The Small-Cap Rotation Is Real

Plus, A New Geopolitical Risk Reshuffles The Deck

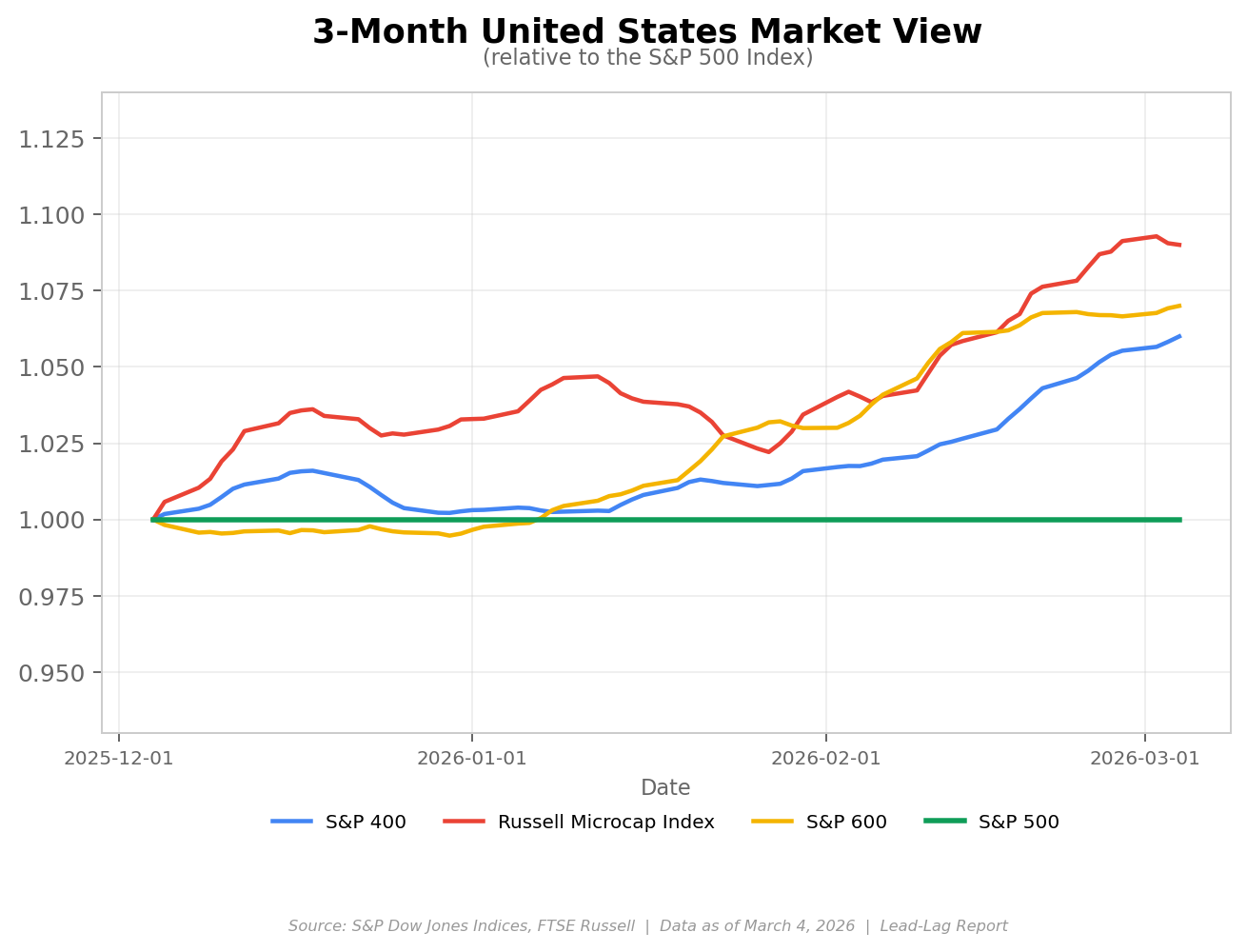

The above chart tells the story that many have been waiting to see for quite some time. Small-caps, mid-caps and micro-caps have been dramatically outperforming the S&P 500 over the past three months in what looks like a meaningful and potentially durable rotation. The S&P 600 is up roughly 9% year-to-date, the S&P 400 has gained more than 8%, and the Russell Microcap Index continues to lead the charge. Meanwhile, the S&P 500 is essentially flat on the year. Energy and materials have been the best performing sectors, while tech and financials have actually lagged. Value is handily beating growth for one of the first times in several years. For those who have been pounding the table on small-caps, this is starting to look like the real deal.

