The Private Credit Machine Is Cracking Where No One Is Looking

Apollo's Q2 Redemption Requests Nearly Doubled Q1's. The KBRA Default Index Just Matched Its All-Time High. The Reckoning Everyone Called Six Months Ago Is Now Compounding.

Today’s Lead-Lag Report post is sponsored by Tuttle Capital

If you have not registered yet, the link is below.

The recording goes to registered attendees only.

What you will get on the call:

● The permanent portfolio framework walked through end to end, conceptually

● Where Browne’s original assumptions hold up and where they break

● How to think about forecast-independent allocation in the current regime

● Live Q and A with Matt, Porter and Frances

● CE credit submission for anyone holding the CFP, CIMA, or equivalent designation

DISCLAIMER — PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC is being paid a fee. The information provided is solely the creation of Tuttle Capital. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided or make any representation as to its quality. All statements and expressions provided are the sole opinion of Tuttle Capital and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided.

The Private Credit Machine Is Cracking Where No One Is Looking

KEY HIGHLIGHTS

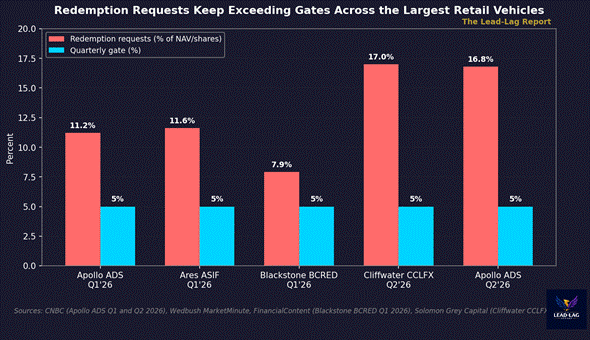

• Apollo’s flagship retail vehicle, Apollo Debt Solutions, took redemption requests equal to 16.8% of the fund in the second quarter of 2026, up from 11.2% in the first quarter, and is again capping withdrawals at 5%.

• The KBRA DLD Direct Lending Index’s trailing twelve-month default rate rose to 2.3% of issuers as of mid-June 2026, matching the highest level since the index launched, with KBRA projecting 3.5% by year-end.

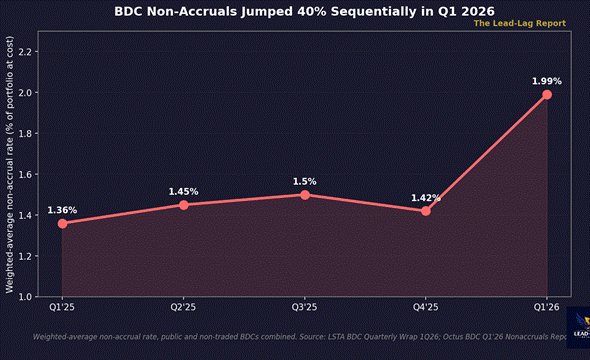

• BDC non-accruals jumped 40% sequentially in Q1 2026 to 2.01% of aggregate reported debt investments at cost, and Octus estimates the adjusted figure, including likely under-reporting, at 3.24%.

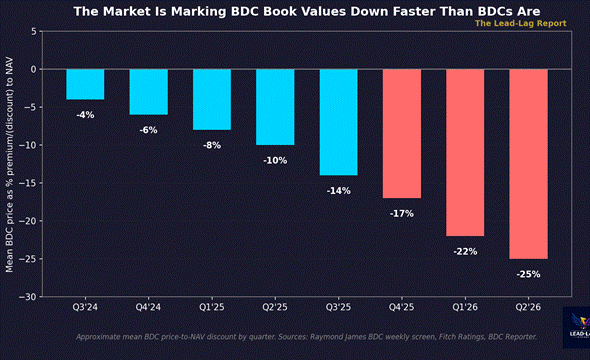

• The mean publicly traded BDC now trades at an estimated 20-25% discount to net asset value, a level not seen since the depths of prior credit cycles, even as reported NAVs have barely moved.

