Today’s Lead-Lag Report post is sponsored by Evoke

The future is highly uncertain, with potential challenges in growth, inflation, and geopolitics, making diversification crucial.

Most investors are unknowingly underdiversified. A traditional 60/40 portfolio is 98% correlated to the stock market, potentially exposing investors to more risk than they realize. The S&P 500 historically experienced extended periods of underperformance, including:

1. Underperforming cash from 1966 to 1982 during inflationary times

2. A 0% average return from 1929 to 1949

3. A lost decade prior to the recent 15-year bull market

Historical bear markets often started with high valuations. Given current high valuations, we may be on the verge of another challenging period for U.S. equities.

Risk parity seeks to offer a more diversified allocation than conventional mixes. By spreading risk across global equities, Treasuries, TIPS, and commodity producers and gold, investors can maintain a low-cost, tax-efficient passive mix seeking:

1. Equity-like long-term expected returns

2. Lower risk than stocks

3. Reduced risk of a lost decade

To learn more about the RPAR Risk Parity ETF, visit rparetf.com.

Before investing you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. This and other information is in the prospectus. A prospectus may be obtained by clicking here. Please read the prospectus carefully before you invest.

Investing involves risk. Principal loss is possible.

Distributed by Foreside Fund Services, LLC.

Data source: Bloomberg.

DISCLAIMER – PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC has been paid a fee. The information provided in the link is solely the creation of Evoke Advisors. Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided in the link or make any representation as to its quality. All statements and expressions provided in the link are the sole opinion of Evoke Advisors and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided in the link.

The Warsh Regime

KEY HIGHLIGHTS

• On June 17, Kevin Warsh chaired his first FOMC meeting and presided over a unanimous 12-0 hold in the 3.50% to 3.75% range. The statement was cut from 341 words to roughly 130, and every word of easing bias and forward guidance was removed. Consensus filed it as a procedural pause. It was a change in the reaction function.

