The Nasdaq Is Falling. Your Income Doesn't Have To.

How a Daily 0DTE Covered Call Strategy on QQQ Turns Tech Volatility Into a Paycheck

Key Highlights

• The Nasdaq 100 fell 2.3% in February—its steepest monthly decline since March 2025—while the Magnificent Seven Index dropped 7.3%.

• Approximately $270 billion has flowed into options-based ETFs as investors seek income beyond traditional dividends and bonds.

• 0DTE (zero-day-to-expiration) options now represent nearly 60% of all S&P 500 options volume, up from 5% in 2016.

• The TappAlpha Innovation 100 Growth & Daily Income ETF (TDAQ) uses a daily 0DTE covered call strategy on QQQ, designed to harvest elevated premiums in volatile markets while maintaining Nasdaq-100 growth participation.

• In a sideways-to-corrective market, the income layer of a daily covered call strategy becomes the primary driver of total return.

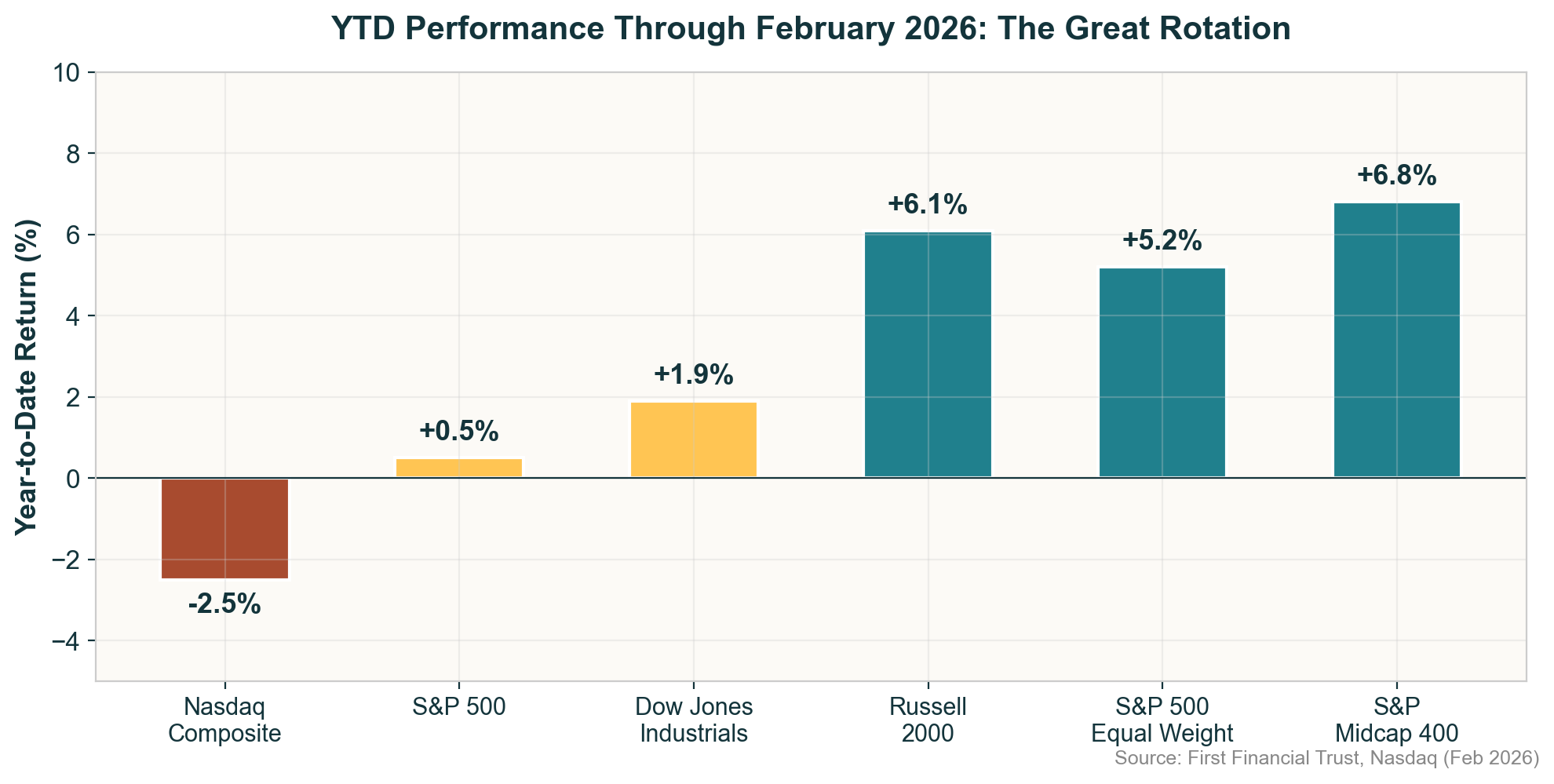

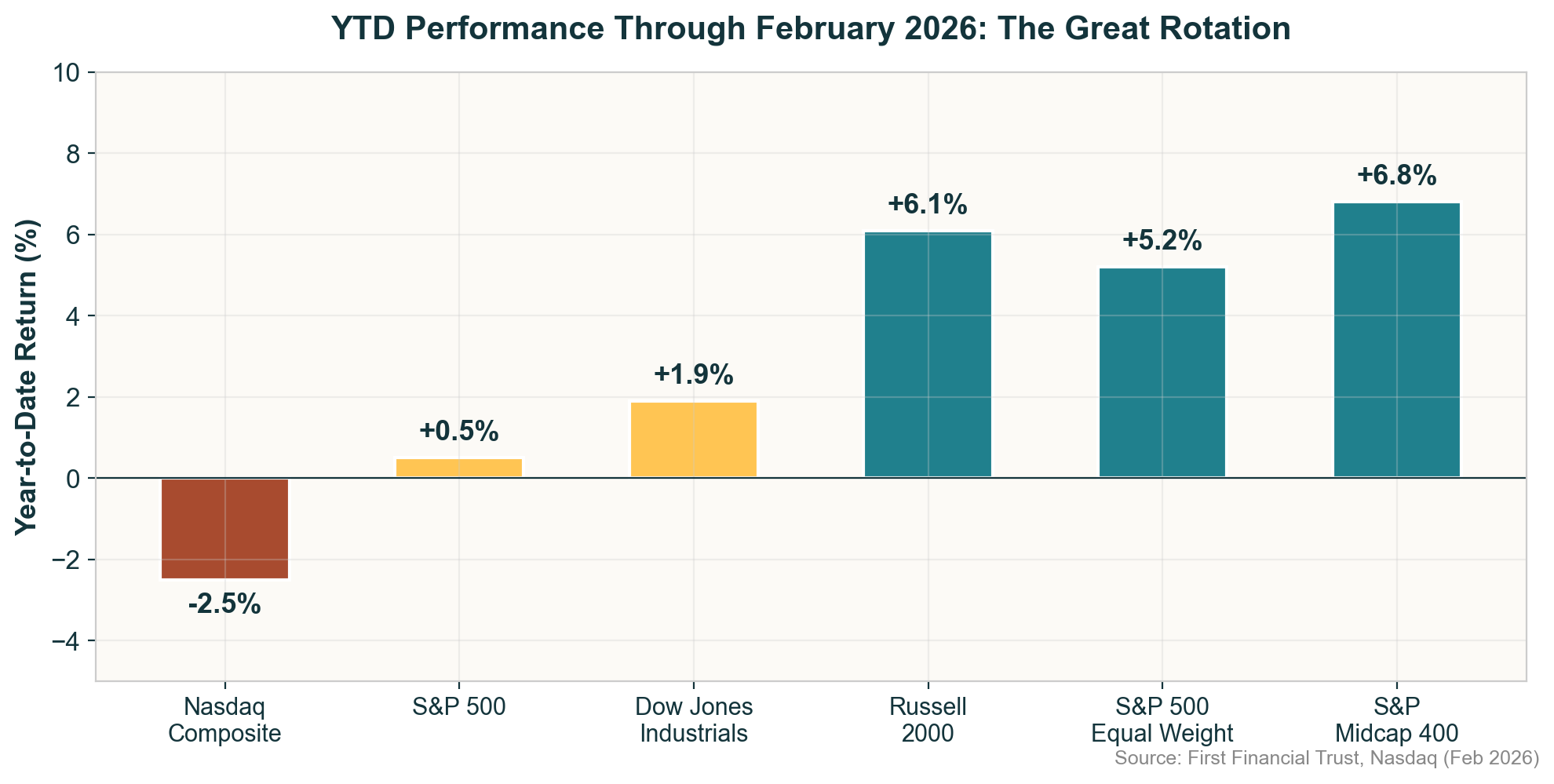

February was a rough month for tech investors. The Nasdaq 100 fell 2.3%, its steepest monthly decline since March 2025, while the Magnificent Seven Index dropped 7.3%.1 The S&P 500 Equal Weight Index, meanwhile, surged 3.5%—its best month since May 2025. The message from the market was clear: the era of being rewarded simply for owning the biggest names in tech is being challenged.

Yet here’s what makes this moment interesting from an intermarket perspective: the same volatility that’s punishing buy-and-hold tech investors is simultaneously creating a potentially richer income opportunity for those who know how to harvest it. Options premiums—the price the market charges for uncertainty—historically have been elevated precisely when fear is highest. And a category of ETF is designed to systematically convert that fear into cash flow, every single trading day.