• Ares’ Strategic Income Fund and Blackstone’s BCRED both breached their own redemption gates earlier in 2026. Cliffwater’s Corporate Lending Fund took 17% redemption requests in Q2 against a 5% cap.

Six weeks ago this column argued that private credit’s reckoning had already started and the marks simply had not caught up. The evidence since then has not complicated that thesis. It has accelerated it.

Apollo Global Management disclosed in late June that redemption requests on its flagship retail vehicle, Apollo Debt Solutions, hit approximately $2.4 billion, or 16.8% of the fund, in the second quarter of 2026 — up from 11.2% just one quarter earlier.[1] Apollo is again capping withdrawals at the contractual 5% ceiling. Investors asking for a dollar are getting roughly 30 cents, and the ratio of demand to available liquidity is now worse than it was the last time this column covered it.

The Equity Market’s Verdict Has Not Changed. It Has Hardened.

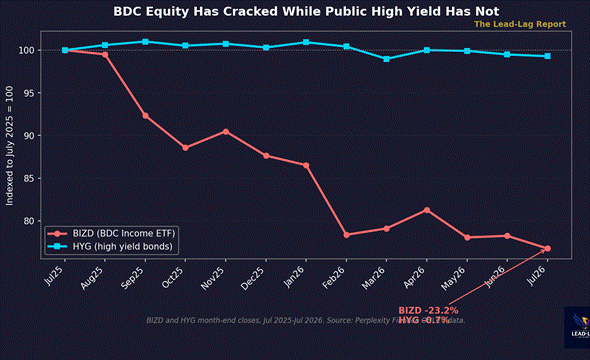

Publicly traded business development companies remain the cleanest real-time proxy for what the market thinks BDC net asset values are actually worth, because their equity trades every day while their underlying loan books are marked quarterly. The VanEck BDC Income ETF, BIZD, has fallen approximately 23% over the trailing twelve months through July 3, 2026, while the iShares iBoxx High Yield Corporate Bond ETF, HYG, is roughly flat over the same period.[2] That is not a broad credit selloff. It is a private-credit-specific repricing, isolated to the vehicles that hold the loans everyone is worried about.

Individual names show the same pattern. Ares Capital, the largest BDC by portfolio size, has fallen from the low $20s a year ago to roughly $18.50 today.[3] Blue Owl Capital Corporation, OBDC, is down to roughly $10.85, having cut its base dividend 16% earlier this year as lower base rates and spread compression pulled adjusted net investment income down to match the reduced payout exactly.[4] Hercules Capital and Blackstone Secured Lending have both round-tripped through sharp February drawdowns and only partially recovered. The mean BDC now trades at an estimated 20-25% discount to stated net asset value — wider than the 22% discount this column flagged in May, not narrower.[5]

The Default Data Just Confirmed the Trend, Not Reversed It

The counting-convention debate from the spring is now resolving in the bears’ direction on every measure that updates in real time. Fitch’s U.S. Private Credit Default Rate, which counts payment-in-kind conversions and maturity extensions alongside bankruptcies, sat at 6.0% on a trailing-twelve-month basis through April, the record this column cited previously.[6] What has changed is the narrower, market-standard measure. Bloomberg reported in mid-June that the KBRA DLD Direct Lending Index’s trailing twelve-month default rate climbed to 2.3% of issuers, matching the highest level since the index’s December 2023 inception, with KBRA projecting a rise to 3.5% — roughly 111 issuers — by the end of 2026.[7] That is the stricter, bankruptcy-and-missed-payment index moving toward the more expansive Fitch measure, not away from it.