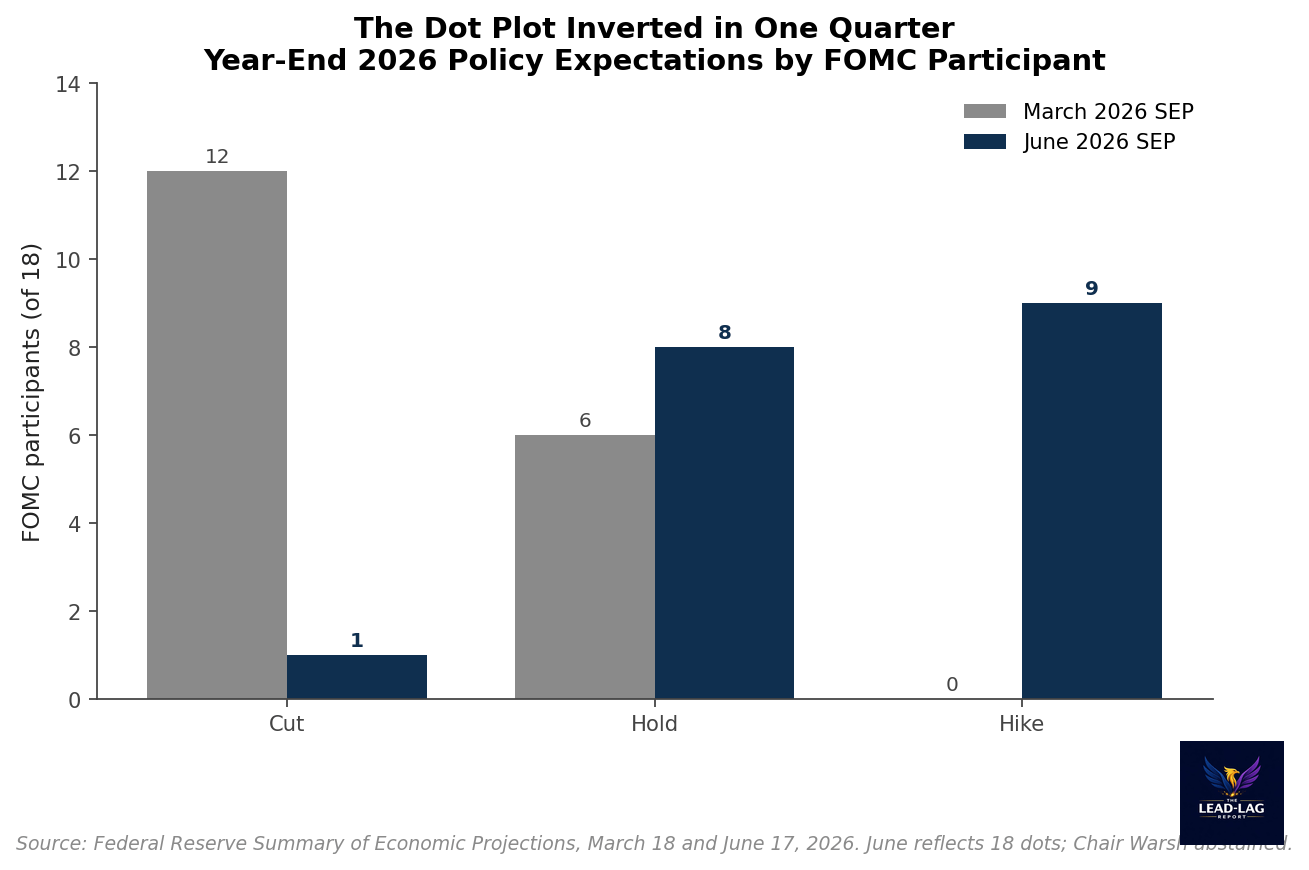

• The dot plot inverted in a single quarter. In March, twelve of eighteen participants expected at least one cut and none expected a hike. In June, nine expected at least one hike, eight expected a hold, and only one still saw a cut. That is the largest single-meeting hawkish swing since the projections began in their current form.

• The June Summary of Economic Projections raised year-end Core PCE from 2.7% to 3.3%, lifted headline PCE from 2.7% to 3.6%, cut real GDP to 2.2%, and pushed the return to the 2% target out to 2028. Goldman Sachs scrapped its 2026 cut calls outright and moved them into 2027.