What’s driving this? The Fed’s rate cutting cycle, which has brought the funds rate down to 3.50-3.75%, is clearly benefiting smaller, more rate-sensitive companies. The January CPI reading came in at 2.4% year-over-year, suggesting that inflation is cooperating enough for the Fed to keep cutting. The market is pricing in roughly a 97% probability that the Fed holds steady at its March meeting. Before the Iran conflict escalated, futures were pointing to about a 48% probability of a rate cut by June, but the spike in oil prices and renewed inflation fears have since pushed the next expected cut out to September. If those cuts materialize later this year, it could add further fuel to the small-cap rally. The labor market, however, is something to watch. January payrolls came in at 130,000, which beat estimates, and the unemployment rate edged lower to 4.3% from 4.4% in December. It’s not alarming, but the trend is worth monitoring, especially for smaller companies that tend to feel labor market shifts more acutely.

One area of concern is the core PCE reading, which came in at 3.0% in December and has been trending upward. If that continues, it could complicate the Fed’s path forward and call into question whether additional cuts are truly justified. For now, the market seems comfortable with the idea that rate cuts are coming and the economy is holding up, but any shift in that narrative could disrupt what’s been one of the cleanest small-cap rotations we’ve seen in years.

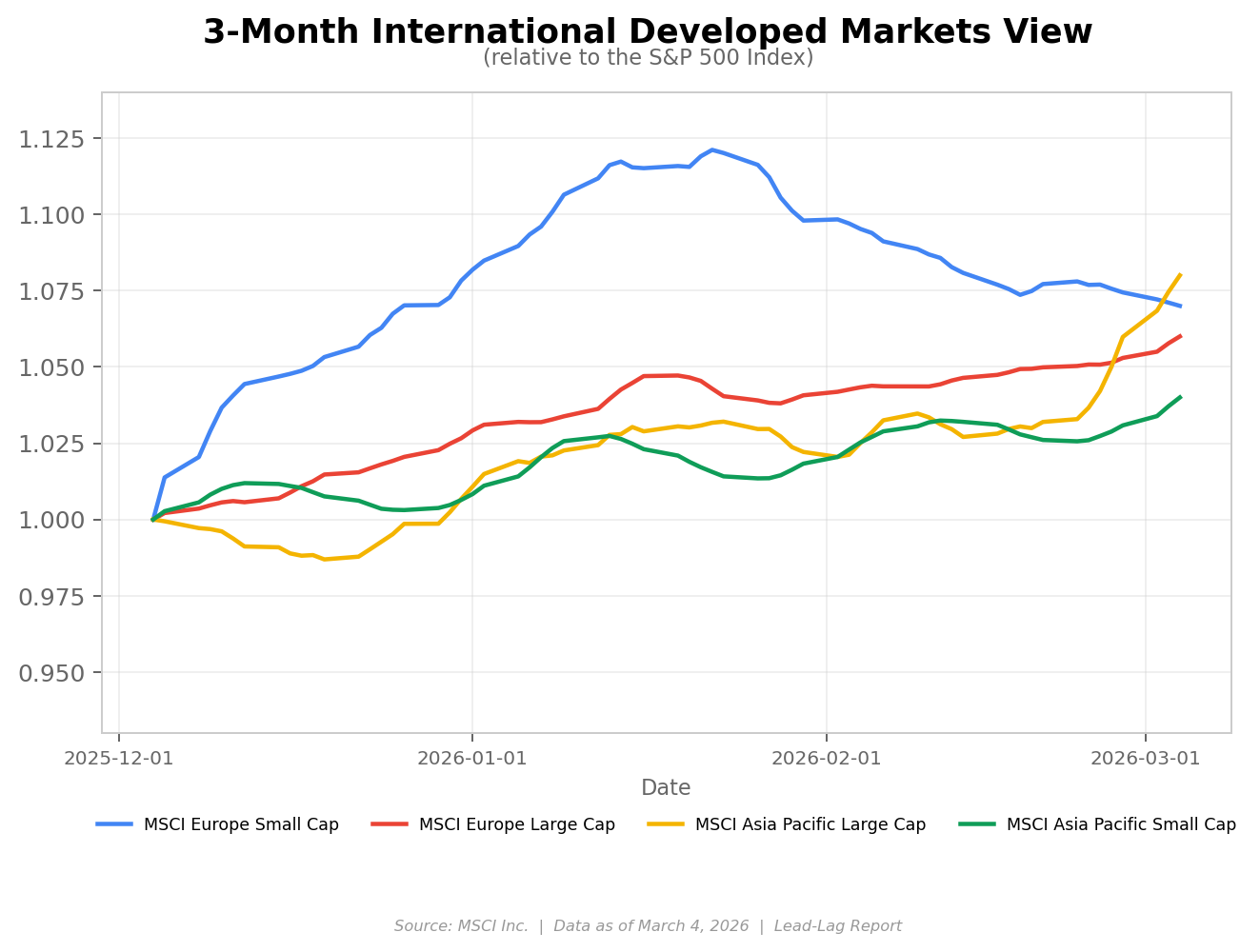

International developed markets have been outperforming the S&P 500 here and it’s not even close. European stocks posted more than 5% gains year-to-date before the recent sell-off tied to the Iran conflict, with the STOXX 600 hitting a new all-time high of 630 in mid-February. MSCI Asia Pacific is up similarly. In dollar terms, MSCI Europe has actually outpaced the S&P 500 by a wide margin over the past 12 months. This is a reversal of the U.S.