The Resilience of the U.S. Consumer Is Showing Cracks in the Credit Data

Retail sales remain stable, but rising delinquencies and elevated borrowing costs suggest repayment capacity is weakening at the margin.

Key Highlights

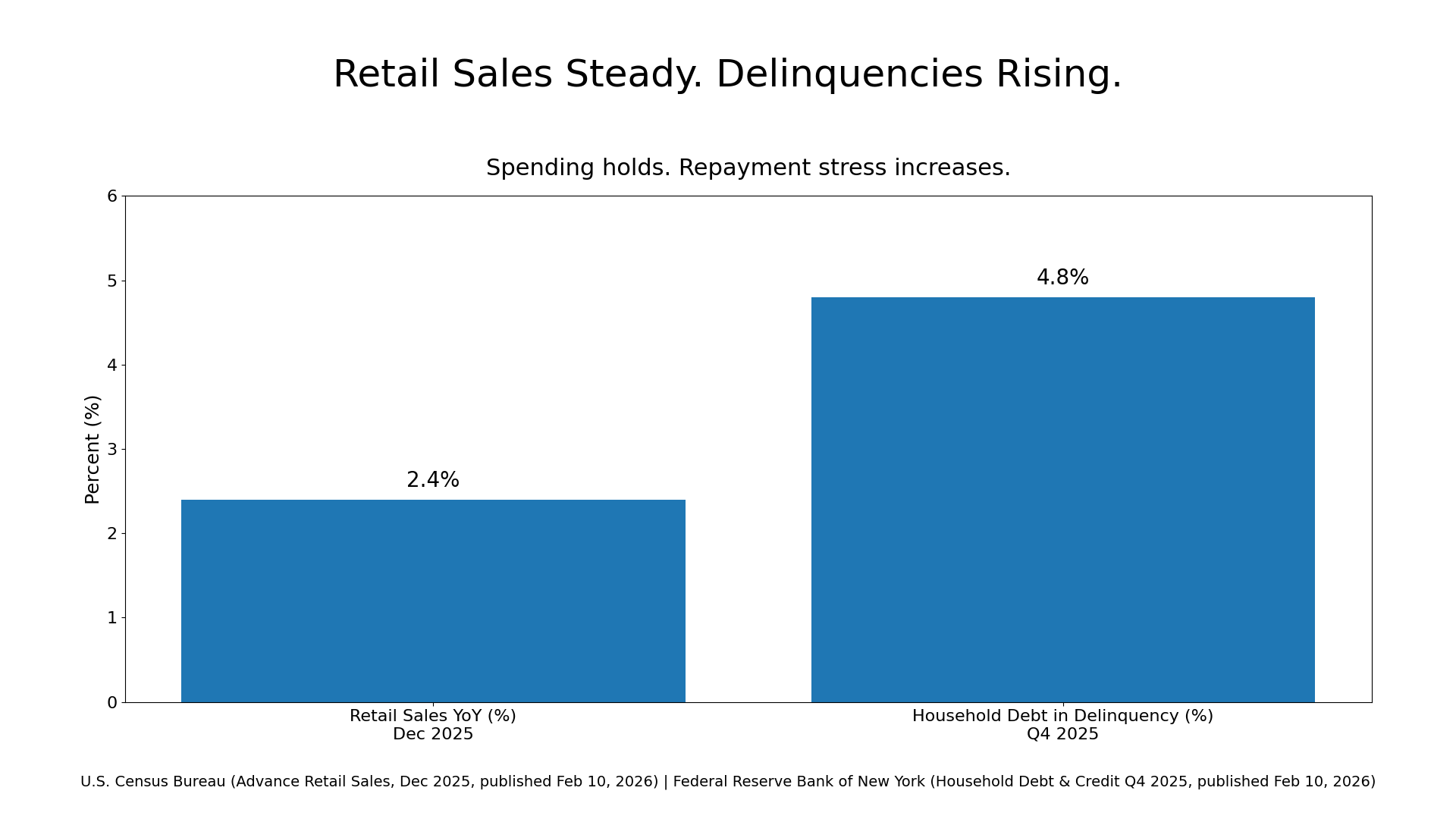

December retail sales held flat month over month and rose 2.4% year over year, yet the figures are not adjusted for price changes.¹

The share of household debt in delinquency increased in Q4 2025, with serious credit card delinquency transitions rising.²

Credit card balances reached roughly $1.28 trillion in Q4 2025, while borrowing costs remain near multi-year highs.³

Auto loan delinquencies have risen across several datasets, including record stress in subprime segments.⁴

Credit deterioration typically transmits to markets through lenders and funding channels before it appears in headline spending data.

Retail Strength Masks Balance Sheet Fragility

On February 10, investors received two signals that, taken together, complicate the narrative of an unshakable U.S. consumer. The U.S. Census Bureau reported December 2025 retail and food services sales of $735.0 billion, essentially unchanged from November and up 2.4% from a year earlier.¹ The same release emphasized that the figures are not adjusted for price changes.¹

Hours later, the Federal Reserve Bank of New York’s Q4 2025 Household Debt and Credit update showed that 4.8% of outstanding household debt sat in some stage of delinquency, up from the prior quarter.² The report also flagged rising serious delinquency transitions for credit cards even as certain non-housing categories leveled out.²

Retail sales capture what households purchased in a given month. They do not capture how that spending was financed, whether balances are being revolved at elevated interest rates, or how close a subset of borrowers sits to payment stress. That distinction matters when borrowing costs remain high and credit utilization carries more weight in supporting consumption.