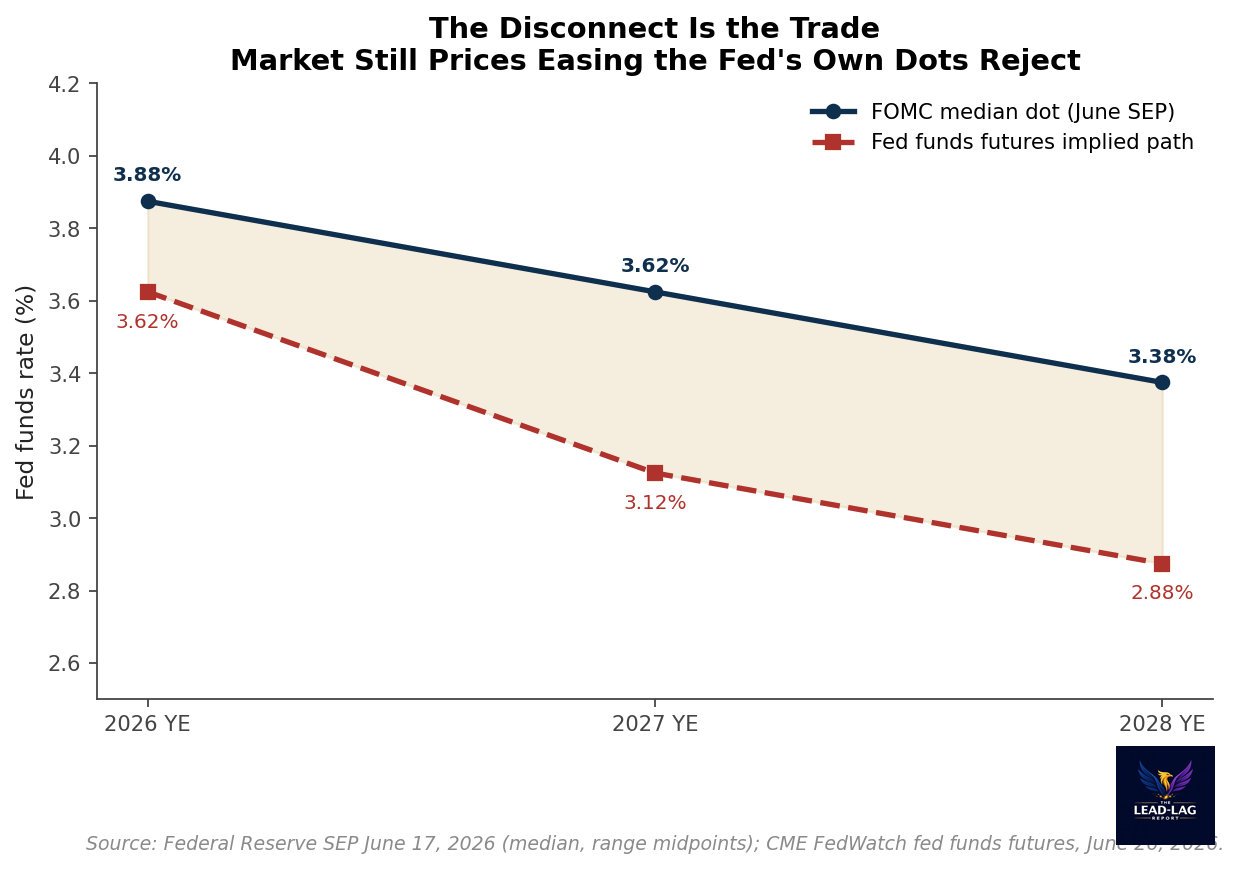

• Fed funds futures still imply easing inside twelve months despite all of it. The market is pricing the hold as a temporary stance. The Fed has restored its right to hike asymmetrically and consensus has not updated. That gap is the trade.

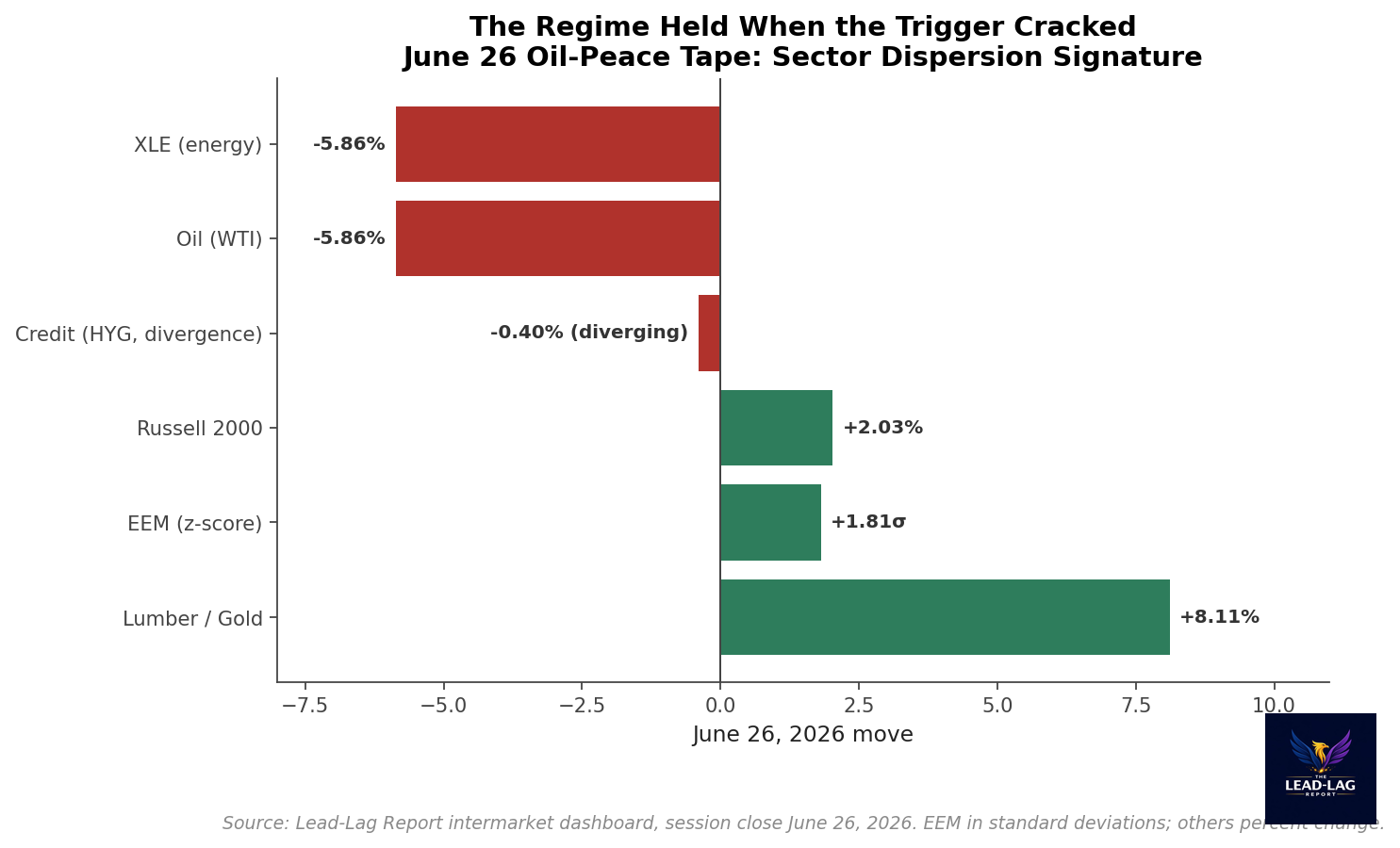

• On June 26, the inflationary trigger cracked. Oil collapsed and energy was the worst sector at -5.86%, yet the regime read held: credit began diverging, emerging markets ran +1.81 standard deviations, the Russell rose +2.03%, and the lumber-to-gold ratio jumped +8.11%. The signature survived the loss of its catalyst.

