The release of last week’s non-farm payroll report brings with it two big concerns. First is the macro implication that it’s signaling a potentially rapidly slowing labor market. Second is Trump’s targeting of the BLS by firing its commissioner. Regarding the former point, this is a trend we’ve been seeing in data elsewhere. Continuing jobless claims have been elevated for weeks. The ADP data, which measures the private sector, showed a jobs contraction in June. The latest hiring data suggests that employers are sitting on the sidelines waiting for more clarity on the tariff front before proceeding. I think there’s little question at this point that we’re seeing a slowdown in the labor market. It probably doesn’t elevate to the level of a full-on stagnation in jobs yet, but it appears to be heading in that direction.

The latter point may be something or it might be paranoia. The market’s impression is that Trump is attempting to control and limit any information that’s unfavorable to him. The official reason may be data integrity concerns, but the bond market has been pricing in a bit more risk over the past few days, both due to the jobs report and its aftermath. The Treasury yield curve steepened slightly, but yields on the short end of the curve dropped significantly, pricing in a higher likelihood of more rate cuts in the near future. U.S. equities reacted for one day on Friday before retracing much of that loss. Within equities, however, there are some shifts. Cyclicals are generally underperforming while utilities have turned into a leader once again. It’s not a broad risk-off move yet, but there are hints that something along those lines is developing.

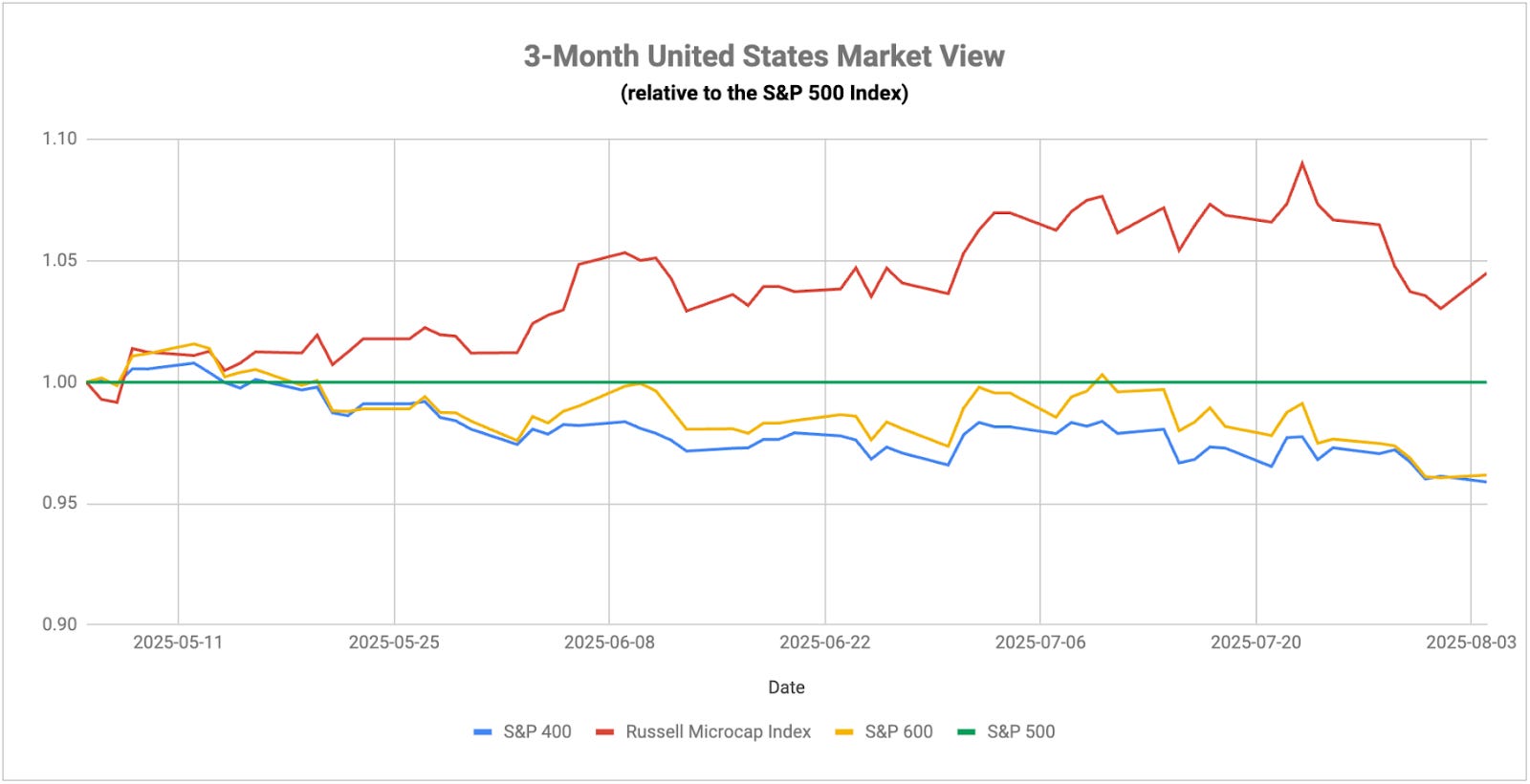

The consumer side is still looking weak as evidenced by the sharp underperformance of discretionary stocks over the past week. Credit card delinquency rates overall are at 12-year highs and rising. According to the St. Louis Fed, nearly ¼ of all credit card debt from the lowest income decile is at least 30 days late. Across the U.S. as a whole, the delinquency rate is almost at the same level as during the peak of the financial crisis. If you look at delinquency rates alongside the Fed Funds rate, you’ll see a very high correlation. In other words, consumers haven’t been able to handle the current high rate regime and are likely to come under more pressure as long as the Fed keeps conditions restrictive. This is no doubt a focus of both economists & the White House because if this trend hits at the same time that the labor market slows down, the situation could turn bad quickly.