-dominated leadership we saw for most of the prior decade. Germany’s massive fiscal package is a significant catalyst. A €500 billion off-budget infrastructure fund covering transport, digitalization, energy and hospitals, combined with a defense budget that has surged by roughly €25 billion this year to €119 billion total, is reshaping the investment landscape. After six consecutive years of economic stagnation, Germany is finally spending its way back toward growth. Goldman Sachs is projecting 1.1% GDP growth for the country this year, which isn’t spectacular, but represents a meaningful inflection point.

The ECB has held rates steady at 2.0% for five consecutive meetings now, and with Eurozone headline inflation ticking back up to 1.9% in February, there’s little pressure to cut further. In fact, the Iran conflict and the associated energy price shock have all but eliminated any residual chance of a near-term cut. Deutsche Bank’s base case now calls for the ECB to hold at 2% through 2026, with the next move potentially a hike in mid-2027. If the ECB remains on hold while the Fed is still cutting, it creates an interesting dynamic that should continue to support European equities relative to U.S. stocks in the near term.

Japan’s situation is perhaps the most fascinating one right now. The country narrowly avoided a technical recession with Q4 GDP coming in at just 0.1% quarter-over-quarter. Headline CPI has actually fallen below 2% for the first time since March 2022, which is notable given how much trouble elevated inflation has caused. Prime Minister Takaichi, Japan’s first female PM, won the snap election on February 8 with the LDP securing a commanding 316-seat supermajority in the lower house. The BoJ held rates at 0.75% in January, and while Governor Ueda flagged the March and April meetings as live for a potential hike, the Iran conflict has made a March move far less likely. Polymarket puts the odds of a March hike at just 5%. If the BoJ does hike later this spring while the yen remains weak around the 156-157 level, it could set up another round of carry trade unwind dynamics that rattled markets last summer.