There is a particular kind of denial that takes hold when a central bank changes its mind faster than the people who watch it. The institution moves. The framework shifts. The language is rewritten. And the market, conditioned by a decade of being rescued, treats the move as a temporary deviation that will mean-revert the moment the data gives anyone an excuse. The gap between what the central bank has decided to be and what investors insist it still is gets wide enough that one side has to capitulate. It is rarely the central bank that blinks first.

That gap is open right now, and it has a name. On June 17, Kevin Warsh chaired his first meeting of the Federal Open Market Committee and the Committee voted unanimously, 12-0, to hold the federal funds rate in its 3.50% to 3.75% range.[1] The financial press reported a hold. That is technically accurate and almost entirely beside the point. The hold was the least interesting thing that happened in that room. What happened underneath the hold was a doctrinal reset, the kind that does not come along in most careers, and the market is still pricing it as a one-meeting reaction to a hot inflation forecast.

I argued the first half of this case in two recent notes, Warsh’s First Strike on June 24 and Peace Broke Out, So Did The Hawkson June 26. This piece consolidates them. The June meeting was not a tactical pause the Fed will unwind once oil rolls off and inflation cools. It was the first expression of a new reaction function. The unanimous vote, the surgical removal of the easing language, and a twelve-vote swing in the dot plot from a cutting bias to a hiking bias inside ninety days are not transitory hawkishness. They are the regime.

The Statement Told You Before the Dots Did

Begin with the document, because the document is where intent lives. The post-meeting statement was cut from 341 words to roughly 130, and in the editing the Committee removed the language that had signaled a bias to ease.[2] There was no reference to additional adjustments, no conditional promise that policy would lean toward accommodation as conditions allowed. Warsh has said for years that he does not believe in date-based or data-tied forward guidance, and at his first opportunity he stripped it out and left a statement that ends on the Committee’s commitment to price stability. He then declined to submit his own dot to the projection materials, calling the tool ill-suited to the present policy context, and announced task forces to review communications, the balance sheet, data sources, productivity, and the inflation framework itself.[3] This is not the housekeeping of a caretaker. It is a chair rebuilding the machine.

None of this is in dispute as a matter of record. The statement is published, the word count is verifiable, the transcript is archived. What is in dispute is interpretation. The dominant read is that Warsh inherited a hot print and an oil shock, reacted to both, and will revert to the prior easing path once the supply side calms. I am arguing the opposite. The framework changed first, and the data merely gave the new framework an unambiguous moment to announce itself.

Forward guidance was never a neutral convenience. It was a commitment device. By telling markets which direction the next move would lean, the Fed surrendered optionality in exchange for easing financial conditions without spending a basis point. Removing it does the opposite. It restores the Committee’s right to surprise, and specifically its right to surprise in the hawkish direction. A Fed that has deleted its easing bias has told you, in the only language it uses without breaking discipline, that the next move is no longer presumed to be down. That is the asymmetry consensus has not absorbed.

Twelve Votes in Ninety Days

The dot plot is the cleanest evidence. In March, twelve of eighteen participants expected at least one cut by year-end 2026 and not a single participant expected a hike.[4] By June the distribution had inverted. Nine participants now expect at least one hike before year-end, eight expect a hold, and exactly one still pencils in a cut.[5] Six of the nine hike-leaning members see more than a single increase. The median year-end 2026 projection moved from 3.4% to 3.8%, a forty basis point upgrade that makes at least one hike the base case rather than a tail.

Run that against the archive. Since the projections were first published in their current form in 2012, there is no comparable single-meeting shift from a cutting bias to a hiking bias. The closest prior episode in the other direction was the December 2018 capitulation, when the median fell from three projected hikes to two over one meeting, a three-dot move. The June 2026 swing moved roughly twelve participants out of the cut column and into hold or hike. The magnitude is not a rounding difference. It is a different category of event.