Figure 1: Broad indices mask a dramatic rotation away from tech and toward small/mid-caps and equal-weight strategies.

The Tech Correction Everyone Saw Coming

The warning signs had been accumulating. AI capex projections from the hyperscalers—Meta, Microsoft, Alphabet, and Amazon—are now expected to exceed $500 billion in 2026.2 Investors initially cheered the spending as a signal of confidence, but a different question started to dominate: when will this spending translate into profits?

Microsoft’s stock has shed roughly $1 trillion in market value since October 2025, driven by slowing Azure growth and concerns that 45% of its future revenue is tied to OpenAI.3 The iShares Expanded Tech-Software Sector ETF (IGV) fell over 35% from its October high to its late-February low.1

Then there’s geopolitics. The U.S.-Israeli military strikes on Iran sent Brent crude surging past $80, with Iran’s threats to close the Strait of Hormuz—a chokepoint for roughly 20% of global oil supply—rattling energy markets and reigniting inflation fears.4 Sticky CPI readings have left the Fed in a holding pattern at 3.50–3.75%, with rate cuts potentially delayed until mid-year.5

Figure 2: February’s sector performance reveals the sharpest growth-to-value rotation in years. Tech, communications, and consumer discretionary led losses while energy, utilities, and materials surged.

For tech investors, this is a triple threat: AI spending uncertainty, geopolitical risk, and a Fed that can’t ride to the rescue. The Nasdaq-100 was rejected at its 100-day moving average in early March and breached the psychologically significant 25,000 level.6 What many analysts are calling “AI fatigue” has set in—the market is no longer willing to pay for potential without proof.

The Income Imperative: Why Volatility Is an Asset

In traditional investing, volatility is something to endure. In the options world, it’s something to monetize. This distinction has never been more relevant than in 2026.

The S&P 500’s dividend yield sits below 2%.7 Ten-year Treasury yields have fallen to near 4%.8 For investors who need income—retirees, endowments, anyone drawing down a portfolio—there’s a growing gap between what traditional sources offer and what they require.

Capital has been flooding into options-based ETFs as a result. According to CNBC, approximately $170 billion has been allocated to “synthetic income” ETFs that use options for income generation, alongside $100 billion in “buffer” ETFs for downside protection.9

Figure 3: The options-based ETF market has grown to $270 billion, reflecting a structural shift from traditional dividends and bonds toward premium-based income strategies.

0DTE: The Mechanic Behind the Strategy

Zero-days-to-expiration options—known as 0DTE—have become one of the most important structural developments in modern markets. In 2025, SPX 0DTE contracts averaged 2.3 million per day and represented 59% of total S&P 500 options volume.10 These are not fringe instruments. They are the new baseline.

Figure 4: 0DTE options have surged from 5% of S&P 500 volume in 2016 to nearly 60% by 2025, fundamentally reshaping how institutions and retail investors manage short-term risk.