Non-accruals tell the same story with a sharper inflection. The LSTA’s BDC Quarterly Wrap found the weighted-average non-accrual rate across public and non-traded BDCs rose to 1.99% in the first quarter of 2026, up from 1.42% in the fourth quarter of 2025 and 1.36% a year earlier.[8] Octus, tracking the dollar figures directly, found $9.98 billion of debt at cost in non-accrual status in Q1 2026, a 40% sequential jump from $7.12 billion in Q4 2025, and estimated that the true, under-reported exposure could be closer to $16.04 billion — a 61% increase over the reported figure.[9] Individual names are the ones carrying the weight: Blue Owl’s OBDC posted a 16% dividend cut, FS KKR’s non-accruals ran as high as 8.1% at cost, and Blackstone Secured Lending’s non-accruals surged to 4.7% of cost with NAV down more than 2% quarter over quarter.[10]

The Structural Backdrop Has Not Moved. That Is the Point.

Private credit assets under management have grown from roughly $500 billion in 2014 to an estimated $2.1 trillion in 2026, a buildout that has outpaced the growth of bank commercial and industrial lending by a wide margin over the same period.[11] Preqin still projects further growth from here. None of the stress data changes that trajectory in the near term — capital keeps flowing in even as redemption requests keep exceeding gates on the way out. That asymmetry, more capital committed to illiquid structures than the structures can return on demand, is the mechanical reason gates keep tripping regardless of how any single quarter’s default number reads.

The Federal Reserve’s May 2026 Financial Stability Report addressed this directly, noting that accepted redemptions from perpetual BDCs exceeded new inflows in the first quarter of 2026 for the first time since these structures were created, while characterizing the redemption activity itself as “limited and manageable.”[12] The Financial Stability Board’s parallel report on private credit vulnerabilities, published the same week, flagged opacity, valuation uncertainty, and interconnection with banks and insurers as the open questions regulators still cannot fully measure.[13]

Redemption Gates Are No Longer an Apollo-Specific Story

What has changed most since this column’s original take is the breadth of the gate-tripping. Ares capped redemptions on its $21.5 billion Strategic Income Fund at 5% in the first quarter after withdrawal requests reached 11.6% of shares — more than double the quarterly limit.[14] Blackstone’s BCRED took $3.7 billion in redemption requests in the first quarter, roughly 7.9% of net asset value, and the board opted to upsize its repurchase limit to 7% rather than hold the standard 5% cap.[15] Cliffwater’s Corporate Lending Fund, one of the largest retail-facing interval funds at roughly $31 billion, took redemption requests of 17% against its 5% cap in the second quarter.[16] Four large, differently structured vehicles, run by four different managers, hit the same wall in the same two quarters. That is not idiosyncratic manager risk. That is a structural feature of how these funds were designed.

Washington Noticed Too

Senator Elizabeth Warren used a June 11 Senate Banking Committee hearing to connect private credit directly to systemic risk, warning that AI companies are “buying borrowing upwards of a trillion dollars” through private credit funds that themselves borrow from banks, and that a downturn in AI-linked revenue could “risk bringing down giant banks” in a scenario she compared explicitly to 2008.[17] Whether or not that specific chain of contagion plays out, the framing matters: a sitting member of the Senate Banking Committee is now treating private credit and AI financing as the same conversation, not two separate ones.

The Other Side, Taken Seriously

The bull case has real substance and deserves a fair hearing. Non-accrual rates at the largest, most conservatively underwritten BDCs remain well below the levels seen in 2020, and several managers — Barings among them — report non-accruals near the low end of the industry even as sector averages rise.[18] Cliffwater’s realized loss data for 2025 came in at 0.70%, below the 1.01% long-run average, and some analysts characterize the current move as normalization back toward historical norms rather than a genuine deterioration.[19] Senior secured unitranche yields remain attractive on an absolute basis, and the asset class is not going away regardless of how this specific cycle resolves.

The problem with the normalization argument is timing, not direction. Normalization from artificially suppressed post-2021 non-accrual levels back to a 2.5% historical average is exactly what a credit cycle turning looks like in its early stages. The KBRA index moving from 1.4% to a projected 3.5% inside twelve months, Octus’s non-accrual dollar figure rising 40% in a single quarter, and four separate retail vehicles tripping gates in back-to-back quarters are not, together, consistent with a mature, stable plateau. They are consistent with a trend that has not yet found its ceiling.