The mechanical trigger is real and I will not pretend otherwise. Core PCE has been reaccelerating, headline inflation sat near 4.2% year-on-year at the end of May, and the labor market refused to loosen into the print.[6] A Committee that cannot project a return to target on the existing path marks up the path. That is orthodox. But orthodoxy does not explain the unanimity. Stephen Miran, who had dissented toward easing at seven consecutive meetings, stopped dissenting and joined the 12-0 vote.[7] When the most reliably dovish voice on the Committee signs a hawkish hold without a fight, the prudent assumption is that the institution has moved its center of gravity, not that one inflation print frightened everyone for a single afternoon.

The Forecast the Fed Will Not Label

The Summary of Economic Projections is where the reaction function becomes a forecast. The Committee raised its 2026 Core PCE projection from 2.7% in March to 3.3% in June, a sixty basis point upgrade in one quarter. Headline PCE went from 2.7% to 3.6%, a ninety basis point upgrade. Real GDP for 2026 was cut to 2.2%.[8] And the projected return to the 2% target, which in March still arrived inside the forecast horizon, was pushed out to 2028. Higher inflation, lower growth, a higher policy rate, and an extra year of above-target prices. The Fed has produced a forecast with every feature of stagflation except the label, and it will not say the word because saying it would break the credibility the institution spends its existence defending.

This is where the regime call diverges sharply from the consensus call. Consensus treats the June SEP as the high-water mark of hawkishness, the worst the forecast will look, with disinflation and easing to follow. The regime read treats the June SEP as the new baseline from which the Committee will react asymmetrically. Under the old reaction function, a soft inflation print would have pulled the Fed back toward cuts because the easing bias was the default. Under the new one, the default is neutrality at best, and the burden of proof has shifted onto anyone arguing for accommodation. The same incoming data now produces a more hawkish policy response than it would have three months ago, because the function that maps data to policy has been rewritten.

Goldman Sachs read it the same way and acted. In early June, after a payrolls report that landed well above estimates, the bank removed its 2026 rate cut calls entirely and pushed its final two cuts of the cycle into June and December 2027.[9] That deferral was published before the FOMC meeting, not in reaction to it. A house that builds its franchise on rate forecasting looked at the same setup and concluded the cutting path was gone for the year. The street’s most cited economics desk has updated. The price has not.

