The Yen at a 52-Week Low and the Setup for a Carry Recompression (JOJO)

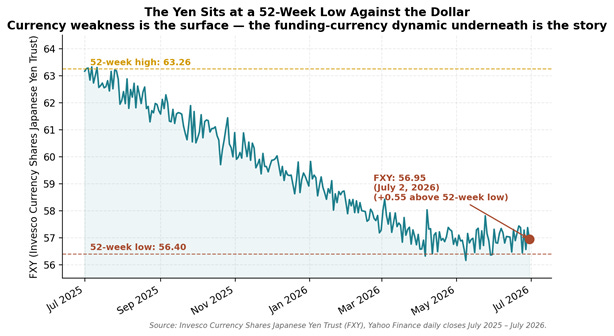

FXY closed at 56.95 on July 2 — just 55 cents above its 52-week low of 56.40. The VIX has collapsed. Credit is complacent. The three ingredients of a reverse-carry episode are on the table.

KEY HIGHLIGHTS

· The Invesco Currency Shares Japanese Yen Trust (FXY, a grantor trust that holds Japanese yen and issues shares designed to track the price of the yen relative to the U.S. dollar, net of expenses) closed at 56.95 on July 2, 2026 — just 55 cents above its 52-week low of 56.40 and firmly at the low end of its 52-week range (56.40 – 63.26).[1]

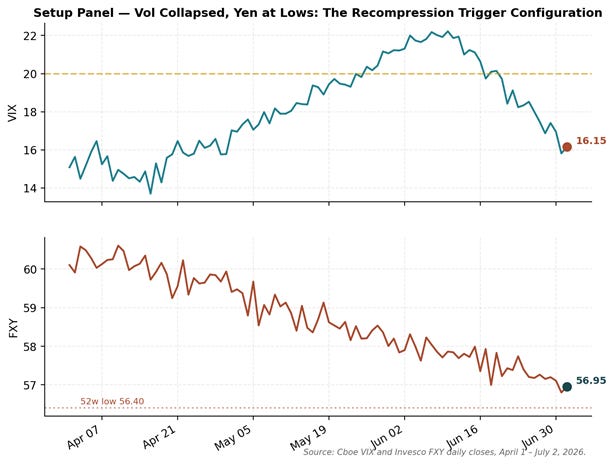

· The VIX collapsed to 16.15 on July 2 — a 27% decline from its June 10 peak of 22.22 and well below its long-run average of 20. Equity vol pricing tranquility is one of the two conditions of a classic carry recompression setup.[2]

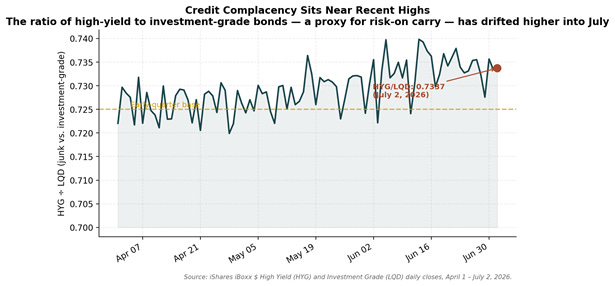

· ICE BofA US High-Yield credit spreads remain historically tight and the HYG/LQD ratio sits near recent highs — meaning that the market is compensating investors very little for the volatility risk that a yen re-strengthening move has historically brought with it.[3]

· This is precisely the setup the ATAC Credit Rotation ETF (Ticker: JOJO) was built to navigate — a bond ETF that rotates between high-yield credit and long-duration Treasuries based on a rules-based equity-defense signal, designed to move before the carry-trade unwind reprices credit rather than after.[4]

· In my view the more honest read of this three-way configuration — yen at multi-decade weakness, equity vol at multi-month lows, credit complacent — is that the setup for a reverse-carry episode is in place. The catalyst is unknown. The setup is not.

I’ve found that the moments in markets that most deserve attention are not the ones where every asset class is confirming the same story. They are the ones where the currency market, the equity vol market, and the credit market are pricing three different worlds. Right now, the yen is pricing extreme funding-currency weakness, equity vol is pricing tranquility, and credit is pricing perfection. In my experience, those three prices do not stay reconciled forever — and the historical resolution has usually been quick. That resolution risk is why the ATAC Credit Rotation ETF (JOJO) exists.

THE MACRO BACKDROP: A CURRENCY AT MULTI-DECADE LOWS

The most durable funding-currency story of the past several years — the persistent weakness of the Japanese yen against the US dollar — is now sitting at a fresh multi-year extreme. FXY closed at 56.95 on July 2, 2026, just 55 cents above its 52-week low of 56.40, and at the very bottom end of its 52-week range of 56.40 to 63.26.[1] In dollar terms, the yen has depreciated to a level that has historically compressed the differential between Japanese and US funding costs to the point where the carry trade — borrow in yen, invest in higher-yielding assets abroad — has stopped being a curiosity and become a structural feature of global capital flows.

Source: Invesco Currency Shares Japanese Yen Trust (FXY), Yahoo Finance daily closes July 2025 – July 2, 2026.

The setup that has historically preceded sharp reversals in this trade is not currency weakness on its own — it is currency weakness paired with two other conditions: equity volatility sitting low enough that vol-scaled portfolios are running larger notional exposures than they otherwise would, and credit spreads tight enough that the risk of a rapid vol repricing is being under-compensated. Right now, both of those conditions are on the table. This is the three-way configuration — currency, vol, credit — that JOJO is designed to respect through a rules-based rotation between credit and duration.

THE VOLATILITY SIDE: A FEAR GAUGE THAT HAS FULLY RESET

The Cboe Volatility Index touched 22.22 on June 10, 2026 and has since collapsed to 16.15 on July 2 — a decline of roughly 27% and a level well below the long-run average of 20.[2] The equity vol surface has, by every conventional read, finished its post-June reset.