Few Understand This

The lead-lag relationship here has not changed since the original thesis, but the lag has started to close faster than the accounting convention was built to handle. BDC equity led. Redemption requests followed. Non-accruals are now confirming both, on a quarter-over-quarter basis, in numbers that keep surprising to the downside relative to where consensus commentary sat even ninety days ago.

Ares Capital reports second-quarter 2026 results on July 29.[20] That print, and the ones from FS KKR, Blue Owl, and Blackstone Secured Lending around it, will be the next test of whether the reported cycle finally catches up to the realized one, or whether the gap keeps widening for another quarter while retail capital keeps discovering, one gated redemption at a time, what patient capital actually costs when it needs to become liquid.

Few understand this.

— — —

Notes

[1] CNBC, “Apollo curbs withdrawals after exit requests hit 17%, reigniting fears over private credit liquidity,” June 23, 2026: Apollo Debt Solutions fund redemption requests of approximately $2.4 billion (16.8% of the fund) in Q2 2026 vs. 11.2% in Q1 2026; 5% gate maintained. https://www.cnbc.com/2026/06/23/apollo-private-credit-fund-withdrawals-redemptions.html

[2] Perplexity Finance OHLCV data: BIZD (VanEck BDC Income ETF) and HYG (iShares iBoxx High Yield Corporate Bond ETF) month-end closes, July 2025 through July 7, 2026. BIZD down approximately 23.2%; HYG down approximately 0.7% over the trailing twelve months.

[3] Perplexity Finance OHLCV data: ARCC (Ares Capital Corporation) closing price history, July 2025-July 2026.

[4] Finsee, “Blue Owl Capital (OBDC) Q1 2026 earnings review”: base dividend cut 16% from $0.37 to $0.31 per share as adjusted net investment income fell to match the reduced payout. https://finsee.ai/earnings/obdc/2026/q1/en/

[5] TigZig, “Private Credit and BDC Stress. Discounts at 13-Year Lows,” June 6, 2026, and Mercer Capital, “Public Prices, Private Marks: What BDC Discounts Are Signaling,” April 9, 2026, aggregated with Perplexity Finance OHLCV data for illustrative estimate of mean BDC price-to-NAV discount. https://www.tigzig.com/post/private-credit-bdc-stress-regulators-jun2026

[6] Fitch Ratings, “U.S. Private Credit Default Rate Hits a High of 6.0% in April 2026,” cited via LinkedIn/Private Credit Solutions summary, June 17, 2026; methodology classifies PIK conversions and maturity extensions as defaults.

[7] Bloomberg, “Private-Credit Defaults Match 2023 High in $300 Billion Index,” June 16, 2026: KBRA DLD Direct Lending Index trailing 12-month default rate at 2.3% of issuers, projected to reach 3.5% (approximately 111 issuers) by year-end 2026. https://www.bloomberg.com/news/articles/2026-06-16/private-credit-defaults-match-2023-high-in-300-billion-index

[8] LSTA, “BDC Quarterly Wrap: 1Q26,” June 9, 2026: weighted-average non-accrual rate for public and non-traded/private BDCs combined rose to 1.99% in Q1 2026 from 1.42% in Q4 2025 and 1.36% in Q1 2025. https://www.lsta.org/content/bdc-quarterly-wrap-1q26/

[9] Octus, “Octus BDC Weekly Roundup: Nonaccruals Jump 40% Sequentially,” June 18, 2026: $9.98 billion in Q1 2026 non-accruals at cost vs. $7.12 billion in Q4 2025 (2.01% of aggregate reported debt investments, up from 1.45%); adjusted estimate of $16.04 billion (3.24%) accounting for likely under-reporting. https://octus.com/resources/articles/octus-bdc-weekly-roundup-061626/