Consensus Hardened in the Wrong Direction

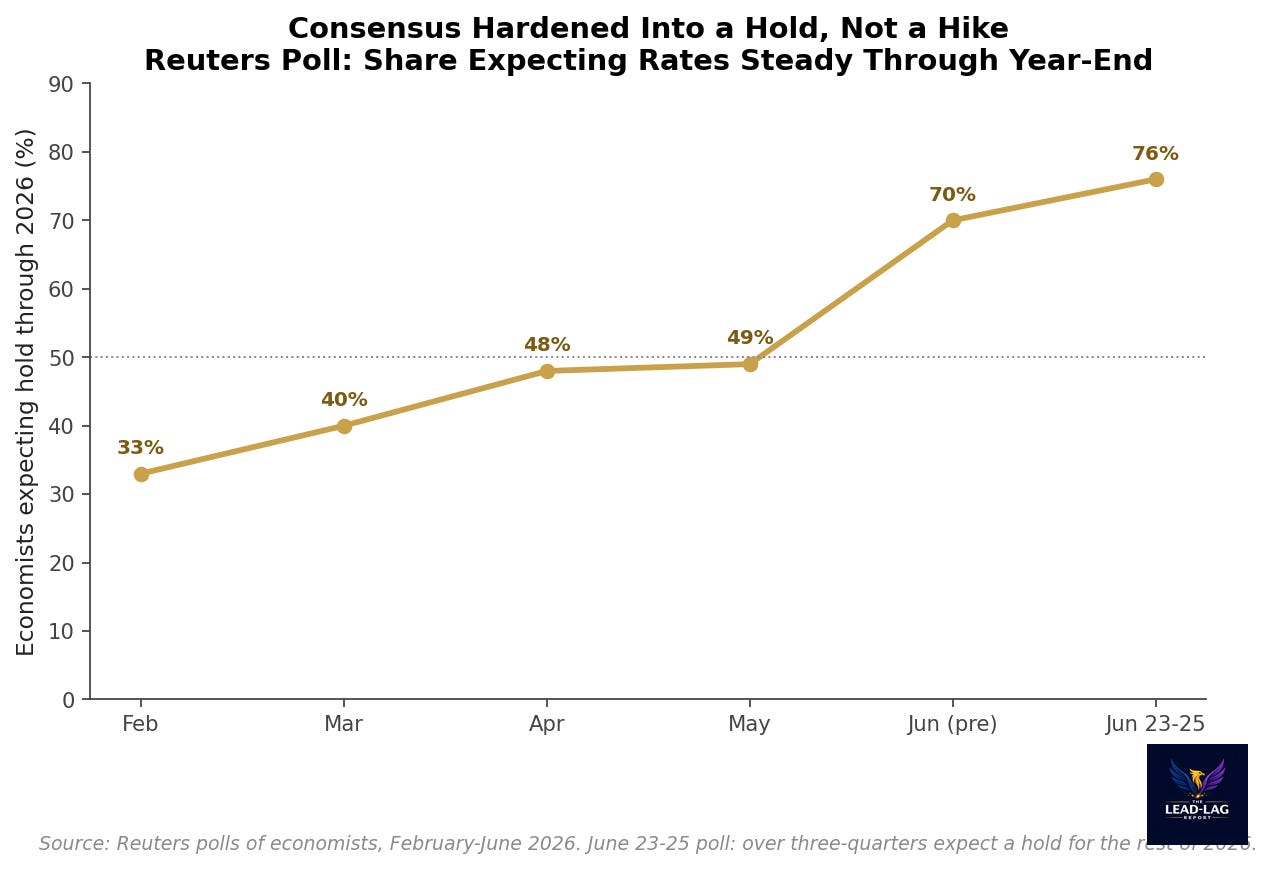

Here is the part that makes this a trade rather than a commentary. Consensus did update after the meeting, but it updated toward a hold, not toward the hikes the Fed itself is now projecting. In the Reuters poll conducted June 23 to 25, more than three-quarters of economists expected the federal funds rate to stay steady for the rest of 2026, up from roughly 70% before the June meeting and just under half a month earlier.[10] The professional forecasting community has converged on the view that Warsh delivered a hawkish hold and will now do nothing. The Fed’s own dots say nine of eighteen participants want to do something, and that something is a hike.

Fed funds futures tell a third story again. Even after the dot plot inverted, the market still implies easing inside a twelve-month window, pricing the year-end hold as a temporary stance that gives way to cuts once the oil-driven inflation impulse fades.[11]Stack the three together. The Fed projects hikes. Economists project a flat hold. Futures still lean toward cuts on a one-year horizon. Three reaction functions cannot all be right. The cheapest assumption an investor can make is that the institution setting the rate understands its own intentions better than the desks forecasting it, and that the gap between the dots and the curve closes by the curve moving, not the dots.

This gap is durable rather than self-correcting because the consensus model has no recent template for a Fed that hikes from already-restrictive policy into a slowing economy. Every reflex built since 2009 assumes the Fed’s instinct is to support markets, that holds are way stations to cuts, and that hawkishness is a phase to be endured. Those reflexes are calibrated to the old reaction function. They will misprice the new one for as long as it holds, which is precisely why the disconnect can persist long enough to matter.

The Tape That Proved the Point

A regime call is only worth the paper it sits on if it survives the disappearance of its catalyst. The obvious objection to everything above is that the hawkishness is just oil. The Iran conflict drove crude toward triple digits, that pushed the inflation forecast higher, and once a peace framework brings the oil premium back down, the hawkish posture should melt with it. June 26 was the test of that objection, and the test came back the wrong way for the consensus.

On June 26 the inflationary trigger cracked. Oil sold off hard on the U.S.-Iran de-escalation tape and energy was the worst-performing equity sector of the day at -5.86%.[12] Under the it-is-just-oil thesis, that is the moment the hawkish regime should have unwound. Instead the regime-confirming signature printed. Credit began to diverge rather than rally in sympathy with the risk-on move in equities. Emerging markets ran +1.81 standard deviations. The Russell 2000 rose +2.03%. And the lumber-to-gold ratio, my preferred forward read on the balance between real growth and monetary debasement, jumped +8.11%.[13] The catalyst for the inflation scare collapsed, and the cross-market read on a higher-for-longer, asymmetrically hawkish Fed held anyway.

That dispersion separates a regime from a reaction. A reaction to oil would have reversed when oil reversed. A regime persists because it is structural. Credit diverging from equities on a risk-on day is the bond market saying the cost of capital is not coming down on the old schedule. Lumber over gold rising while the headline inflation input falls is the real economy repricing the policy stance directly rather than the commodity that supposedly drove it. June 26 told you the Warsh Fed is the variable, and oil was only ever the occasion.

