UTF: Leveraged Infrastructure at the Crossroads of Grid Expansion and Capital Costs

How the Cohen & Steers Infrastructure Fund’s closed-end structure, leverage profile, and discount dynamics shape outcomes in a rate-sensitive, electricity-driven investment cycle.

Key Highlights

UTF provides global listed infrastructure exposure through a leveraged closed-end fund rather than an ETF structure.

Portfolio construction blends common equity, preferred securities, and other income instruments, increasing sensitivity to rates and credit.

Discount/premium dynamics and periodic corporate actions materially affect investor experience.

Accelerating electricity demand and grid investment create a structural tailwind for utilities.

Financing conditions, real rates, and credit spreads remain decisive for valuation and leverage outcomes.

Infrastructure investing in early 2026 sits at a regime intersection. Electricity demand is accelerating across advanced economies, transmission investment plans are expanding, and essential-service assets enjoy multi-year capital pipelines.¹ At the same time, policy rates remain elevated relative to the prior cycle, and credit markets continue to price leverage as a central variable.²

The Cohen & Steers Infrastructure Fund (UTF) operates squarely within that tension. UTF is not a passive ETF. It is a closed-end fund listed on the New York Stock Exchange, meaning shares trade in the secondary market rather than being created and redeemed at net asset value.³ That structural choice introduces an additional return driver beyond portfolio performance and leverage costs: the fund’s discount or premium relative to NAV.⁴

UTF therefore represents more than infrastructure exposure. It represents infrastructure exposure expressed through leverage, market structure, and capital-market psychology.

Portfolio Architecture and Closed-End Structure

UTF’s investment policy requires that at least 80 percent of managed assets be invested in infrastructure companies, defined broadly to include utilities, pipelines, toll roads, airports, railroads, ports, and communications infrastructure.⁵ The fund may employ borrowings, reverse repurchase agreements, and derivatives such as interest-rate swaps and caps to manage financing exposure.⁵

The most recent factsheet reflects a diversified global portfolio spanning hundreds of positions, with a capital stack that blends common equity and a meaningful allocation to preferred and other income-producing securities.⁶ That hybrid approach matters. Preferred and fixed-income instruments introduce additional duration and credit sensitivity relative to a pure equity infrastructure portfolio.

Sector exposure leans heavily toward electric utilities, supplemented by midstream energy transport, communications towers, and transportation infrastructure.⁶ Representative holdings include NextEra Energy, Inc.; TC Energy Corporation; National Grid plc; Enbridge Inc.; American Tower Corporation; and CSX Corporation.⁶ These companies operate in capital-intensive industries characterized by regulated or contract-backed cash flows.

The closed-end fund structure creates distinct behavioral considerations. Shares may trade at persistent discounts or premiums to NAV, and shareholders cannot redeem at underlying asset value.⁴ Market price therefore reflects supply-demand conditions in addition to portfolio fundamentals.

Corporate actions can amplify that effect. In October 2025, the sponsor announced preliminary results of a transferable rights offering that raised substantial new capital for infrastructure opportunities.⁷ Rights offerings frequently increase short-term supply and may widen discounts regardless of underlying asset performance. That dynamic represents market structure rather than a direct signal on portfolio quality.

Leverage is the second defining feature. The factsheet indicates that leverage represents a material portion of managed assets and that financing sources include both fixed- and variable-rate instruments.⁶ The fund uses swaps to seek to reduce interest-rate risk.⁶ Investors should treat this as explicit macro exposure. UTF’s performance reflects not only infrastructure earnings trends but also financing costs and hedge effectiveness.