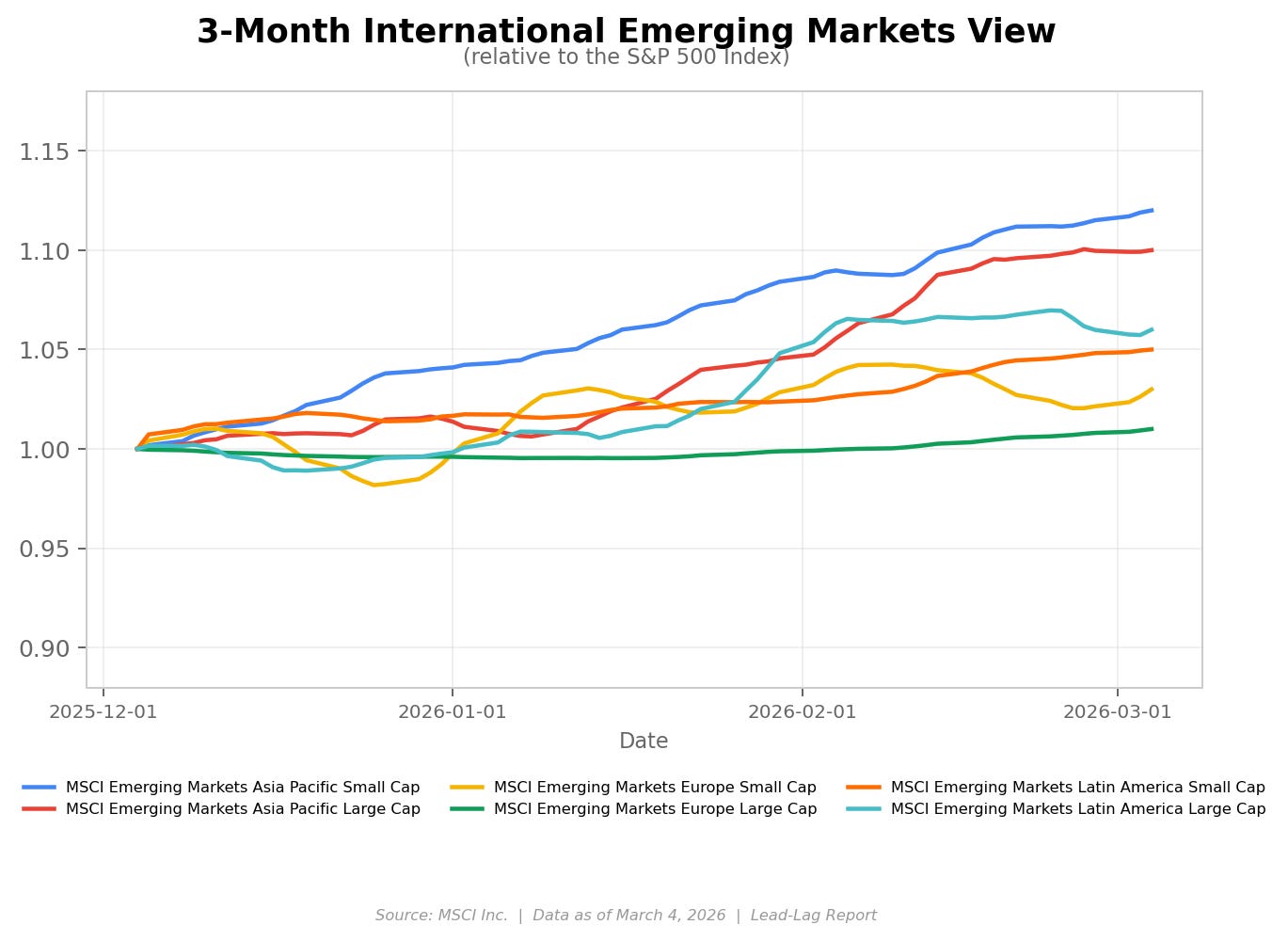

Emerging markets have been the surprise story of the year so far. MSCI Emerging Markets is up roughly 14% year-to-date, the best start to a year since 2017. Asia Pacific EM has been leading the way, driven largely by the AI and semiconductor boom. The Supreme Court’s decision to strike down IEEPA tariffs in February was a game changer. Trump quickly pivoted to invoking Section 122 at 15%, but the trade-weighted average tariff has effectively come down, which is a meaningful reduction from where things stood last year. For many emerging markets, this has been an enormous relief.

India has been one of the biggest beneficiaries. The landmark U.S.-India trade deal signed in February slashed tariffs from 50% down to 18%, which immediately boosted Indian equities. The macro story is compelling too. The RBI is projecting 7.4% GDP growth for FY26, CPI inflation has plunged to just 1.33% in December, and the repo rate stands at 5.25% after multiple cuts during 2025 with the central bank maintaining a neutral stance. India looks like it’s in the sweet spot right now where growth is accelerating while inflation has come fully under control. China, on the other hand, is a more complex picture. The NPC has convened and is expected to set a growth target around 5%. Q4 GDP growth slowed to 4.5% year-over-year, the weakest in nearly three years, and the manufacturing PMI data has been mixed. The PBoC is signaling a moderately loose stance for 2026, but domestic demand remains the persistent drag. The one-year tariff truce with the U.S. holds through November, and there’s a Trump-Xi summit expected at the end of March, which could be an important signpost for the relationship going forward.