The Analog That Should Make You Uncomfortable

The closest historical parallel is not 2018 and not 2022. It is Volcker’s 1979 doctrinal reset. When Paul Volcker took the chair in August 1979, he did not merely tighten policy. He changed the operating framework and, with it, the market’s understanding of what the Federal Reserve was for. The shift from a cutting posture to a committed tightening posture happened faster than the market could absorb, and it took something on the order of six to nine months for investors to fully price that the rules had changed rather than the cycle having merely turned. The doubters spent those months betting on a reversal that did not come.

I am not arguing the magnitudes line up, because they do not. Volcker was fighting double-digit inflation with a policy rate that would climb above 11% and eventually far higher. Warsh is operating from a 3.50% to 3.75% range against inflation in the low single digits.[14] The scale is an order of magnitude apart and nothing here forecasts a 1980-style rate path. What rhymes is institutional posture, not arithmetic. A new chair arrives with a defined view of what the central bank has been doing wrong, imposes a new reaction function against a market that expects continuity, removes the communication crutches his predecessor relied on, and accepts a period of being misunderstood as the cost of re-establishing that the Fed’s default is not to ease. The 1979 lesson is not about the level of rates. It is about how long a market will keep betting against a chair who has decided to be someone it has not met yet.

The portfolio implication of that analog is about duration and about the cost of capital, not about any single position. When the market finally accepts that the discount rate is not going to fall on the old schedule, the assets that repriced hardest in prior regime shifts were the longest-duration claims, the ones whose value depends most on cash flows far in the future and on a friendly central bank to discount them. That exposure is the one carrying a risk it did not carry at the start of the year, and it is carrying it precisely because consensus still believes the friendly central bank is coming back.

The Steelman

Let me give the soft-landing argument its fairest version, because it is the consensus for reasons that are not foolish. The hawkish surprise was disproportionately driven by oil and tariffs, both of which the Committee itself identifies as supply-side shocks with a known mechanical drag on year-on-year inflation comparisons. If the Iran de-escalation holds and crude stays near the levels it fell to in late June, the energy contribution to inflation rolls off through the third quarter and the data mean-reverts toward the Fed’s longer-run path on its own. Bloomberg Economics has argued exactly this, expecting inflation to approach target by next spring and reading the hike-leaning dots as low-conviction, with Warsh himself acknowledging that the hawkish members lacked much conviction and that a cut was barely discussed.[15] Under that read, the June SEP is the peak of the hawkishness, not the baseline, and the futures market is correctly looking through a transient spike to the easing on the other side.

That is the steelman, and it is not crazy. If the supply shocks roll off cleanly it will be the right call. The regime thesis requires inflation to stay sticky enough that the new reaction function actually gets tested, requires the hawkish lean to prove conviction rather than posture, and requires Warsh to mean what his statement edits imply. None of those are guaranteed. A doctrine that is never forced to act looks the same on the tape as a bluff.

What Would Prove Me Wrong

So here is the falsification condition I am willing to commit to in writing. If Core PCE prints below 3.0% year-on-year for two consecutive months by the September Summary of Economic Projections, and any FOMC voter publicly endorses a cut over that window, the regime call is wrong. That combination would mean the hawkishness was a reaction to a supply shock that faded, the easing bias was dormant rather than dead, and Warsh’s framework rhetoric was cover for a Committee that quietly intends to ease the moment the data permits. I would write that piece. I do not expect to write it, because the statement edits, the unanimity, and the twelve-vote swing read as structure rather than reflex. But the bar is explicit, it is near-term, and it is falsifiable. A thesis that cannot be killed is not a thesis.

Until that bar is cleared, the asymmetry runs one direction. If consensus is right and this was a hawkish pause that reverts to cuts, portfolios positioned for the old reaction function are fine and nothing needs to change. If the regime read is right, the same portfolios are positioned for a Fed that no longer exists, carrying duration and cost-of-capital risk against a central bank that has restored its right to hike and removed the language that used to promise relief. When one outcome costs nothing and the other costs a repricing, the disconnect itself is the opportunity, and right now the disconnect is wide because three different reaction functions are trading against each other and only one of them sets the rate.

The Fed has done the work for anyone willing to read it instead of pattern-matching to the last decade. It deleted the easing bias. It moved twelve votes. It pushed the return to target out a year. It changed the chair and the chair changed the machine. And it held that posture even when the oil shock that supposedly explained all of it cracked on June 26. Consensus heard a hold and a calming voice and went back to waiting for the cut. The institution is no longer the one consensus is waiting for.

Warsh did not pause. He pivoted. The market is still waiting for him to pause.

Few understand this.

