The Rate Hike Paradox

Markets just priced 70% odds of a Fed HIKE — and ran eight straight up-weeks anyway. The duration playbook just broke.

Special Announcement

A Conversation on the AI Trade Most Portfolios Are Missing — Monday June 1 @ 2pm ET

The AI conversation has fixated on the same six names for two years.

Matt Tuttle thinks the more interesting layer sits one step beneath the hyperscalers — in the **physical infrastructure** that AI cannot exist without.

On Monday, June 1 at 2:00 PM ET, Matt joins the Lead-Lag team for a 60-minute conversation on the **Heavy Assets, Low Obsolescence (HALO)** lens — a way of thinking about businesses with physical assets (mines, railroads, energy companies, and power utilities, for starters) that are unlikely to be disrupted by the next model release.

We’ll discuss:

- What “heavy asset, low obsolescence” actually filters for as a screen

- Why the AI capex cycle may rotate from compute toward heavy assets, infrastructure and materials over the coming years

- Sector-level implications for advisor portfolios

- Live Q&A with Matt Tuttle, Michael Gayed (Lead-Lag), xx, and zz [two RIA partners; will insert names and firm names]

**1.0 hour of CFP CE credit available** (Investment Planning, Intermediate).

📅 Monday, June 1, 2026

🕑 2:00 PM ET

🎥 Live on Zoom

**Register:** https://us06web.zoom.us/webinar/register/WN_FDWhyy9MTMy_wsGO2Tukyw

Hosted by Tuttle Capital Management and Lead-Lag Publishing, LLC. This webinar is educational; no specific product is being marketed.

Disclaimer:

This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided is solely the creation of Tuttle Capital Management. Lead-Lag Publishing, LLC does not guarantee accuracy or completeness. All statements are the sole opinion of Tuttle Capital Management. Past performance does not guarantee future results. Investing involves risk including possible loss of principal. Nothing in this webinar should be construed as a recommendation to buy or sell any security or as personalized investment advice.

The Rate Hike Paradox

KEY HIGHLIGHTS

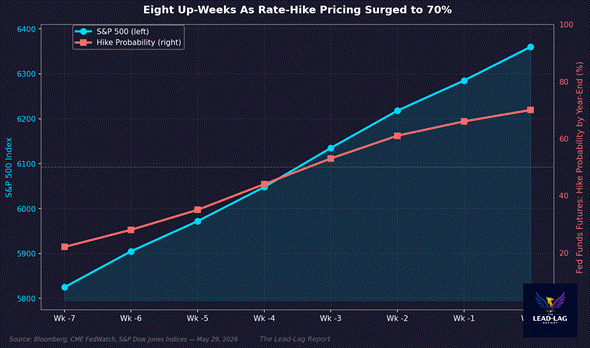

● Fed funds futures are pricing roughly a 70% probability of a rate HIKE by year-end. The S&P 500 has responded by closing at fresh all-time highs for an eighth consecutive week.

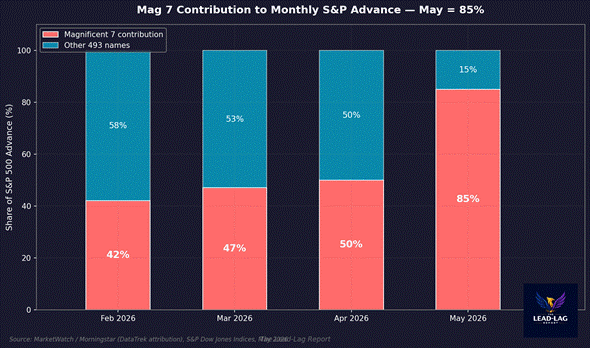

● Textbook duration math says higher-for-longer rates compress growth multiples. Yet the Magnificent Seven contributed 85% of the S&P’s May advance — the highest-duration corner of the market grabbing the bid as a HIKE gets priced in.

● April CPI re-accelerated to 3.8% year-over-year — the highest reading since May 2023 — while the 10-year term premium has risen to roughly 0.83%. The bond market is telling a stagflation-adjacent story; the equity tape is celebrating.

● When markets violate their own textbook in real time, the question is no longer where the consensus is wrong. The question is which tail is being mispriced — and whose portfolio is positioned for the wrong one.

● The most dangerous regimes are not the loud ones. They are the regimes where the price action and the macro data point in opposite directions and nobody can explain why.

— — —

EIGHT UP-WEEKS AGAINST A HIKE

The S&P 500 just closed its eighth consecutive up-week. Fresh all-time highs. The Nasdaq right alongside it. Memorial Day weekend came and went with the index melting up through one round number after another — Dow 50,000, Nikkei 65,000, KOSPI 8,000. The mood music is unambiguous.

And yet, sitting underneath that tape, Fed funds futures are pricing roughly a 70% probability of a rate HIKE by year-end. Not a cut. A hike. Kevin Warsh, sworn in as Fed Chair earlier this month, is on record demanding the Fed defend its credibility against a CPI print that just re-accelerated to 3.8% year-over-year — the highest reading since May 2023.

If you went to bed in early 2024 with the consensus playbook in your head — duration math, growth-tech sensitivity to terminal rate, multiple compression on rising real yields — and you woke up to this tape, you would assume something was broken in your model. Because something is.

The textbook says higher-for-longer rates hurt long-duration assets. The Magnificent Seven are the longest-duration assets in the equity universe. And the Magnificent Seven contributed 85% of the S&P’s May advance. The thing that should be most under pressure is the thing that is leading the tape. The rate-hike trade is not killing growth. It is currently *bidding* growth.

THE DURATION PLAYBOOK IS NOT JUST WRONG. IT IS INVERTED.

Let’s be precise about what is happening, because this matters for how portfolios are positioned.

The 10-year Treasury term premium, as estimated by the San Francisco Fed’s Treasury yield premium series, sat at roughly 0.83% on May 22. That is meaningfully positive. Investors are demanding compensation for the uncertainty of holding long-dated paper. That uncertainty is being driven by exactly the variables you would expect — a CPI re-acceleration, an energy index up 17.9% year-over-year, and a new Fed Chair telegraphing a willingness to move in the opposite direction from the cut consensus.

In any normal cycle, a positive and rising term premium plus a hawkish policy reset is the macro setup that crushes high-multiple growth. We have seen this movie. 1994 under Greenspan. 2018 under Powell. 2022 under Powell again. Each time, the long-duration corner of the market took the heaviest losses.

This time, the long-duration corner of the market is what is making the highs.

There is a story Wall Street is telling itself to explain this — that NVIDIA’s $81.6 billion quarter, 85% year-over-year revenue growth, and Jensen Huang’s $50 to $80 trillion total addressable market commentary make the Magnificent Seven a ‘flight to quality’ destination during macro whipsaws. The earnings, the argument goes, are so dominant that duration sensitivity no longer applies. Cash flows have overtaken discount rates as the dominant variable.

Maybe. Or maybe the market is doing what it always does in late-cycle regimes — narrowing into the smallest possible cohort of names that can still tell a clean story while the macro distribution widens around them. That is not a ‘flight to quality.’ That is a flight to narrative.

SMALL CAPS, BREADTH, AND THE THING THAT IS NOT BEING SAID

Here is the part that is being underreported. Small caps are also rallying. The Russell 2000, by every textbook measure, should hate a rate-hike environment more than any other equity cohort. Higher refinancing costs. Floating-rate debt. Thinner balance sheets. And yet small caps have joined the move.