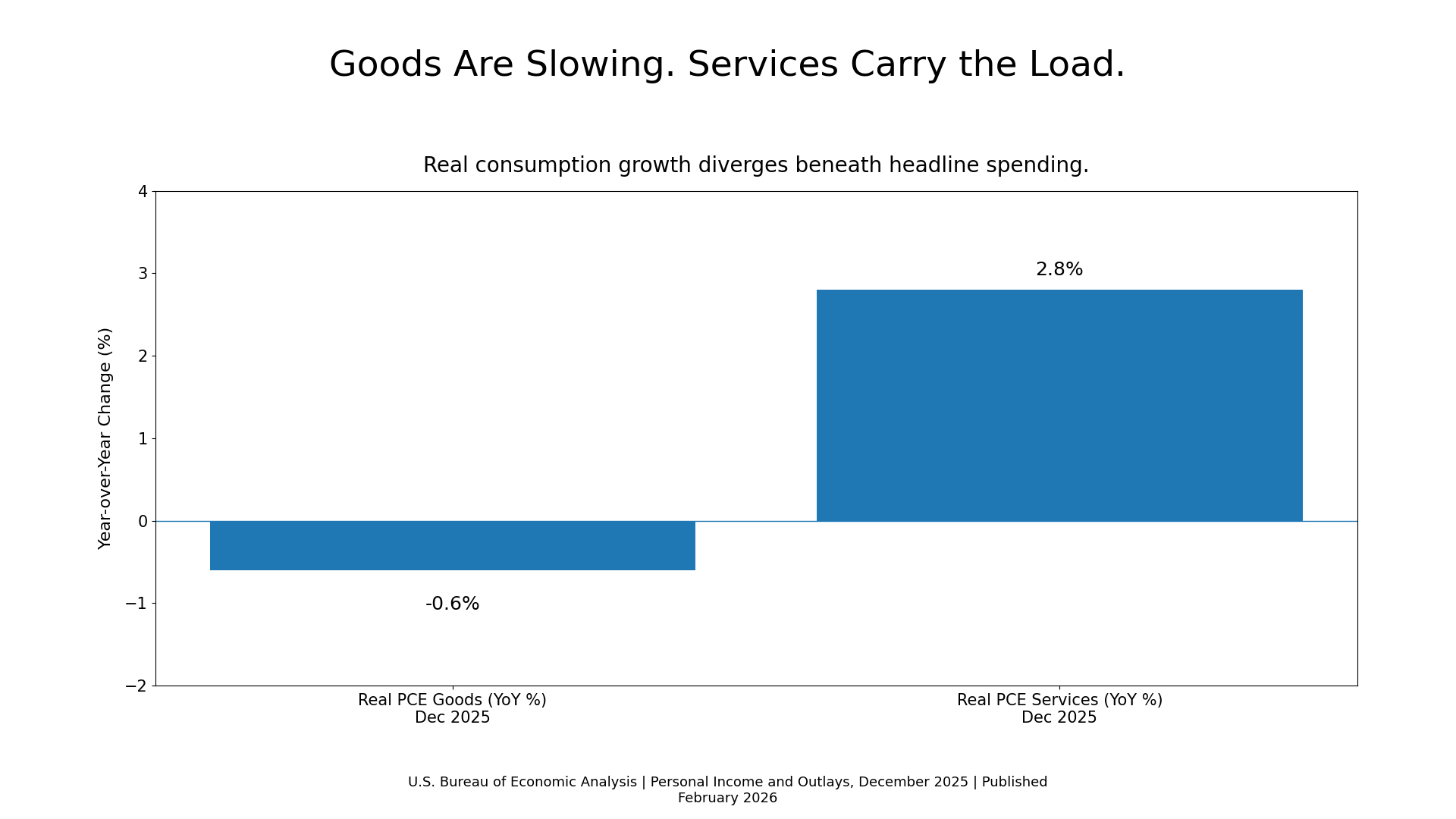

Broader consumption data reinforce the composition issue. The Bureau of Economic Analysis’ December 2025 Personal Income and Outlays release showed that growth in current-dollar personal consumption expenditures was driven by services, while goods spending declined.⁵ Real PCE increased only modestly.⁵ Retail sales, concentrated in goods and a narrow slice of services, therefore provide an incomplete read on household balance sheet pressure.

Meanwhile, the Federal Reserve’s G.19 consumer credit report for December 2025 showed that revolving credit continued to expand, with December growth exceeding the fourth-quarter pace.⁶ Credit growth is not, by itself, evidence of distress. Yet in a high-rate environment, expanding revolving balances raise the base upon which delinquencies and interest burdens compound.

The structural risk is straightforward: nominal spending can remain steady while repayment capacity erodes at the margin. That erosion tends to appear first in delinquency rates, minimum-payment behavior, and lender underwriting decisions—long before a collapse in store receipts.

Credit Card Expansion Meets Elevated Delinquency Risk

Credit cards sit at the center of this divergence because they allow households to sustain spending even as cash flow tightens. The New York Fed reported that credit card balances increased by $44 billion in Q4 2025 to roughly $1.28 trillion, with total household debt approaching $18.8 trillion.³ Rising balances in isolation are not unusual. Rising balances alongside elevated borrowing costs warrant closer scrutiny.

Borrower-level delinquency data point to stress that is no longer improving cleanly. TransUnion’s Q4 2025 Credit Industry Insights release reported a 90+ days past due credit card delinquency rate of 2.58% at the borrower level and noted a recent uptick after several quarters of year-over-year improvement.⁷ Issuers, according to the same release, expanded balances while managing risk by assigning lower initial credit limits to below-prime accounts.⁷ That approach supports growth while containing exposure, yet it signals active portfolio management in response to performance concerns.