— — —

Notes

[1] Board of Governors of the Federal Reserve System, FOMC statement, June 17, 2026. Unanimous 12-0 hold at the 3.50%-3.75% target range, Chair Kevin Warsh’s first meeting. https://www.federalreserve.gov/newsevents/pressreleases/monetary20260617a.htm

[2] Transcript of Chair Warsh’s Press Conference, June 17, 2026, Board of Governors of the Federal Reserve System. Statement pared down and easing-bias / forward-guidance language removed; commitment to price stability retained. https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20260617.pdf

[3] Federal Reserve, June 17, 2026 press conference and projection materials. Chair Warsh declined to submit a dot, citing skepticism of forward guidance, and announced reviews of communications, balance sheet, data sources, productivity, and the inflation framework. https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20260617.htm

[4] Federal Reserve, Summary of Economic Projections, March 18, 2026. March distribution: twelve of eighteen participants expected at least one cut by year-end 2026, none expected a hike. https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20260318.pdf

[5] Federal Reserve, Summary of Economic Projections, June 17, 2026. June distribution of 18 dots: nine expect at least one hike, eight a hold, one a cut; median year-end 2026 fed funds projection 3.8%, up from 3.4% in March. https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20260617.htm

[6] Reuters and U.S. News & World Report coverage, June 17, 2026: headline inflation near 4.2% year-on-year at end of May; labor market firm into the meeting; six of nine hike-leaning members saw more than one increase. https://money.usnews.com/investing/news/articles/2026-06-17/nearly-half-of-fed-policymakers-see-a-2026-rate-hike-in-the-cards

[7] Yahoo Finance, New Era for the Fed: Kevin Warsh at the FOMC, June 17, 2026. Governor Stephen Miran did not advocate a rate cut for the first time in his seven-meeting tenure; the decision was 12-0. https://finance.yahoo.com/economy/policy/articles/era-fed-kevin-warsh-fomc-205600350.html

[8] Federal Reserve, Summary of Economic Projections, June 17, 2026. 2026 year-end Core PCE revised to 3.3% (from 2.7% in March); headline PCE to 3.6% (from 2.7%); real GDP to 2.2%; return to the 2% target pushed to 2028. https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20260617.htm

[9] Goldman Sachs Research, Why the Fed Is Unlikely to Cut Rates This Year, June 2026; reporting via Bloomberg and Reuters, June 6-8, 2026. Goldman removed its 2026 cut calls and moved the final two cuts of the cycle to June and December 2027. https://www.goldmansachs.com/insights/articles/why-the-fed-is-unlikely-to-cut-rates-this-year

[10] Reuters poll of economists, conducted June 23-25, 2026. Over three-quarters expect the federal funds rate to hold for the rest of 2026, up from roughly 70% before the June meeting and just under half a month earlier, defying market pricing for hikes. https://www.marketscreener.com/news/fed-to-hold-rates-this-year-economists-say-defying-market-bets-for-hikes-ce7f5fd9dd88f021

[11] CME FedWatch fed funds futures, late June 2026; Raison.app weekly economic update, June 15-21, 2026. Market pricing continued to imply easing within a twelve-month horizon despite the inverted dot plot. https://raison.app/news/analytics/june-15-21-2026-weekly-economic-update

[12] Morningstar and Reuters coverage of the U.S.-Iran de-escalation tape, June 2026: oil fell roughly 5% and energy equities led declines as the geopolitical risk premium unwound. https://global.morningstar.com/en-nd/markets/oil-prices-fall-us-iran-peace-deal-signals-possible-end-energy-crisis

[13] Lead-Lag Report intermarket dashboard, session close June 26, 2026: XLE -5.86% (worst sector), EEM +1.81 standard deviations, Russell 2000 +2.03%, lumber-to-gold +8.11%, with high-yield credit diverging from the equity risk-on move. Lumber-to-gold ratio used as a forward proxy for the real-growth versus debasement balance.

[14] Federal Reserve historical data via FRED, St. Louis Fed. Effective federal funds rate exceeded 11% during the Volcker tightening that began in 1979; the June 2026 target range is 3.50%-3.75%. https://fred.stlouisfed.org/series/FEDFUNDS

[15] CRE Finance Council market commentary, June 23, 2026, summarizing Chair Warsh’s June 17 remarks and Bloomberg Economics’ view that hike-leaning members lacked conviction, a cut was barely discussed, and inflation may approach target by next spring. https://www.crefc.org/cre/content/News/Items/Research_and_Data/2026/Economy_the_Fed_and_Rates_6_23_26.aspx

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.