What Credit Is Saying That Equity Isn't Hearing

The Headline Spread Looks Calm. The Plumbing Underneath It Does Not.

Today’s Lead-Lag Report post is sponsored by TappAlpha

For the first time in three years, U.S. equity breadth is improving. Equal-weight S&P hit fresh all-time highs in mid-June. Russell 2000 followed. The Mag-7 — the names that carried 2023, 2024, and the first half of 2025 — is actually UNDER-performing the broader index YTD.

If you believe that broadening continues, your income sleeve has a problem.

Most popular income ETFs are concentrated in the same mega-cap names that just stopped leading. Covered-call funds written on the S&P or the Nasdaq inherit the index’s concentration. You collect the premium, but you collect it against the part of the market that may be done leading.

TSYX (TSPY Lift ETF) is built differently. The strategy generates income from S&P 500 exposure without doubling down on the top-10 concentration that already defines most income products. For advisors positioning client portfolios for a broadening market — where leadership rotates from mega-cap tech toward the other 490 names — TSYX is the income tool that sits on the right side of that rotation.

Income that doesn’t require betting the rally stays narrow.

Learn more at tappalpha.com.

____________________________________________________________

Disclosures

Investors should carefully consider the Fund’s investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Fund’s prospectus and summary prospectus, which may be obtained by visiting TappAlphaFunds.com or by calling (844) 403-2888. Read the prospectus and summary prospectus carefully before investing.

An investment in the Fund is subject to risks, including the possible loss of the principal amount invested. The Fund and adviser are new, and the ETF has only recently commenced operations. This Fund may not be suitable for all investors.

The Fund seeks leveraged exposure to the performance of its reference asset and does not invest directly in equity securities in the same manner as a traditional equity fund.

Exchange-Traded Funds (ETFs) trade like stocks, are subject to investment risk, and will fluctuate in market value. Transactions in shares of ETFs will result in brokerage commissions, which will reduce returns. There is no assurance that the Fund’s investment process will consistently lead to successful investing. As of the date of this prospectus, the Fund has no operating history and currently has fewer assets than larger funds. Like other new funds, large inflows and outflows may impact the Fund’s market exposure for limited periods of time. This impact may be positive or negative, depending on the direction of market movement during the period affected. TSYX is distributed by Foreside Fund Services, LLC.

Daily Leverage and Compounding Risk. The Fund seeks daily leveraged investment results and resets its exposure on a daily basis. As a result, the Fund’s performance for periods longer than a single trading day will differ from the stated leveraged objective due to the effects of compounding. In volatile markets, compounding may significantly impact returns and may cause the Fund to experience losses even if the reference asset’s performance is positive over the same period. The use of leverage may magnify losses and increase the risk of losing the entire investment.

Leverage Risk. The Fund obtains investment exposure in excess of its net assets by utilizing leverage and may lose more money in market conditions that are adverse to its investment objective than a fund that does not utilize leverage. An investment in the Fund is exposed to the risk that a decline in the daily performance of TSPY will be magnified. This means that an investment in the Fund will be reduced by an amount equal to 1.3% for every 1% daily decline in TSPY, not including the costs of financing leverage and other operating expenses, which would further reduce its value. If TSPY declines by approximately 77% or more in a single trading day, the Fund could experience a total loss of its value for that day. A total loss may occur in a single day even if TSPY does not lose all of its value. Leverage will also have the effect of magnifying any differences in the Fund’s correlation with TSPY and may increase the volatility of the Fund. The cost of maintaining leveraged exposure (e.g., swap financing, collateral, and related fees) may increase, particularly in rising interest rate environments, which can adversely affect performance.

Rebalancing Risk. If for any reason the Fund is unable to rebalance all or a part of its portfolio, or if all or a portion of the portfolio is rebalanced incorrectly, the Fund’s investment exposure may not be consistent with its investment objective. In these instances, the Fund may have investment exposure to TSPY that is significantly greater or significantly less than its stated multiple. The Fund may be more exposed to leverage risk than if it had been properly rebalanced and may not achieve its investment objective, leading to significantly greater losses or reduced gains. Intraday market movements may cause the Fund’s actual exposure to drift from 130% between rebalancing times, which can contribute to tracking differences.

