This 10% Yielder Gives You Equity Upside With A Bond Floor

But The Premium And Leverage Deserve A Harder Look

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Markets are in a peculiar spot right now. The Fed is expected to continue cutting rates into the back half of 2026, yet geopolitical flare-ups have pushed the VIX back toward 25 and rattled equity markets. Credit spreads, while still tight by historical standards at roughly 312 basis points for high yield, have started to widen. Meanwhile, convertible bond issuance hit a record $166 billion in 2025 and shows no signs of slowing. That matters because convertibles sit at a unique intersection — they offer bondholders equity upside through conversion optionality while providing a fixed-income floor when equities sell off.

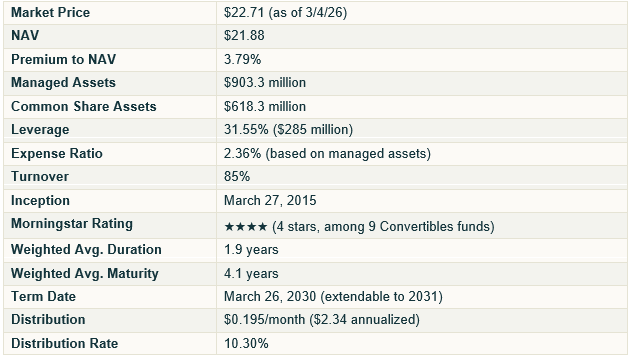

It’s that asymmetric profile that makes the Calamos Dynamic Convertible and Income Fund (CCD) particularly interesting right now. CCD is a closed-end fund managed by the convertible bond specialists at Calamos Investments, yielding approximately 10.3% through monthly distributions of $0.195 per share. With nearly $903 million in managed assets and a portfolio that’s 85% invested in convertible securities, CCD offers one of the purest high-yield convertible plays available in the CEF market.

Fund Background

CCD’s investment objective is to provide total return through a combination of capital appreciation and current income. The fund invests primarily in convertible securities and high-yield fixed-income, with the flexibility to sell options for additional income. At least 50% of the portfolio must be in convertibles, and at least 80% in convertible and income-producing securities combined.

What distinguishes CCD from many income-focused CEFs is its hybrid nature. Convertible bonds give the portfolio equity-like participation in rising markets while the bond component provides coupon income and downside protection. Calamos actively allocates across convertibles, corporate bonds, bank loans, and equities to optimize risk-reward over full market cycles.

Key Fund Facts

The term-limit structure is worth highlighting. CCD is scheduled to terminate on its 15th anniversary in March 2030, keeping the market price anchored closer to NAV than a perpetual CEF — which is why it trades at only a modest premium rather than the deep discounts common in the closed-end fund space.

Portfolio Composition

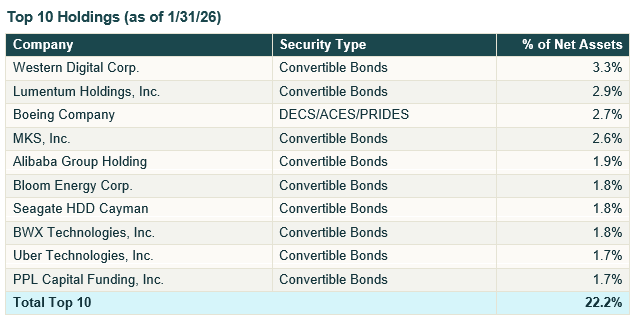

CCD’s portfolio as of January 31, 2026 is overwhelmingly positioned in convertible bonds at 85.2%, followed by corporate bonds (9.2%), cash (2.7%), bank loans (1.6%), and common stock (1.1%).

Nearly 75% of the portfolio is in unrated securities — typical for convertible bonds, since most convertible issuers are mid-cap and small-cap growth companies that don’t seek traditional credit ratings. Of the rated portion, about 12.7% is investment-grade and 12.4% is high-yield. The weighted average duration of just 1.9 years means interest rate sensitivity is remarkably low.

Sector-wise, CCD is heavily tilted toward technology at 36.7%, followed by Industrials (14.9%), Health Care (9.0%), Financials (8.4%), and Consumer Discretionary (7.8%). Geographic exposure is 91.3% U.S.

This is essentially a diversified bet on the equity upside of several hundred mid-cap growth companies — through convertible bonds that pay coupons and mature at par.

Historical Performance

CCD has delivered annualized total returns of 9.47% on market price and 9.70% on NAV since its March 2015 inception. The calendar year returns tell a more dramatic story — CCD’s NAV returned 59.93% in 2020, 28.89% in 2019, and 21.73% in 2025. The 2022 drawdown was painful at -28.54% on NAV, roughly in line with what you’d expect from a leveraged convertible portfolio in the worst bond market in decades.

The divergence between market price and NAV returns is notable. In 2025, CCD’s NAV returned +21.73% but the market price returned -3.99% — driven by premium compression. In 2024, the reverse: NAV returned just 7.89% but market price surged 36.82% as the premium expanded. Over time, total return on market price and NAV converge, but in any given year, discount/premium dynamics can dominate the return experience.

Volatility Comparison

Given its leverage and equity-linked holdings, CCD exhibits higher volatility than a traditional high-yield bond fund. The 2022 drawdown illustrates this — convertible exposure amplified the sell-off in both rates and equities. However, the short duration (1.9 years) provides genuine insulation against pure interest rate risk, which is why CCD recovered faster than many longer-duration bond funds.

Discount/Premium to NAV

CCD currently trades at a 3.79% premium to NAV. Historically, this fund has oscillated between meaningful discounts (exceeding -15% during the COVID crash) and double-digit premiums (late 2024). A 3.8% premium isn’t outrageous for a 10%+ yielder, but it does mean you’re paying above intrinsic value. With the March 2030 term date approaching, the premium may remain contained.

Macro Environment

The macro backdrop for CCD is a mixed bag — and honestly, that’s exactly when convertibles tend to shine. The convertible bond market entered 2026 with strong momentum after record 2025 issuance. Calamos’s own research team has noted that convertibles are well-positioned for a broadening of equity leadership beyond mega-caps, given the asset class’s heavy weighting toward small- and mid-cap issuers.

On the bullish side, the Fed is expected to bring rates closer to 3% over 2026. Lower rates reduce CCD’s borrowing costs on its $285 million in leverage and support convertible valuations. AI infrastructure buildout continues driving issuance from data center and technology companies well-represented in CCD’s portfolio.

On the bearish side, credit spreads have started widening. J.P. Morgan forecasts U.S. high-grade spreads reaching 110 basis points by year-end. Geopolitical risk has injected volatility into equity and credit markets simultaneously. For a leveraged convertible fund, that’s a double-edged sword — the equity optionality benefits from volatility in theory, but leveraged drawdowns can be severe in practice.