22 on June 10 to 16.15 on July 2 is one of those. The fear gauge has reset. What sits underneath the reset is a different question, and in my view a more important one for anyone thinking about how to be positioned into the second half of 2026 — and it is exactly the question the ATAC Rotation Fund (ATACX) was built to answer.

THE MACRO BACKDROP: A VOLATILITY RESET UNDER A CALM HEADLINE

In the space of three weeks, the equity vol surface has undergone a complete reset. The Cboe Volatility Index touched 22.22 on June 10, 2026 — the highest reading of the quarter — and closed at 16.15 on July 2, a collapse of roughly 27%.[1] By the standard read of the fear gauge, the market has decided the June risk-off episode is behind it.

That read is not unreasonable on its own terms. Long-term inflation expectations, as measured by the University of Michigan 5-year survey, fell from 3.9% to 3.3% in the most recent print — a substantial decline in a series that tends to be sticky.[3] Core inflation is running at 2.9%, month-over-month CPI at 0.5%, and the unemployment rate came in at 4.2%.[3] The macro backdrop, taken at face value, has given the equity market a genuine reason to reprice the near-term probability of a recession or a policy-shock scenario lower.

Source: Cboe VIX daily closes, April 1 – July 2, 2026. From 22.22 on June 10 to 16.15 on July 2, the fear gauge round-trip is complete.

On the surface, that is a benign configuration. The problem, in my view, is that a vol reset that shows up in the headline number is only one dimension of what a market is doing. The other dimension — the composition dimension — has been quietly moving in the opposite direction. That divergence between the headline number and the composition beneath it is the exact signal that ATACX is designed to weigh.

THE COMPOSITION: UNDER THE CALM HEADLINE, A DEFENSIVE ROTATION

The single most instructive session of the past week was July 2, 2026. On a day when SPY closed −0.13% and IWM −0.58% — an almost featureless tape at the headline level — the internals told a very different story.

The Utilities Select Sector SPDR (XLU) rose 2.21% on the same session, while the Nasdaq-100 (QQQ) fell 1.73%.[2] That is a nearly 400 basis-point single-day spread between the most defensive sector of the equity market and the most growth-oriented one — on a day the headline said nothing was happening.

Source: Yahoo Finance close prices for XLU, SPY, IWM, QQQ on July 2, 2026. The headline was flat; the composition was not.

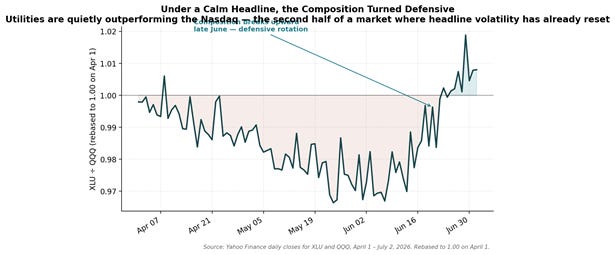

One session is one session. But this is not one session. Over the past several weeks, the XLU/QQQ ratio has broken upward from its post-April drift, and the pattern of Utilities outperforming Nasdaq into a calm tape has become a repeated feature — not a single-day event.

Source: Yahoo Finance daily closes for XLU and QQQ, April 1 – July 2, 2026, rebased to 1.00. The composition has broken defensive even as the headline has reset calm.

WHY THE COMPOSITION MATTERS MORE THAN THE HEADLINE

There is a durable pattern in equity markets that I have spent a long time studying: when defensive sectors — Utilities in particular — begin to outperform the broader market under a calm headline, that outperformance has historically preceded, not followed, a re-emergence of headline volatility. Equity rotation has lower friction than credit rotation, and defensive sector rotation has lower friction than either. When investors are getting cautious in a hurry, they show it in the sector composition first and the headline vol number second.

What makes the current setup worth paying attention to right now — rather than as an abstract observation — is that we are looking at a VIX that has already reset lower and a defensive-sector composition that is trending in the opposite direction. That is a divergence, and divergences of this kind, when they persist, historically resolve in the direction of the composition, not the headline.

From a portfolio management perspective, the more subtle — and in my view more important — implication is this: when the vol surface prices tranquility and the sector composition prices defense, the asset most exposed to a resolution of that divergence is the one most tightly correlated with the vol surface. That is high-yield credit. And it is precisely the environment in which a rules-based approach to credit exposure — the approach that sits inside ATACX — has, in my view, its clearest advantage over a static allocation.

WHAT THIS MEANS FOR A RULES-BASED CREDIT ROTATION APPROACH (ATACX)

This is the kind of regime that is precisely what the ATAC Rotation Fund (Ticker: ATACX), which I brought to market and manage as portfolio manager, was designed for.

ATACX is built around a single idea: credit regimes shift, and the best time to respect that shift is not after spreads blow out, but when the composition of the equity market begins to signal a change beneath a calm headline. The fund is designed to move between credit exposure and a more defensive posture based on rules-based intermarket signals — signals that have historically led credit volatility rather than coincided with it. The intuition is straightforward: equity investors reallocate faster than credit investors, defensive sectors reallocate faster than the overall equity market, and Utilities reallocate faster than most.

I want to be honest about the trade-off. Rules-based credit rotation is not a tool for avoiding short-term noise. There are periods when the signal whipsaws. ATACX has had years of negative returns as well as strong years — the fund’s worst calendar year since inception was −25.80% in 2022, and its best was +72.51% in 2020.[4] Rules-based rotation is not designed to be smooth. It is designed to not be structurally committed to credit risk through a regime change.

The current setup — a VIX that has reset from 22.22 to 16.15, a defensive-sector composition that has broken upward under that calm headline, and macro conditions that give the market permission to price tranquility — is the kind of configuration where the cost of staying static in credit can compound quickly if the composition is correct and the headline is not.

THE BOTTOM LINE

Right now we have:

— a VIX that has reset from 22.22 (June 10) to 16.15 (July 2), a −27% round-trip,[1]

— XLU +2.21% on July 2 while QQQ fell 1.73% on the same session,[2]

— long-term inflation expectations declining from 3.9% to 3.3%,[3] and

— core inflation at 2.9% and unemployment at 4.2%.[3]

That combination does not guarantee that the composition is right and the headline is wrong. But it does suggest the asymmetry has changed. When the fear gauge has reset and the sector composition has quietly rotated defensive, I think the more honest read is not that risk has been resolved — it is that the market has chosen where to express its caution, and that is not, right now, in the headline vol number. That is the environment ATACX was built to navigate — not to predict, but to respect.

ENDNOTES

[1] Cboe Global Markets, “VIX Index Historical Data,” accessed July 5, 2026, https://www.cboe.com/tradable_products/vix/vix_historical_data/

[2] Yahoo Finance close prices for XLU (Utilities Select Sector SPDR), SPY (SPDR S&P 500 ETF), IWM (iShares Russell 2000 ETF), and QQQ (Invesco QQQ Trust) on July 2, 2026.

[3] University of Michigan Surveys of Consumers (5-year inflation expectations) and U.S. Bureau of Labor Statistics (CPI, unemployment rate), accessed via FRED, July 5, 2026, https://fred.stlouisfed.org/

[4] ATAC Rotation Fund (ATACX) calendar-year performance data, ATAC Funds, https://atacfunds.com/atacx/. Past performance is not indicative of future results.

Michael A. Gayed, CFA

DISCLOSURES (ATACX)

References to other securities is not an offer to buy or sell.

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the “fear gauge” of Wall Street, is a real-time market index that measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

ATACX is distributed by Foreside Fund Services, LLC.

Learn more about $ATACX at https://atacfunds.com/atacx/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.