____________________________________________________________

Definitions

Equal-weight S&P (S&P 500 Equal Weight) — A version of the S&P 500 in which all constituents carry the same weight rather than being weighted by market capitalization, so the largest companies do not dominate the index’s performance.

Russell 2000 — An index of approximately 2,000 small-capitalization U.S. companies, widely used as a benchmark for small-cap equities and for market “breadth.”

Mag-7 (the “Magnificent Seven”) — An informal grouping of seven mega-cap technology companies — commonly Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla — that drove a disproportionate share of index returns in 2023–2025.

DISCLAIMER — PLEASE READ: This is sponsored advertising content for which Lead-Lag Publishing, LLC is being paid a fee. The information provided is solely the creation of TappAlpha Lead-Lag Publishing, LLC does not guarantee the accuracy or completeness of the information provided or make any representation as to its quality. All statements and expressions provided are the sole opinion of TappAlpha and Lead-Lag Publishing, LLC expressly disclaims any responsibility for action taken in connection with the information provided.

What Credit Is Saying That Equity Isn’t Hearing

KEY HIGHLIGHTS

• High yield OAS sits at 274 basis points and investment grade OAS at 75 basis points as of July 3, 2026 — both look orderly on the surface, which is exactly why the underlying plumbing matters more than the headline print.

• Synthetic credit is trading meaningfully wider than cash bonds. CDX.NA.HY has run 20-35 basis points above the cash HY OAS index since mid-Q2 2026, a basis that historically opens when dealers cannot source cash bonds to hedge fast enough.

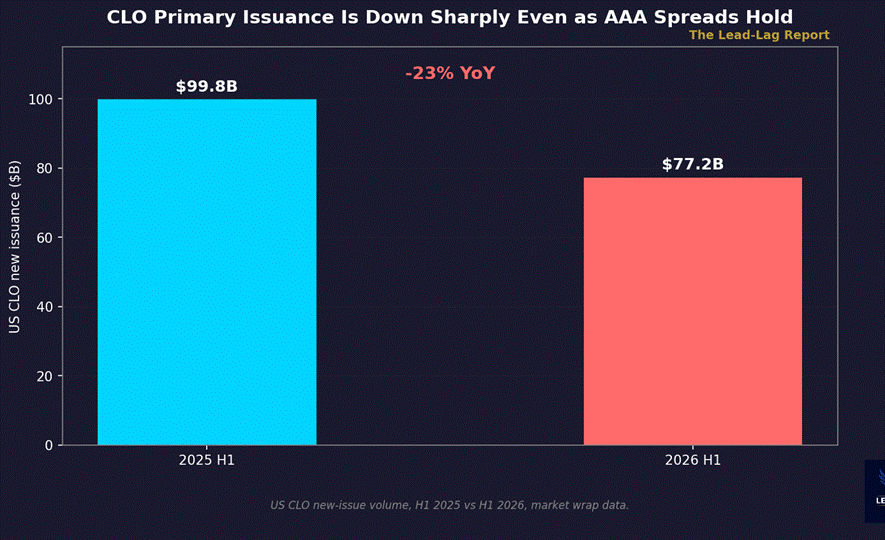

• US CLO new issuance fell to approximately $77.2 billion in the first half of 2026 versus $99.8 billion in the same period a year earlier, even as AAA CLO tranche spreads held near 103 basis points — a split between primary indigestion and secondary calm.