The appeal of 0DTE for income generation is rooted in theta decay—an option’s accelerating loss of value as expiration approaches. A call option that expires at the close of the same day it’s written delivers the maximum possible rate of time decay to the seller. This is the core mechanism behind the TappAlpha Innovation 100 Growth & Daily Income ETF (TDAQ).11

TDAQ holds QQQ—the Invesco QQQ Trust, which tracks the Nasdaq-100—and writes out-of-the-money call options against it every single trading day that expire the same day. Each morning, the strategy resets. Each evening, those options expire. The premium collected becomes income. The next day, it starts again.

The daily cadence matters. First, it helps to limit the fund’s risk of being caught on the wrong side of a sudden move—if markets gap overnight, the previous day’s options have already expired. Second, it allows constant recalibration. In a week when the Nasdaq drops 3%, the fund isn’t locked into a call it wrote at higher prices. Third, and most importantly for income investors, the daily premium collection compounds into a continuous stream rather than a single monthly check.

Why This Market Makes the Case

When the VIX is elevated, options premiums are richer. When the Nasdaq-100 is trading sideways or correcting, the probability that daily calls expire worthless—allowing the fund to keep the full premium—increases. The S&P 500 has returned less than 0.5% year-to-date.9 The Nasdaq is down 2.5%.8 In this stagnant environment, option premiums become the primary source of return.

BlackRock’s 2026 Investment Directions outlook noted that “options income strategies can help investors with a differentiated source of return by seeking to capture volatility risk premium through covered call writing.”12 The combination of AI-driven dispersion, midterm election year volatility, and a shifting rate environment makes covered call strategies particularly well-positioned this year.

The Trade-Off You Need to Understand

No strategy is a free lunch. A covered call strategy caps upside participation. If the Nasdaq-100 surges 5% in a single day, TDAQ’s calls will limit the fund’s ability to capture all of that gain. In a relentless bull market, a pure QQQ position will outperform over time.

But “relentless bull market” does not describe what investors are currently experiencing. The market is in what analysts have termed a “show me” phase.6 Good earnings are no longer sufficient to drive price appreciation without proof that AI spending will translate to bottom-line growth. In this environment, the upside cap of a covered call strategy is less costly than it would be during a momentum-driven rally.

Because TDAQ’s underlying holding is QQQ, the fund inherits the Nasdaq-100’s heavy weighting toward technology (~50%), communications services (~17%), and consumer discretionary (~12%). A daily 0DTE covered call strategy is not a replacement for diversification—it’s a complement that maintains tech growth participation while generating a cash flow stream difficult to replicate through dividends alone.

Where TDAQ Fits in a Portfolio

TDAQ is best understood as an allocation decision rather than a trade. For income-oriented investors—retirees, those in the distribution phase—it offers a structural source of cash flow tied to the Nasdaq-100 without requiring the index to rise. For growth-oriented investors, it can serve as a volatility dampener within a broader tech allocation, generating yield that partially offsets drawdowns during corrective periods like the one underway.

With an AUM of approximately $121 million and listing on the Cboe since its September 2025 inception, TDAQ’s three-holding structure—overwhelmingly QQQ with a small cash position—keeps the strategy transparent.11 The daily 0DTE approach means the fund doesn’t take multi-week directional bets through its options book. Each day is a clean slate.

The Bigger Picture

We are in a market repricing risk in real time. The growth-to-value rotation is the broadest in years.1 Geopolitical shocks are injecting energy-driven inflation risk that the Fed has limited tools to combat.13 And yet—fourth-quarter earnings growth came in at 13.2%, the fifth consecutive quarter of double-digit growth.8 AI spending may be excessive, but it is building real infrastructure.

The investors who navigate this environment most effectively are those who recognize that volatility is not the absence of opportunity but the presence of it. A daily 0DTE covered call strategy on the Nasdaq-100 is one answer. It doesn’t require you to be right about the direction of AI spending, the outcome of the Iran conflict, or the Fed’s next move. It requires only that you’re willing to trade some upside for a consistent income stream—and that volatility, the very thing making headlines, keeps doing its job.

The Nasdaq is falling. Your income doesn’t have to.

Disclosure:

This content is sponsored by TappAlpha. The Lead-Lag Report has been compensated for the publication of this material. The views and opinions expressed herein are those of the author and do not necessarily reflect the views of TappAlpha or its affiliates.

