The Grid Is the New Gold: Inside UTG, the Utility CEF Built for the AI Power Era

Reaves Utility Income Fund is paying you $0.20/month to own the AI power trade.

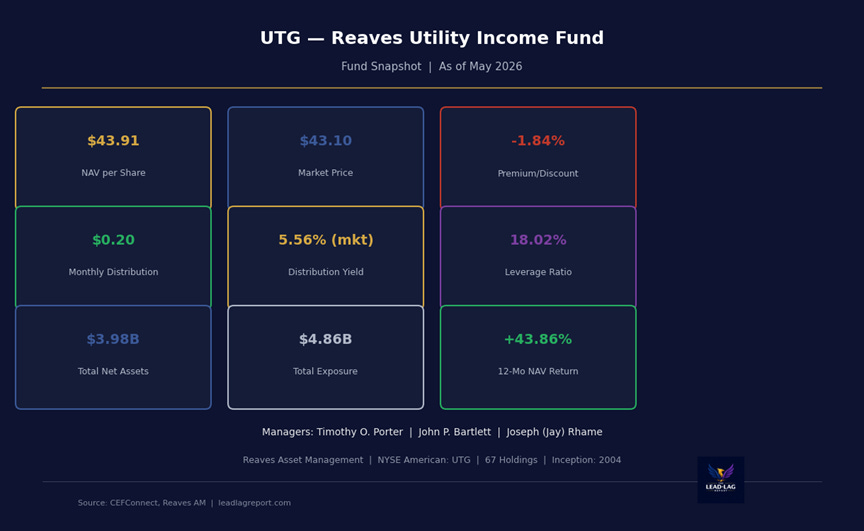

UTG — Reaves Utility Income Fund | Fund Snapshot as of May 2026

There is a phrase I keep coming back to lately: the grid is the new gold. Every AI model that gets trained, every data center that hums through the night, every electric vehicle charging up at midnight — all of it runs on electrons. And someone has to build, own, and operate the infrastructure that delivers those electrons. That someone is the utility sector. And one of the most compelling ways to own that story — while getting paid $0.20 every single month — is the Reaves Utility Income Fund (NYSE American: UTG).

I want to walk through why UTG has become one of my favorite ways to think about the intersection of income and infrastructure, and why the current setup — a mild discount, a recent distribution raise, and a portfolio aligned to the biggest secular theme of our time — is worth your attention.

Fund Background

UTG is a closed-end fund managed by Reaves Asset Management (W.H. Reaves & Co.), a firm that has focused almost exclusively on utilities and essential infrastructure since the 1960s. That specialization matters. Reaves isn’t a generalist manager dabbling in utilities when the trade looks interesting — they are utilities, full stop.

The fund launched in 2004 and trades on the NYSE American exchange. As of early May 2026, total common assets stand at approximately $3.98 billion, with total investment exposure (including leverage) reaching $4.86 billion. The fund holds 67 positions and turns over roughly 37% of the portfolio annually — an active but not frenetic approach.

The portfolio managers are Timothy O. Porter, John P. Bartlett, and Joseph (Jay) Rhame. The mandate is to generate “a high level of after-tax income and total return” by investing at least 80% of total assets in dividend-paying stocks and debt instruments of utility-industry companies.

The NAV per share currently sits at $43.91, while the market price is $43.10, reflecting a -1.84% discount to NAV. The 52-week average was essentially flat to NAV at -0.22%, so today’s mild discount is slightly below the norm — and if you believe the utility cycle is still early-innings, that’s a reasonable entry point.