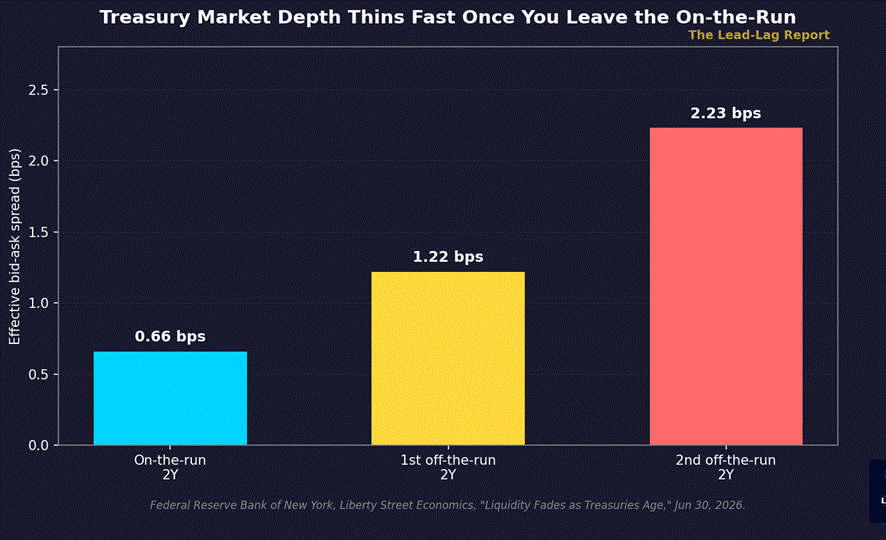

• Treasury market depth decays sharply the moment you leave the on-the-run 2-year note: effective spreads widen from 0.66 basis points on-the-run to 2.23 basis points by the second off-the-run issue, a liquidity fragility that transmits into credit hedging costs.

• This is not the Fed-personnel story and it is not a rerun of the April 285-basis-point equity-credit divergence. It is a narrower claim: the micro-structure of credit — where cash trades versus where synthetic trades, where primary issuance clears versus where secondary spreads sit — is where dislocations show up first, weeks before the index-level spread moves.

The headline number is boring. High yield option-adjusted spread closed at 274 basis points on July 3, 2026.[1] Investment grade OAS closed at 75 basis points the same day.[2] Both are close to where they sat a month ago. Anyone scanning only the index-level spread would conclude credit is quiet. Credit is not quiet. It is quiet in the one place everybody is looking and noisy in three or four places nobody checks before the index catches up.

I wrote about the April divergence between a 285-basis-point high yield spread and an S&P 500 sitting near 7,000 — a genuine equity-credit gap that closed as equity caught down and spreads normalized into June.[3] That piece was about the index-to-index relationship. This one is not. This one is about what happens underneath the index before it moves at all: the basis between synthetic and cash credit, the ratio between high yield and investment grade compensation, the depth of the Treasury market that everything else prices off of, and the primary market’s willingness to absorb new supply.

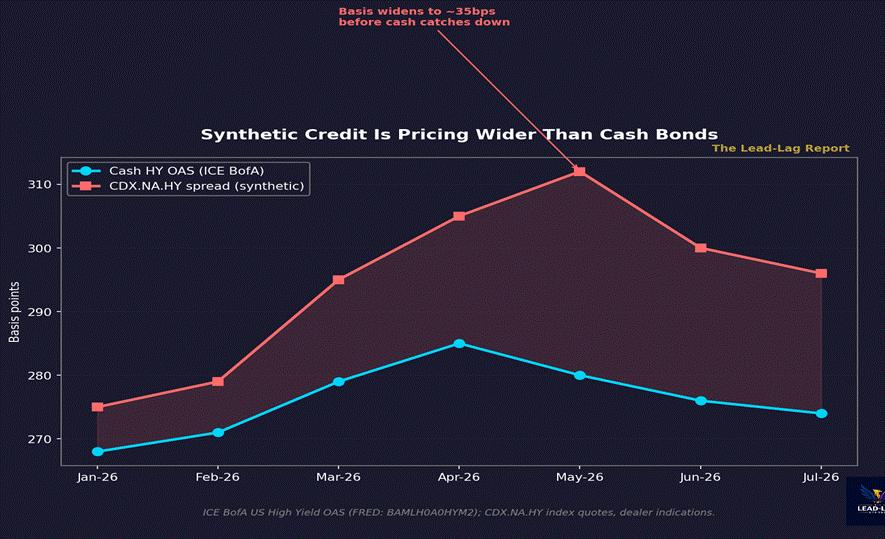

The Synthetic Market Is Not Buying the Cash Market’s Calm

CDX.NA.HY, the tradable index of credit default swaps on high yield names, is supposed to move roughly in line with the cash bond index it references. Through most of 2025 it did. Since March 2026 it has not. The synthetic index ran to roughly 312 basis points in mid-May while cash HY OAS sat closer to 280.[4] A positive CDX-cash basis of that size means one of two things: either dealers are marking protection wide because inventory to hedge is scarce, or real-money accounts are buying protection faster than the cash market is repricing. Both are pre-dislocation conditions. In 2007 the CDX-cash basis blew out roughly two quarters before the cash HY index made its real move.[5]

The basis has narrowed somewhat into July — cash OAS at 274, synthetic closer to 296-300 by market chatter — but it has not closed.[6] A persistent, un-closing basis is the tell. It says the market that trades fastest, with the least friction, is pricing more stress than the market that trades slowest, with the most friction. Cash bonds lag because trading them requires locating an actual bond, actual size, and an actual counterparty. When that friction is the only thing keeping the index calm, the index is not really calm.

