Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

It seems that there is no shortage of “enhanced income” strategies being launched today in the fund industry. Most fall under the umbrella of covered call strategies, but even these have gotten bolder. The traditional covered call funds that add a 50-100% option overlay using monthly call contracts seem passé nowadays. Today, we’ve got 0DTE products that can produce annualized yields of 60% to 100% and, in some cases, even more!

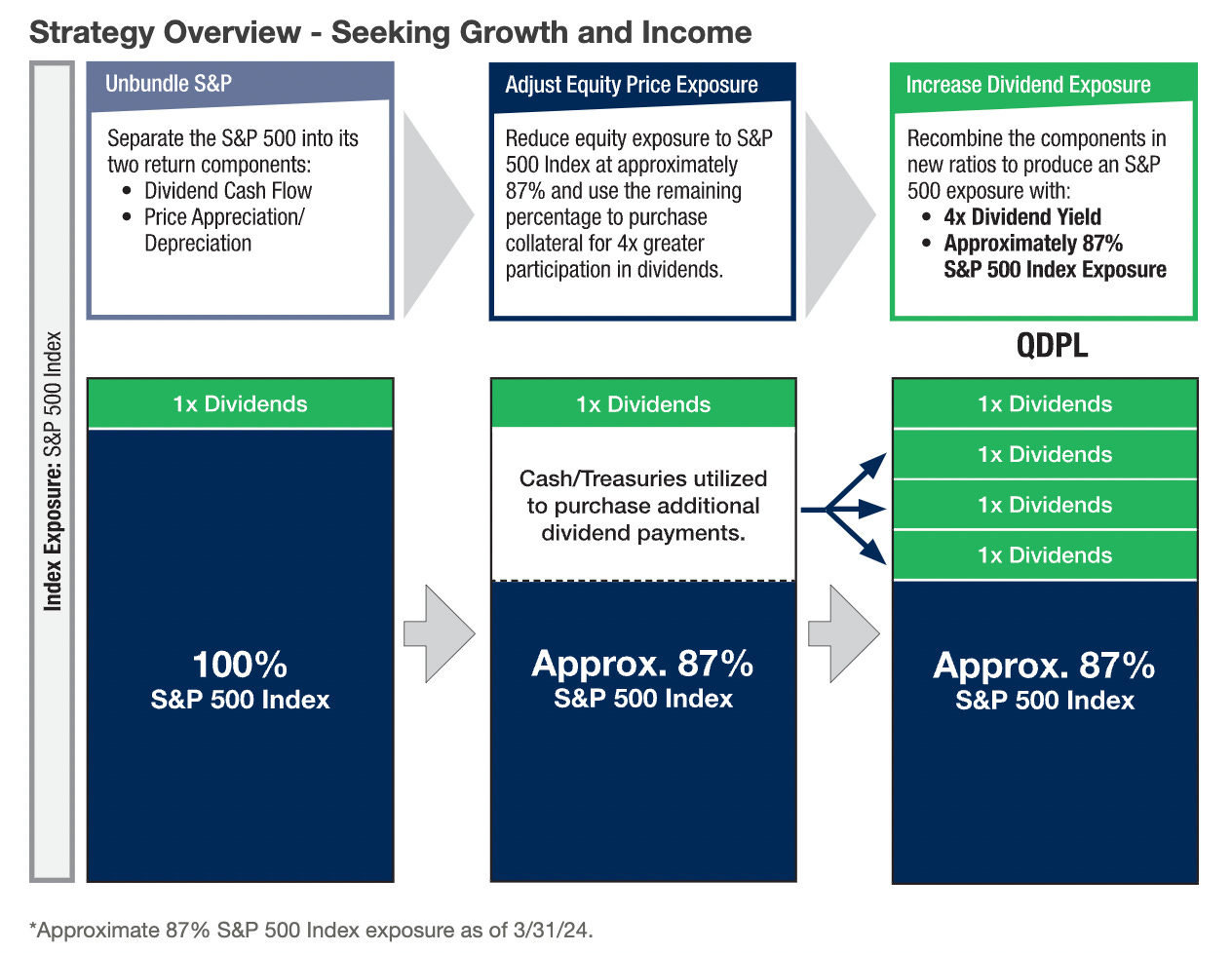

Another income strategy that’s a little further under the radar involves using futures contracts to multiply dividend income exposure. The risk/return profile looks at least somewhat similar to a covered call strategy, but they’re structured much differently. This is the strategy utilized by the Pacer Metaurus U.S. Large Cap Dividend Multiplier 400 ETF (QDPL). You may be able to figure out what the fund is trying to accomplish based on the name alone, but it’s an interesting one based on its more unique approach. Instead of trying to generate high income via options premiums, it’s generating high income based on multiplying equity dividends instead. It’s a strategy interesting enough because it appears to be working.

Fund Background

QDPL tracks an index based on the stocks in the S&P 500 index; long S&P dividend futures contracts and 3-year Treasuries. The objective is to provide 400% of the ordinary yield of the S&P 500 in exchange for reduced participation in the price performance, currently about 87% of the index’s performance.

The big difference between QDPL and a traditional covered call strategy is the upside/downside capture and the yield. QDPL aims to deliver approximately 87% of the S&P 500’s performance and if you look at upside/downside capture ratios over the past year, it does a pretty effective job of this. If you look at the Global X S&P 500 Covered Call ETF (XYLD), which uses a 100% option overlay, it has approximately 50% upside/downside capture. Its sister fund, the Global X S&P 500 Covered Call & Growth ETF (XYLG), which uses a 50% option overlay, has about a 75% upside/downside capture. Therefore, it’s reasonable to expect QDPL to be a bit more volatile.

XYLD yields about 10% right now, thanks to the high option income, while XYLG is at around 5% (these used to be around 12% and 6%, respectively, but lower S&P 500 volatility means lower option premiums). QDPL is at around 5.7% right now, although it’s been above 6% in the recent past.