Electricity Demand, Capex, and the Cost of Money

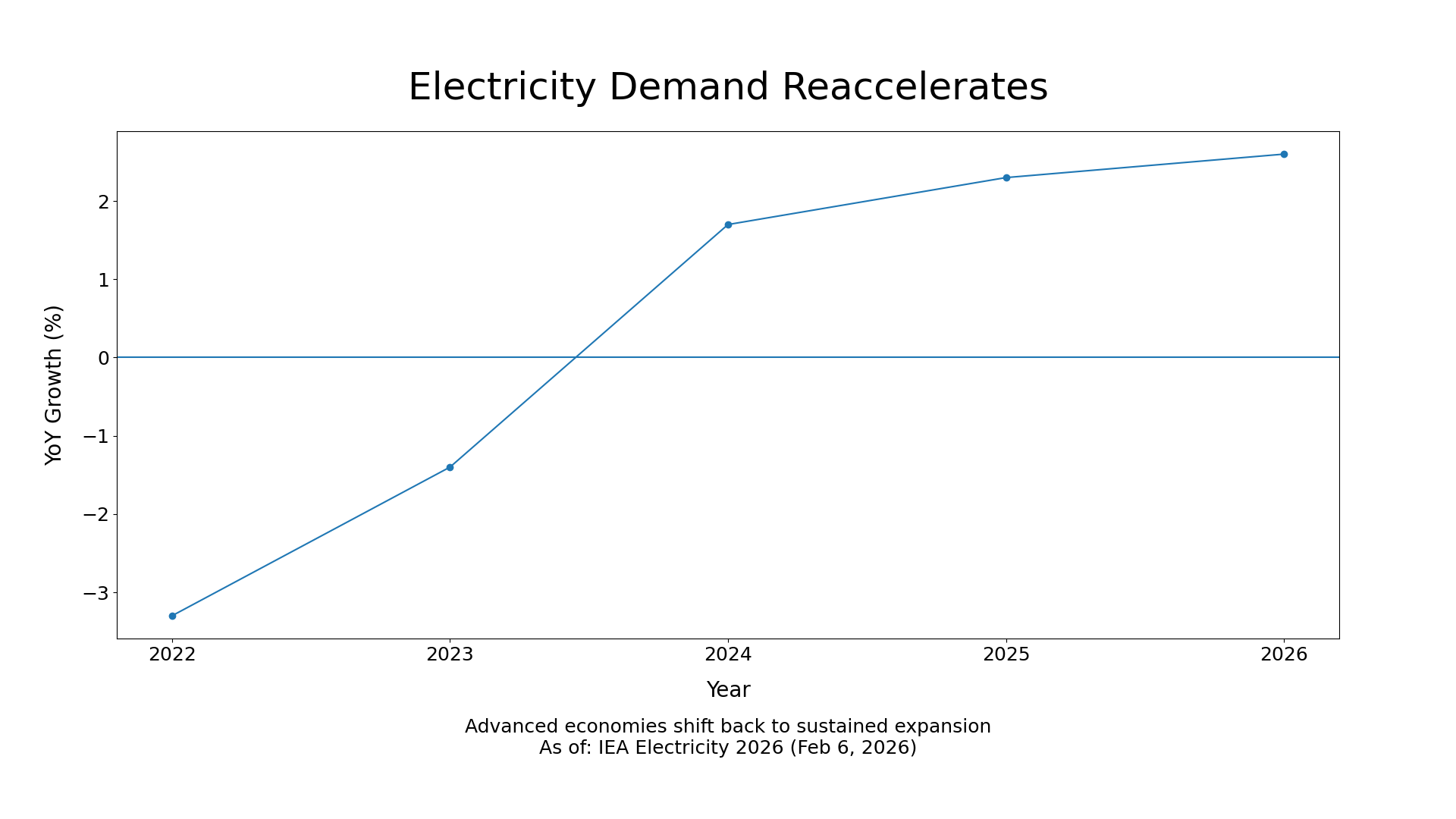

The structural bull case for infrastructure rests on renewed electricity demand growth and substantial planned capital investment. The International Energy Agency’s Electricity 2026 report documents accelerating consumption in advanced economies and highlights grid expansion and flexibility as critical constraints.¹ Utilities expand rate base by building transmission, upgrading networks, and modernizing systems to meet that demand.