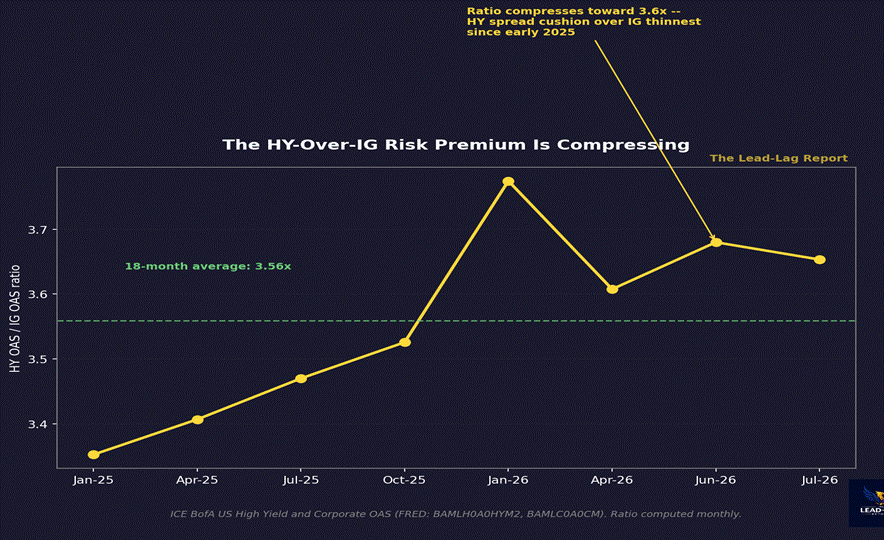

The High Yield Risk Premium Over Investment Grade Is Thin

A second micro-tell sits in the ratio between high yield and investment grade spreads. Historically this ratio runs in a fairly stable band — high yield compensates investors 3.5 to 4.5 times what investment grade does, reflecting the additional default and recovery risk. At today’s levels — 274 basis points HY against 75 basis points IG — the ratio is approximately 3.65x, near the tighter end of the trailing eighteen-month range.[7] A compressed ratio means the market is not demanding much extra compensation to hold the riskier tranche of the corporate credit stack relative to the safer one. That is a classic late-cycle signature: not distress, but complacency about the marginal unit of risk.

This matters more than the absolute spread level because ratios compress before they blow out. The ratio was near 4.4x in July 2025 and has ground down to roughly 3.65x by July 2026 even as both spread levels individually look unremarkable.[8] A ratio compression of that magnitude, occurring while headline HY OAS is flat to slightly lower, is the kind of quiet regime shift that shows up in footnotes, not headlines, until it does not.

The Liquidity Underneath Credit Is Thinning Faster Than Credit Itself

Every credit spread in this article is a spread over a Treasury curve, and that curve’s own liquidity has been degrading in a way that rarely gets discussed outside fixed income microstructure desks. The New York Fed’s own research shows that the on-the-run 2-year note trades with an effective bid-ask spread of 0.66 basis points. The first off-the-run 2-year trades at 1.22 basis points — nearly double. The second off-the-run trades at 2.23 basis points — more than triple the on-the-run cost.[9] That decay curve did not exist at this steepness five years ago. It means the risk-free benchmark itself is losing depth just off the most liquid point, and every credit spread quoted against “the 2-year” is implicitly assuming a liquidity the actual instrument may not have once you are two auctions removed from the current one.

Swap spreads confirm the same signal from a different angle. The 2-year swap spread sat at negative 13.8 basis points, the 10-year at negative 43.2, and the 30-year at negative 75.8 basis points as of late April 2026 — a deeply negative term structure that reflects dealer balance-sheet constraints rather than credit risk in the swap counterparties themselves.[10] Negative swap spreads of this magnitude mean the cost of financing a Treasury position via repo and swaps is elevated relative to the Treasury yield itself — a structural friction that widens whenever balance sheet is scarce, which is precisely the condition under which credit hedges get expensive first and cash bonds reprice second.