A low VIX regime is not, in itself, a problem. The problem is that vol-scaled strategies — risk-parity, target-volatility, and increasingly a large share of systematic macro — mechanically scale up exposure when realized and implied vol both fall. That scaling is the mechanism by which carry trades quietly become larger, more crowded, and more sensitive to a shock that has not yet arrived.

In August 2024, when the yen re-strengthened sharply and the carry trade unwound over a matter of days, the trigger was not a fundamental repricing of Japan’s interest rate outlook. The trigger was a small shift in policy expectations that ran into a positioning setup that had grown while the vol surface was calm. That episode is worth studying not because I think it will replay identically — it will not — but because the setup that preceded it is, in outline, the setup we are looking at now. Portfolios structurally committed to high-yield credit through that kind of episode paid a price. JOJO is built so that a rules-based investor does not have to.

THE CREDIT SIDE: COMPLACENCY SITS NEAR RECENT HIGHS

The third dimension of the reverse-carry setup is the credit market — specifically, how much compensation credit investors are demanding for the volatility risk that a currency-driven vol episode brings with it. The answer, right now, is very little.

Source: iShares iBoxx $ High Yield (HYG) and Investment Grade (LQD) daily closes, April 1 – July 2, 2026. The ratio has drifted higher into July — a risk-on carry signature.

The HYG/LQD ratio — the price of high-yield bonds relative to investment-grade — has drifted higher into July. That is the signature of a market in which the marginal buyer of credit is unwilling to pay a meaningful premium for the safer tier. Combined with the yen at multi-year lows and equity vol at multi-month lows, the message is that all three asset classes have decided the current regime is durable.

Historically, that has been the moment where the setup is best. The three assets — currency, equity vol, credit — do not all price a benign regime for very long once one of them starts to move. The historical asymmetry has been that credit re-prices to vol faster than the reverse, and vol re-prices to currency dislocation faster than the reverse. In other words, the yen is the leading edge, credit is the trailing edge, and both are, right now, priced for continuity.

THE SETUP CONFIGURATION

The visual below is the setup — not a forecast, not a call, but a mapping of where the three assets sit today.

Source: Cboe VIX and Invesco FXY daily closes, April 1 – July 2, 2026. The two-panel setup: equity vol collapsed to 16.15 and the yen at 56.95, just above its 52-week low.

The catalyst for a reverse-carry episode is not something a portfolio manager can predict with confidence. What can be identified with confidence is whether the setup is in place — and by the two most reliable historical markers, it is. That is the question JOJO is designed to answer: not what triggers the unwind, but whether the equity-defense signal has begun to say hold the safer tier.

WHAT THIS MEANS FOR A RULES-BASED CREDIT ROTATION APPROACH (JOJO)

This is the kind of configuration that highlights why the ATAC Credit Rotation ETF (Ticker: JOJO), which I brought to market and manage as portfolio manager, exists in the form it does.

JOJO is a bond ETF that either holds high-yield credit exposure or long-duration Treasury exposure, based on the behavior of the Utilities sector relative to the broader S&P 500. The intuition is not complicated: when Utilities outperform the broader equity market, equity investors are quietly shifting toward defense — and historically, equity defense has led credit defense by enough time that a rules-based investor can act on the signal without trying to forecast the currency catalyst, the vol catalyst, or the credit trigger.

The mechanics are not the pitch. The mechanics are that JOJO will hold credit when the equity-defense signal says hold credit, and will hold long-duration Treasuries when the signal says move. The fund is not designed to outsmart every short-term move in the yen, the VIX, or high-yield spreads. It is designed to not be structurally committed to credit risk through a regime change — specifically the kind of regime change that historically follows a three-way divergence between currency, vol, and credit.

The 30-day SEC yield for JOJO is disclosed on the fund’s prospectus page at atacfunds.com/jojo, and I would encourage anyone considering the fund to review it there alongside the full statutory prospectus.[4]

THE BOTTOM LINE

Right now we have:

— the Japanese yen ETF (FXY) at 56.95, just 55 cents above its 52-week low,[1]

— the VIX collapsed to 16.15, a −27% round-trip from June 10,[2]

— the HYG/LQD ratio at recent highs, signaling credit complacency,[3] and

— an equity vol surface that has fully reset just as the currency and credit sides of the carry trade are pricing continuity.

That combination does not guarantee a reverse-carry episode is imminent. But it does describe a setup where three of the most reliable historical markers of one are simultaneously in place. In my view, the more honest read of this configuration is not that the market has resolved the risk, but that the market has agreed to price it at zero — and pricing at zero is what precedes the historical re-pricings, not what follows them. JOJO is the vehicle I built to respect that asymmetry rather than argue with it.

ENDNOTES

[1] Invesco Currency Shares Japanese Yen Trust (FXY), Yahoo Finance daily closes, accessed July 5, 2026.

[2] Cboe Global Markets. “VIX Index Historical Data.” Cboe Global Markets, Inc., 2026. Accessed 5 July 2026.

[3] iShares iBoxx $ High Yield Corporate Bond ETF (HYG) and iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), Yahoo Finance daily closes, accessed July 5, 2026.

[4] ATAC Credit Rotation ETF (JOJO). Statutory Prospectus and 30-day SEC Yield Disclosure. Tidal Trust II, 2026. Accessed 5 July 2026.

DISCLOSURES (JOJO)

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the “fear gauge” of Wall Street, is a real-time market index that measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

JOJO is distributed by Foreside Fund Services, LLC.

Learn more about $JOJO at https://atacfunds.com/jojo/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.