The Great Rotation Meets $100 Oil

Small Caps Surge, Hormuz Stays Shut, and Seven Central Banks Walk Into a Bar

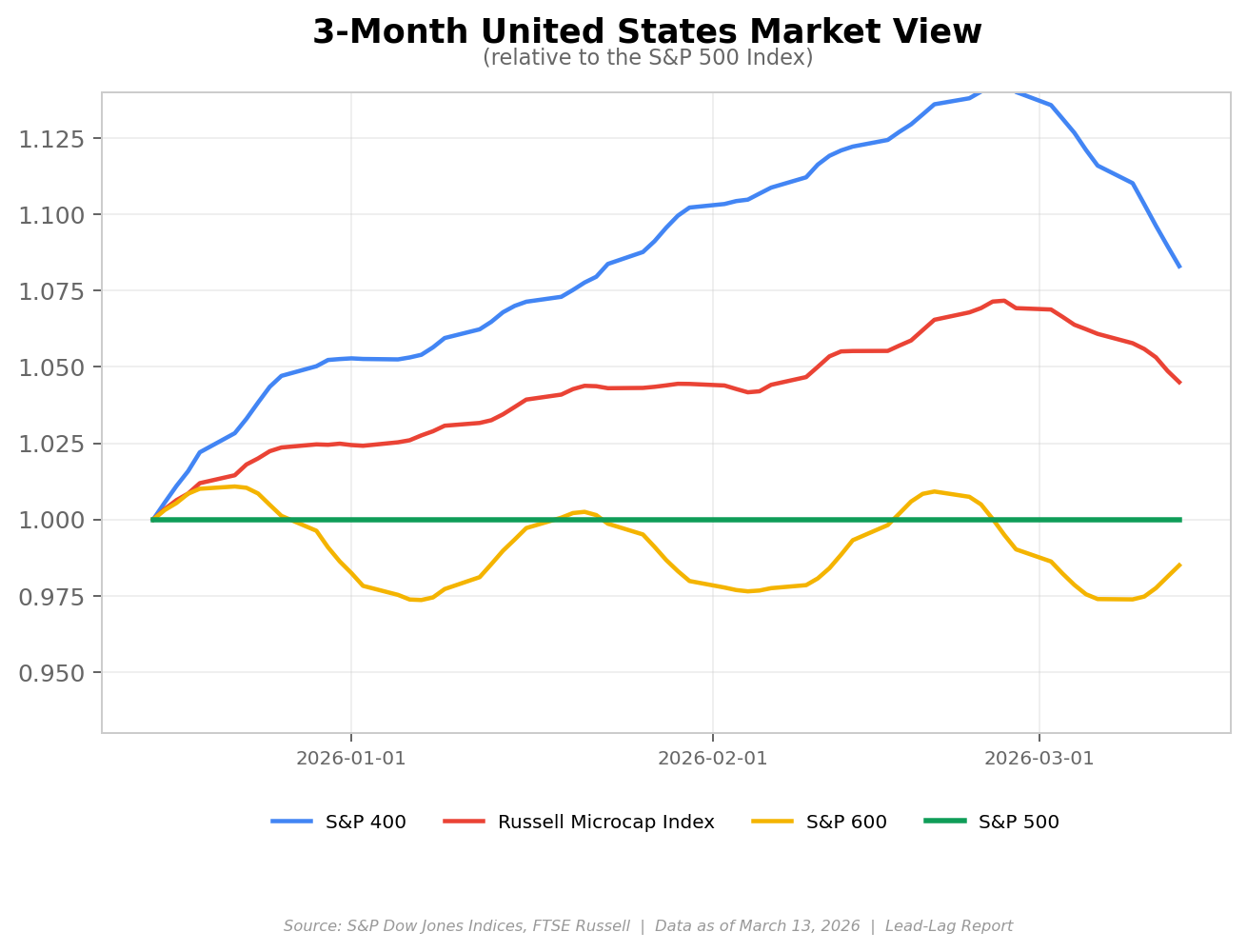

A week ago I said the rotation was real. It’s more than real now—it’s accelerating in a way that’s forcing even the most stubborn large-cap bulls to pay attention. The Russell 2000 is up 8.9% year-to-date through March 11. The equal-weight S&P 500 is positive on the year by several percentage points. Meanwhile, the cap-weighted S&P 500 sits at 6,672.62 as of Wednesday’s close, down 2.53% on the year. That’s a spread of more than 11 percentage points between the Russell 2000 and the S&P 500, and it’s happening while the VIX is at 27.85 after spiking to 35.3 intraday on Monday. This is not a calm, orderly rotation. This is a market that’s simultaneously pricing in a regime change in equity leadership and a geopolitical crisis that has no clear resolution.

The sector story is equally dramatic. The Energy Select Sector SPDR is up roughly 27% year-to-date, hitting fresh 52-week highs almost daily as Brent crude trades above $100 a barrel for the first time since 2022. WTI is at roughly $96. The software sub-sector of the S&P 500, measured by the IGV ETF, is down 19.5% year-to-date. That’s a nearly 47-percentage-point divergence between the best and worst-performing sectors. I’ve been in this business a long time, and I cannot recall a YTD sector spread this extreme by mid-March. February CPI came in at 2.4% year-over-year on March 11, largely in line with expectations. But the real inflation story is in the ISM Manufacturing Prices Paid index at 70.5%, the highest since June 2022, and that reading was taken before Brent broke through $100. The February PPI release has been delayed to March 18 due to the government shutdown—the same day as the FOMC decision. The Fed is boxed in. CME FedWatch shows an overwhelming probability of a hold at the March 18 meeting. The dot plot update will be the real event. If the median dot shifts higher, that’s the Fed admitting the stagflation scenario is becoming baseline.