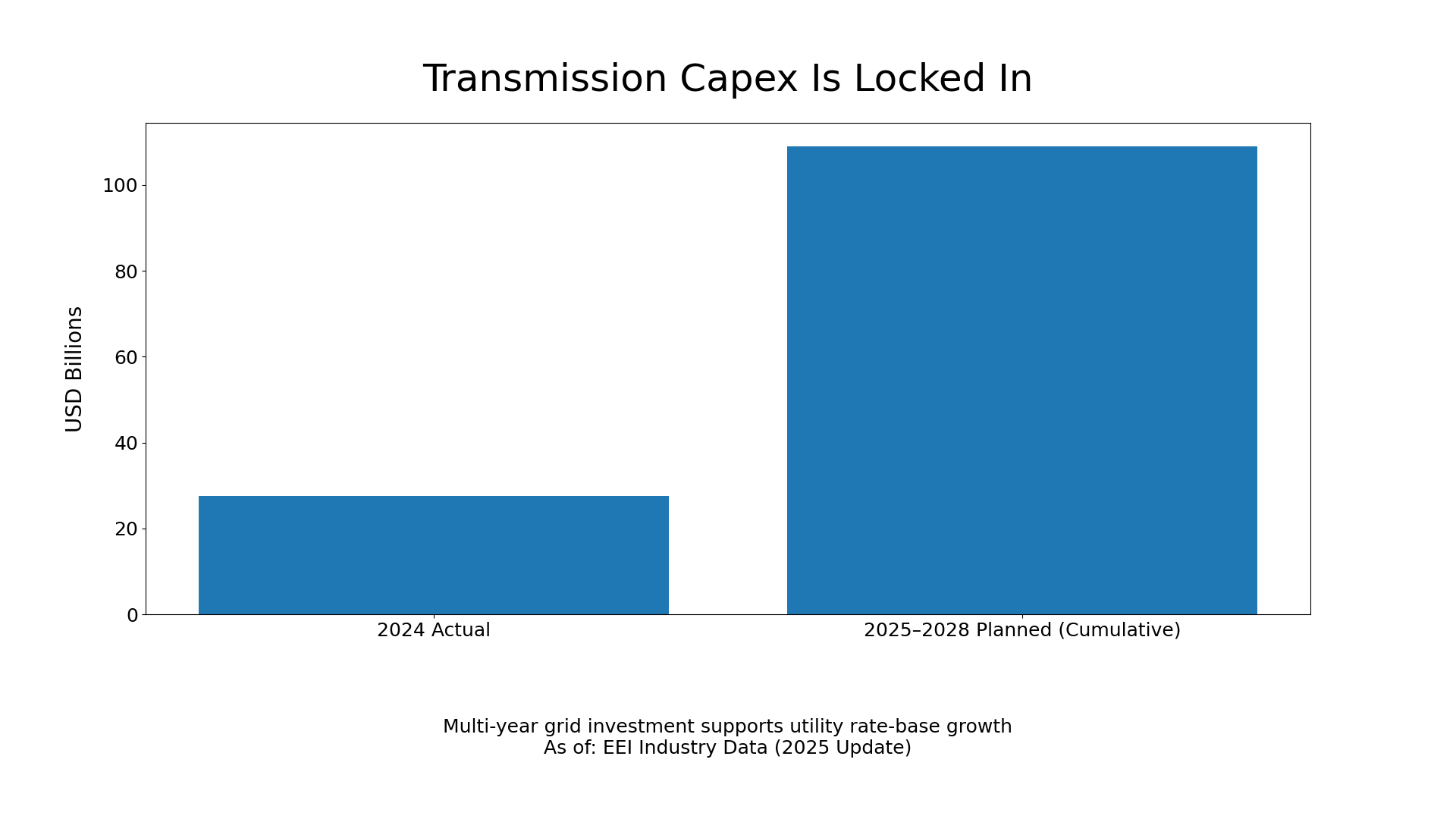

Industry data reinforce the scale of planned spending. Edison Electric Institute reports significant planned transmission construction investment across the 2025–2028 period.⁸ Independent research similarly identifies upward revisions to load forecasts and transmission bottlenecks requiring accelerated buildout.⁹