The S&P 500 Is at a Record High. The Question Is How to Get Paid While Holding It.

How a Daily 0DTE Covered Call Strategy on SPY Converts the Market’s Volatility Premium Into a Daily Paycheck

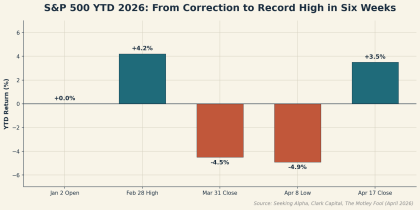

The S&P 500 closed at 7,126 on April 17, 2026, a new record high following 13 consecutive higher closes. [1] That capped one of the more jarring round trips in recent memory. Three weeks earlier, the index finished March down 4.98% for the month—its worst monthly print since April 2025—and sat roughly 4% lower on the year by the start of April. [2] The VIX1 touched 30.19 intraday on March 9 before receding to 18.87 by April 20. [3] Six weeks. A 5% drawdown. A 13-day winning streak. A new all-time high.

Figure 1: S&P 500 YTD 2026 — correction to record high in six weeks

For investors accustomed to a benchmark that only goes up, the last sixty days have been a reminder of something income investors figured out long ago. In a market that can swing between correction and record high in a quarter, the most reliable return source is often not the direction of the index but the premium the market pays for uncertainty. Options premiums. Harvested daily. On an S&P 500 chassis most investors already own.

The Market Most Investors Thought They Bought

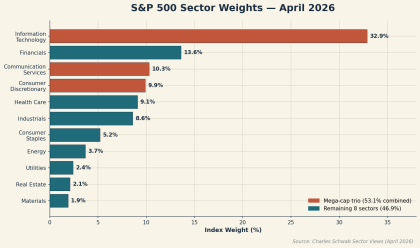

The S&P 500 is not the index it was two years ago. As of early April 2026, information technology alone represented 32.9% of the index by weight, with communication services adding 10.3% and consumer discretionary 9.9%. [4] The top five names—NVIDIA, Apple, Microsoft, Amazon, Alphabet—account for roughly a quarter of the entire index on their own.2 [5] When investors buy “the market,” they are buying an increasingly concentrated bet on a

small number of mega-cap companies whose earnings trajectories are more correlated than at any point in the modern era.

Figure 2: S&P 500 sector weights, April 2026 — the mega-cap trio accounts for 53.1%. Past performance does not guarantee future results.

This has consequences for income. The index’s dividend yield has been compressed to roughly 1.1%—one of the lowest readings since the late 1990s and a fraction of the multi-decade average near 1.7%. [6] The companies driving the index don’t need to pay dividends to attract capital, so

they don’t. Ten-year Treasury yields sit near 4.13%, and the Fed Funds rate stands at 3.50– 3.75%, meaning investors who shift to bonds give up equity participation entirely. [7] The gap between what the market offers and what investors require is widening, not closing.

The Income Opportunity Hidden in Plain Sight

Options-based ETFs have quietly become one of the most important structural developments in modern portfolio construction. Goldman Sachs Asset Management reports derivative income ETFs were the top flow-gaining category within active ETFs in 2025. [8] Investors, in short, will pay a premium to convert volatility into cash flow.

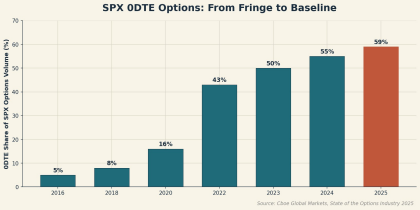

The mechanic is not new—selling calls against an equity position to generate income has existed in institutional portfolios for decades. What has changed is the chassis. Zero-days-to expiration options—0DTE—have gone from roughly 5% of S&P 500 options volume in 2016 to averaging 2.3 million SPX contracts per day in 2025, representing 59% of total SPX options volume. [9] These are no longer exotic. They are the baseline of how the S&P 500 options market functions.

Figure 3: SPX 0DTE options have grown from fringe (5% of volume) to baseline (59%)

The appeal of 0DTE for income generation is rooted in theta decay3—the accelerating rate at which an option loses value as expiration approaches. A call that expires at the close of the same day it is written delivers the maximum possible rate of time decay to the seller. For a strategy designed to harvest that decay, daily expiration is not a feature. It is the entire design.

The Mechanics of a Daily Cadence

The TappAlpha SPY Growth & Daily Income ETF (TSPY) holds SPY—the SPDR S&P 500 ETF Trust—and writes out-of-the-money call options4 against it every trading day, with each option expiring at the close of that same session. [10] Each morning, the strategy resets. Each evening, the options expire. The premium collected becomes income. The next day, the process begins again.

Three features of this design matter. First, the daily expiration cycle means the fund is not locked into a directional view that can go stale. When the S&P 500 sold off in March and then reversed, the strategy reset its strike selection at the new level rather than being trapped at a higher price. Second, the daily cadence transforms income from a single monthly event into a continuous stream—a structural change for investors who depend on cash flow. Third, because the options expire the same day, the options book carries no overnight event risk.

Why This Market Makes the Case

The current environment makes a strong case for broad-market options income. Three dynamics stand out. The VIX closed at 18.87 on April 20, off its March high above 30 but still elevated relative to the 12–14 readings that dominated 2024—richer premiums translate more cleanly into distributions. [3] S&P 500 Q1 2026 earnings growth is running at 13.2% blended, the sixth consecutive quarter of double-digit growth, which gives the underlying index a fundamental floor. [11] And the breadth of the rotation underway—some sectors leading, others lagging—rewards covered call strategies on the full index over narrow single-name overlays.