[10] A.L. Capital Advisory, “Private Credit 2026: BDC Crisis, Default Outlook & Safest BDCs,” April 2, 2026, and Forbes, “4 Deeply Discounted BDCs Paying Us Up To 13%,” June 13, 2026: OBDC dividend cut, FSK non-accruals up to 8.1% at cost, BXSL non-accruals at 4.7% of cost with NAV down over 2% quarter over quarter. https://alcapitaladvisory.com/research/intelligence/private-credit.html

[11] Preqin private credit AUM estimates and historical trajectory, 2014-2026; Federal Reserve H.8 release, commercial and industrial loans outstanding at all commercial banks, used for comparative bank lending growth. https://www.preqin.com/insights/global-reports/private-credit-in-2026

[12] Federal Reserve, “Financial Stability Report,” May 2026: accepted redemptions from perpetual BDCs exceeded new inflows in Q1 2026 for the first time since inception; redemption activity characterized as limited and manageable. https://www.federalreserve.gov/publications/files/financial-stability-report-20260508.pdf

[13] Financial Stability Board, “Report on Vulnerabilities in Private Credit,” May 6, 2026: opacity, valuation uncertainty, leverage, liquidity mismatch, and interconnection with banks and insurers flagged as open risks. https://www.fsb.org/uploads/P060526.pdf

[14] A.L. Capital Advisory, “Private Credit 2026: BDC Crisis, Default Outlook & Safest BDCs,” April 2, 2026: Ares Strategic Income Fund (ASIF) capped redemptions at 5% after withdrawal requests of 11.6% of shares in Q1 2026. https://alcapitaladvisory.com/research/intelligence/private-credit.html

[15] FinancialContent/Wedbush MarketMinute, “Blackstone BCRED Navigates Record $3.7 Billion Redemption Wave,” April 6, 2026: BCRED took $3.7 billion in redemption requests (approximately 7.9% of NAV) in Q1 2026; board upsized repurchase limit to 7%. https://markets.financialcontent.com/wral/article/marketminute-2026-4-6-private-credits-leaning-tower-of-liquidity-blackstone-bcred-navigates-record-37-billion-redemption-wave

[16] Solomon Grey Capital, “Private Credit’s Bifurcation: Liquidity Panic, Not a Credit Crisis,” May 5, 2026: Cliffwater Corporate Lending Fund received 17% redemption requests against a 5% cap in Q2 2026. https://solomon-grey-capital.ghost.io/private-credits-bifurcation-liquidity-panic-not-a-credit-crisis/

[17] Senator Elizabeth Warren, Senate Banking Committee hearing, June 11, 2026: warned that AI companies are borrowing upwards of a trillion dollars through private credit funds linked to banks, comparing systemic risk to 2008.

[18] Investing.com, “Earnings call transcript: Barings BDC Q1 2026 earnings miss forecasts, stock rises,” May 8, 2026: non-accruals at fair value approximately 1.0% of portfolio, among the lowest in the industry. https://www.investing.com/news/transcripts/earnings-call-transcript-barings-bdc-q1-2026-earnings-miss-forecasts-stock-rises-93CH-4672950

[19] Solomon Grey Capital, “Private Credit’s Bifurcation: Liquidity Panic, Not a Credit Crisis,” May 5, 2026: Cliffwater Direct Lending Index realized losses of 0.70% for 2025 vs. 1.01% historical average; non-accruals at 1.48% vs. 2.13% long-term norm. https://solomon-grey-capital.ghost.io/private-credits-bifurcation-liquidity-panic-not-a-credit-crisis/

[20] Yahoo Finance/PRNewswire, “Ares Capital Corporation Schedules Earnings Release for the Second Quarter Ended June 30, 2026,” July 2, 2026: earnings scheduled for July 29, 2026. https://finance.yahoo.com/markets/stocks/articles/ares-capital-corporation-schedules-earnings-110000833.html

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.