Too Calm for Comfort: Why Tight Spreads and Hot Markets Complicate the Fed’s Next Move

At first glance, pushing higher interest rates sounds counterintuitive. Investors and pundits today expect the Fed to continue to cut rates as the economy softens. Yet history shows that complacency can be dangerous. Consider credit spreads – the extra yield that corporate borrowers pay over safe Treasuries. Right now, those spreads are exceptionally tight, near historic lows.¹ That means investors aren’t demanding much extra return to hold corporate debt, a sign of optimism – or perhaps of dangerous complacency. Some analysts warn that when lenders refuse to charge a risk premium, they may be ignoring the possibility of trouble ahead.¹ In other words, we may have plenty of liquidity chasing assets, and that can fuel bubbles. In this climate, it isn’t obvious that monetary policy is too tight. Even the Federal Reserve’s own officials are sounding cautionary notes. For example, St. Louis Fed President Bullard recently pointed out that U.S. inflation is closer to 3% than to the Fed’s 2% goal and that monetary policy is already “close to neutral.” He advised the Fed to “tread with caution” on further rate cuts.²

The point is stark: if markets are acting as if money is abundant, it’s worth asking whether the Fed should let up at all. Some Fed governors have argued that with inflation still elevated, cutting rates now could backfire. In fact, Kansas City Fed President Esther George once dissented against a proposed rate cut, explicitly noting that ongoing inflation made it unwise.³ And Fed Chair Powell himself has signaled that recent rate cuts may be the end of the cycle, given rising inflation pressures through 2025.⁴⁵ All this suggests that the era of easy money may not be over – at least, not yet.

Market Complacency and Tight Credit

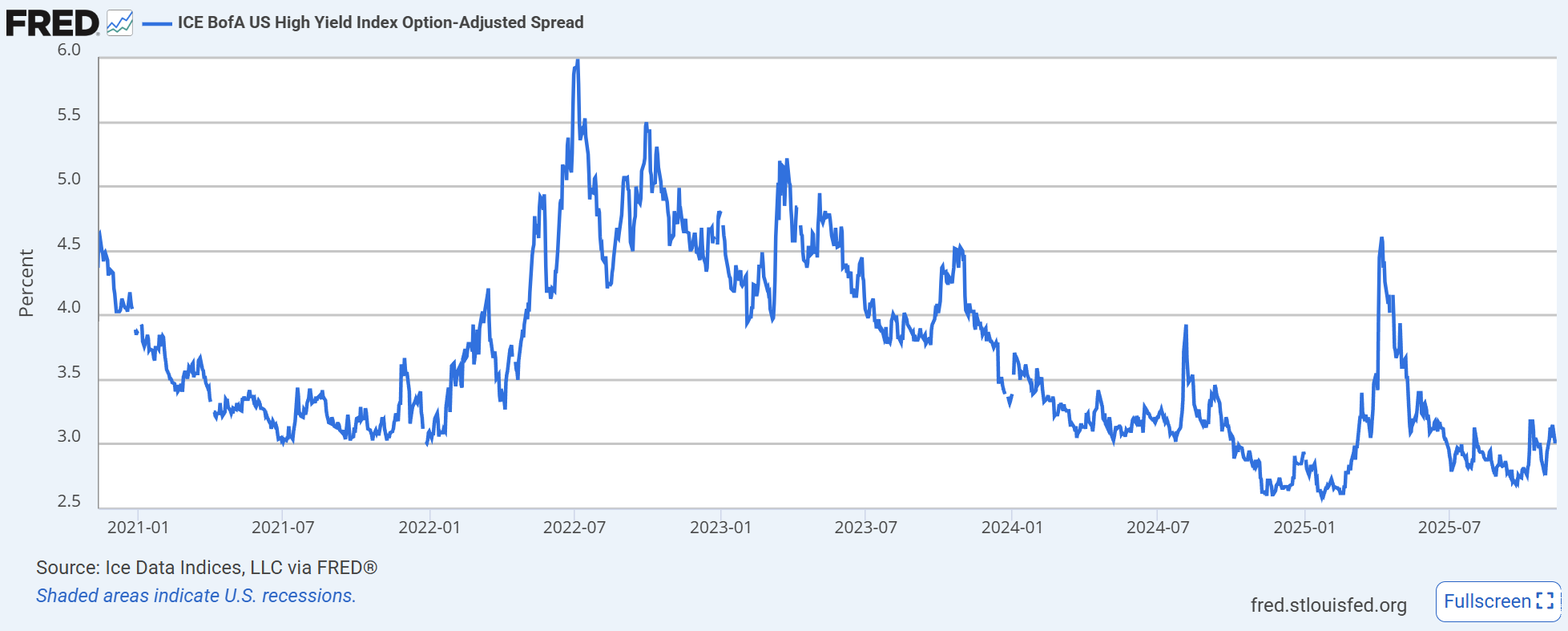

If Fed policy feels loose, the credit markets agree. Corporate debt is easier and cheaper to borrow than at almost any time in recent memory. Investment-grade bonds yield very little more than Treasuries today.¹ Even speculative-grade (“junk”) spreads are hovering near record lows. This tells us that investors broadly feel good about the economy. But that cheerfulness can be a warning sign. When spreads are vanishingly small, it often means investors are underestimating risk. A whiff of trouble – a sudden slowdown, a big debt default, or global shock – can quickly reverse those trends. Right now, the data on credit suggest an overheat, not a downturn. In plain terms, excess credit appetite is flooding the system with liquidity.

Why might that argue for higher rates? Because loose financial conditions themselves can reignite inflation. Historically, one aim of higher rates is to cool off excess risk-taking. By making borrowing costlier, the Fed can add a modest brake to an economy running on borrowed money. In today’s bond market, the lack of a risk cushion is the odd sign, not the norm. It’s worth noting that when spreads were similarly low before, trouble often followed (think 2007–08 or late 2019). For an everyday investor, the lesson is that complacency in the markets can be a hidden danger – and that a Fed move to tighten even further might simply be the prudent thing to do.