The Trade-Off You Need to Understand

No strategy is a free lunch. The most important cost of a daily covered call program is upside participation. If the S&P 500 rallies sharply in a single day on a Fed pivot or earnings surprise, the written calls will limit the fund’s participation. In a relentless, momentum-driven bull market, an unhedged SPY position will outperform TSPY over time. That is the design, not a flaw.

Because TSPY’s underlying holding is SPY, the fund also inherits all of the S&P 500’s characteristics: concentration in mega-cap technology, cyclicality, and full exposure to index level drawdowns. If the S&P 500 falls 10%, TSPY will decline substantially alongside it, only partially offset by premium collected during the drawdown. Investors should view TSPY as an income-generating complement to equity exposure, not a replacement for diversification or risk management.

Where TSPY Fits in a Portfolio

TSPY is best understood as an allocation decision rather than a trade. For income-oriented investors, it offers a structural source of cash flow tied to the S&P 500 without requiring the index to rise. For growth-oriented investors, the fund can serve as a yield-enhancement sleeve within a broader large-cap allocation, generating income that can be reinvested or used to rebalance into lagging parts of the market. The fund currently expects, but does not guarantee, monthly distributions funded, in part, by the daily premium harvest. [10]

TSPY’s three-holding structure—overwhelmingly SPY alongside a small cash position and the daily options book—keeps the strategy transparent. Listed on the Nasdaq since August 14, 2024, TSPY has roughly $132.6 million in AUM and carries a 0.77% expense ratio. [12]

The S&P 500 is at a record high. The question is no longer whether to own it. It is how to get paid while you do.

Definitions and Disclosures:

1The Cboe Volatility Index, or VIX, calculates the implied volatility—how much and how quickly prices are expected to change—of the S&P 500 Index (SPX).

2TSPY does not directly hold the securities mentioned but may have indirect exposure through its underlying exposure.

3Theta decay is the rate at which an option loses value as time passes, assuming all else stays equal.

4An out-of-the-money (OTM) call option is a call option where the strike price is above the current market price of the underlying asset.

This content is sponsored by TappAlpha. The Lead-Lag Report has been compensated for the publication of this material. The views and opinions expressed herein are those of the author and do not necessarily reflect the views of TappAlpha or its affiliates.

This material is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy, sell, or hold any securities, including TSPY.

The fund currently expects, but does not guarantee, to make distributions on a monthly basis. Distributions may exceed the fund’s income and gains for the taxable year. Distributions in excess of the fund’s current and accumulated earnings and profits will be treated as a return of capital.

Investors should carefully consider the investment objectives, risks, charges and expenses of the ETF. This and other important information about the Fund are contained in the prospectus, which should be read carefully before investing.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Returns less than one year are not annualized.

Investing involves risk. Principal loss is possible. The Fund’s shares will change in value, and you could lose money by investing in the Fund. The Fund may not achieve its investment objectives. The Fund invests in options contracts that are based on the value of the Index. This subjects the Fund to certain of the same risks as if it owned shares of companies that comprised the Index, even though it does not own shares of companies in the Index. The Fund will have exposure to declines in the Index. The Fund is subject to potential losses if the Index loses value, which may not be offset by income received by the Fund.

Due to the short time until their expiration, 0DTE options are more sensitive to sudden price movements and market volatility than options with more time until expiration. The timing of trades utilizing 0DTE options becomes more critical. 0DTE options may also suffer from low liquidity, making it more difficult for the Fund to enter into its positions each morning at desired prices. The bid-ask spreads on 0DTE options can be wider than with traditional options, increasing the Fund’s transaction costs and negatively affecting its returns.

Distributor: Foreside Fund Services, LLC, Member FINRA.

Footnotes

1. Seeking Alpha, “S&P 500 Clocks New Record High As Near-Record Winning Streak Continues,” April 20, 2026.

2. Clark Capital Management Group, Benchmark Review & Monthly Recap, March 2026, April 6, 2026; The Motley Fool, “The S&P 500 Is Down 4% in 2026,” April 5, 2026. 3. Federal Reserve Bank of St. Louis (FRED), CBOE Volatility Index, observation for April 20, 2026; Barchart S&P 500 VIX March 2026 futures data.

4. Charles Schwab, “Sector Views: Monthly Stock Sector Outlook,” April 3, 2026. 5. Slickcharts, S&P 500 Components by Weight, April 2026.

6. Multpl, S&P 500 Dividend Yield by Month, April 2026; TheStreet, “S&P 500 index dividend yield hits nearly 50-year low,” April 15, 2026.

7. Federal Reserve Economic Data (FRED), 10-Year Treasury Constant Maturity Rate and Federal Funds Effective Rate, April 2026.

8. Goldman Sachs Asset Management, “Why 2026 will be another big year for derivative income & defined outcome ETFs,” February 2026.

9. Cboe Global Markets, “The State of the Options Industry: 2025.”

10. TappAlpha, TSPY Fund Prospectus, April 30, 2025.

11. FactSet, “S&P 500 Earnings Season Update,” April 17, 2026.

12. TappAlpha, TSPY fund page, April 2026; Stock Analysis, TSPY ETF data, April 2026.

DISCLAIMER – PLEASE READ: This is a sponsored article for which Lead-Lag Publishing, LLC has been paid a fee. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the article or make any representation as to its quality. All statements and expressions provided in this article are the sole opinion of TappAlpha and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the discussion. The content in this writing is for informational purposes only. You should not construe any information or other material as investment, financial, tax, or other advice. A participant may have taken or recommended any investment position discussed, but may close such position or alter its recommendation at any time without notice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer to buy or sell any securities or other financial instruments in any jurisdiction. Please consult your own investment or financial advisor for advice related to all investment decisions.