This material is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy, sell, or hold any securities, including TDAQ.

The fund currently expects, but does not guarantee, to make distributions on a monthly basis. Distributions may exceed the fund’s income and gains for the taxable year. Distributions in excess of the fund’s current and accumulated earnings and profits will be treated as a return of capital.

For Institutional Use Only

Investors should carefully consider the investment objectives, risks, charges and expenses of the ETFs identified on this site. This and other important information about the Fund are contained in the prospectus, which can be obtained on this site or by calling (844) 403-2888. The prospectus should be read carefully before investing. Please click here for the prospectus: https://cdn.prod.website-files.com/659c04f60051914529d01524/69a72d03b40134867ab95421_TappAlpha%20Prospectus%204.30.2025%2C%20%20sticker%202026.03.02.pdf

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. Performance current to the most recent month-end can be obtained above. Returns less than one year are not annualized.

Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. The Fund does not have a track record of reporting to investors or widely available research coverage which may result in price volatility.

Market performance is the price at which shares in the ETF can be bought or sold on the exchanges during trading hours, while the net asset value (NAV) represents the value of each share’s portion of the fund’s underlying assets and cash at the end of the trading day.

Click here for standardized performance: https://www.tappalphafunds.com/etfs/tdaq

Investing involves risk. Principal loss is possible. The Fund’s shares will change in value, and you could lose money by investing in the Fund. The Fund may not achieve its investment objectives. The Fund invests in options contracts that are based on the value of the Index. This subjects the Fund to certain of the same risks as if it owned shares of companies that comprised the Index, even though it does not own shares of companies in the Index. The Fund will have exposure to declines in the Index. The Fund is subject to potential losses if the Index loses value, which may not be offset by income received by the Fund. By virtue of the Fund’s investments in options contracts that are based on the value of the Index, the Fund may also be subject to an indirect investment risk, an index trading risk & a Nasdaq 100 Index Risk.The Nasdaq-100® Index is a widely recognized benchmark index that tracks the performance of 100 of the largest non-financial companies listed on the Nasdaq Stock Market, including NDX and XND options. These companies represent a broad range of industries, with a notable concentration in technology-related sectors. The Index is market-capitalization weighted and includes companies across sectors such as information technology, consumer discretionary, communication services, healthcare, and industrials. As of December 31, 2023, the five largest sectors in the Index were information technology, consumer discretionary, communication services, healthcare, and industrials. The composition of the Index can change over time due to market capitalization shifts, periodic rebalancing, and company eligibility changes.

Regarding volatility, the Nasdaq-100® Index, like all market indices, has experienced periods of significant daily price movements. Its higher concentration in growth-oriented and technology-related companies can contribute to greater short-term volatility compared to more diversified indices. Despite these fluctuations, the Index has demonstrated strong long-term performance over its history.

Due to the short time until their expiration, 0DTE options are more sensitive to sudden price movements and market volatility than options with more time until expiration. Because of this, the timing of trades utilizing 0DTE options becomes more critical. Even a slight delay in the execution of 0DTE trades can significantly impact the outcome of the trade. 0DTE options may also suffer from low liquidity, making it more difficult for the Fund to enter into its positions each morning at desired prices. The bid-ask spreads on 0DTE options can be wider than with traditional options, increasing the Fund’s transaction costs and negatively affecting its returns. These risks may negatively impact the performance of the fund.

As of the date of this prospectus, the Fund has no operating history and currently has fewer assets than larger funds. Like other new funds, large inflows and outflows may impact the Fund’s market exposure for limited periods of time. This impact may be positive or negative, depending on the direction of market movement during the period affected.

Distributor: Foreside Fund Services, LLC, Member FINRA.

DISCLAIMER – PLEASE READ: This is a sponsored article for which Lead-Lag Publishing, LLC has been paid a fee. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the article or make any representation as to its quality. All statements and expressions provided in this article are the sole opinion of TappAlpha and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the discussion. The content in this writing is for informational purposes only. You should not construe any information or other material as investment, financial, tax, or other advice. A participant may have taken or recommended any investment position discussed, but may close such position or alter its recommendation at any time without notice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in any jurisdiction. Please consult your own investment or financial advisor for advice related to all investment decisions.