The Pipes That Power AI, Repriced: A Renamed, Restructured Bet on Energy Infrastructure

Kayne Anderson's flagship midstream fund has been rebranded, switched to a monthly and 20% higher distribution, and rallied 39% this year, yet the discount to NAV has widened rather than closed.

Today’s Lead-Lag Report post is sponsored by workzone

Kill The Busywork. Get Your Week Back.

It's called vibe coding: you describe what you want in plain English, and AI builds it. Landing pages and campaigns. Dashboards and reports for leadership. Automations that kill the busywork. No code, no waiting on anyone else. On July 30th, we'll show you how, starting from the beginning.

DISCLAIMER — PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC is being paid a fee. The information provided is solely the creation of workzone. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided or make any representation as to its quality. All statements and expressions provided are the sole opinion of workzone and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided.

The Pipes That Power AI, Repriced: A Renamed, Restructured Bet on Energy Infrastructure

KEY HIGHLIGHTS

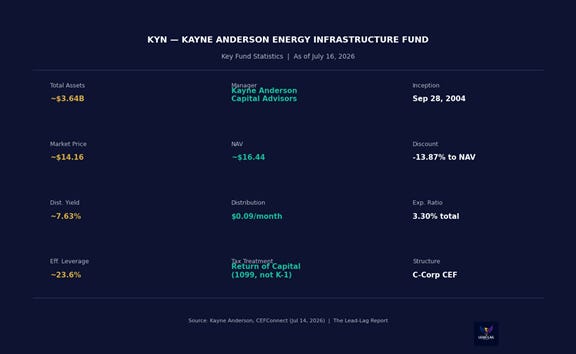

· Yield: 7.63% distribution yield | $0.09/month (switched from quarterly, raised 20%)

· Tax: Return of capital distributions — 1099 (not K-1)

· Valuation: -13.87% discount to NAV — wider than 52-week avg (-11.89%); mean-reversion potential

· 2026 YTD: +25.7% price return as AI energy demand lifts midstream; NAV rose faster

· AUM / Cost: ~$3.64B total assets | 3.30% expense ratio (C-Corp tax drag included)

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Macro/Market Context

The single most important energy story of this decade is not the price of oil. It is electricity, and more specifically the electricity required to power artificial intelligence. Every major hyperscaler, from Microsoft and Google to Amazon and Meta, is racing to build and expand data centers that consume power on a scale the grid has never had to accommodate. The fastest-deployable source of baseload power for that buildout is natural gas, and natural gas moves through pipelines. RBC Capital Markets estimated in May 2026 that natural gas consumption from data centers could reach roughly 6.1 billion cubic feet per day by 2030, a demand driver that simply did not exist when most pipeline investors first built their thesis.

The reframing has been swift enough to reach the mainstream financial press. Fortune ran the headline “Data centers and gas demand make boring pipelines great again” in April 2026, and that same month ADI Analytics described “midstream’s shift from pipes to power platforms.” The companies that own and operate these systems are the toll collectors of the energy economy. They do not need oil at a hundred dollars a barrel to profit. They collect fees on volume, and volume is rising because the AI campuses being built across the country have to be fed.

One vehicle that packages this exposure into a single listed security is the Kayne Anderson Energy Infrastructure Fund (KYN), a closed-end fund managed by Kayne Anderson Capital Advisors, L.P. The fund was officially renamed from the Kayne Anderson MLP/Midstream Investment Company in June 2026, a change that captures how the underlying business has broadened from pure MLPs toward the wider energy infrastructure that now includes the power backbone of the data center era. KYN owns a concentrated portfolio of the largest midstream operators in North America and pays a distribution that yields roughly 7.63% at the current price. It is not a quiet income vehicle. It is a leveraged, high-conviction wager on the arteries of the continent’s energy system, and it has just gone through a transformation that changes how the fund should be read.

Fund Background

Structure. KYN is a non-diversified closed-end fund that trades on the NYSE. It launched on September 28, 2004, and operates on a fiscal year ending November 30. Unlike most closed-end funds, which are organized as regulated investment companies, KYN is structured as a C-corporation, a detail that carries meaningful tax consequences discussed later.

Manager. The fund is managed by Kayne Anderson Capital Advisors, L.P., a firm with deep specialization in energy and midstream infrastructure investing. That focus matters in a sector where portfolio construction, leverage management, and tax handling require dedicated expertise.

Scale and leverage. KYN now manages roughly 3.64 billion dollars in total assets, with net assets attributable to common shareholders of about 2.78 billion dollars. That is a dramatic increase from the fund’s footprint a year or two ago, driven by both asset appreciation and the sector’s expansion. Effective leverage sits near 23.6% of assets, notably lower than the 30 to 33 percent range the fund carried in prior cycles. The deleveraging is a meaningful risk reduction, though leverage still amplifies both gains and drawdowns.

Pricing. As of July 16, 2026, KYN trades near 14.16 dollars per share against a net asset value of roughly 16.44 dollars, a discount to NAV of about negative 13.87 percent. Over the trailing 52 weeks the shares have ranged from 11.31 to 14.70 dollars, and the average discount over that period has been negative 11.89 percent. The price is up roughly 39% so far this year.