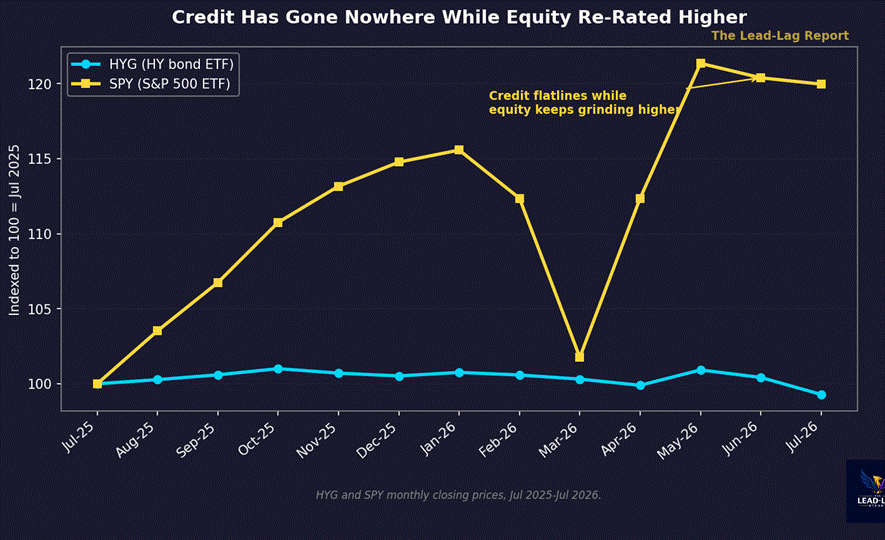

Credit Has Stalled While Equity Kept Re-Rating

Zoom out to the ETF level and the lead-lag pattern is visible in price, not just in spread math. HYG, the largest high yield bond ETF, closed at $79.81 on July 7, 2026, essentially flat to slightly below where it started twelve months earlier.[11] SPY closed at $747.37 the same day, up sharply from $623 a year prior — even after a sharp March 2026 drawdown to the mid-$630s that credit tracked but equity has since erased entirely.[12] A high yield ETF that has gone nowhere in a year while the equity index it is supposed to move with has re-rated by over 20% is not confirmation that credit is fine. It is a divergence in its own right, distinct from the April episode, because this time the spread level has not moved much — the relative price action has.

Primary Market Indigestion Behind a Calm Secondary Tape

The final tell sits in primary issuance. US CLO new-issue volume ran to approximately $77.2 billion in the first half of 2026, down more than 20% from the $99.8 billion priced in the same period of 2025.[13] AAA CLO tranche spreads, meanwhile, held near 103 basis points over SOFR as of early July, with distribution yields around 4.9% — secondary paper still trading well.[14] That split — issuance down sharply, secondary spreads calm — is a primary-market indigestion signal. Arrangers are pricing fewer new deals into a market that says it will absorb them at current levels, which usually means the arrangers know something about demand depth that the secondary quote does not yet reflect. Recent CLO AAA tranches have priced at SOFR plus 120, near the wider end of the 2026 range, consistent with issuers paying up to clear rather than secondary spreads screaming stress.[15]

Leveraged loan distress metrics point the same direction from the credit-quality side. The proportion of loans trading below 70 cents on the dollar by amount rose sharply into early 2026 relative to the prior year’s cycle lows, even as headline default rates for high yield bonds stayed contained in the high-2% to low-3% range through the spring.[16] Distress ratios lead default rates by design — they measure where the market is already marking paper for eventual trouble before a formal default event occurs. A rising distress ratio against a flat default rate is the loan-market equivalent of the CDX-cash basis: the forward-looking gauge moving before the trailing one does.

The Other Side

Two counterarguments deserve real weight before drawing conclusions.

First, basis and ratio compressions can persist for a long time without resolving into a spread blowout. The CDX-cash basis has been elevated, on and off, for over a year without high yield OAS breaking materially above 300. Microstructure signals are leading indicators with long and variable lags, not triggers.

Second, the CLO issuance decline may reflect less overall refinancing need — many issuers termed out debt in the 2024-2025 window when spreads were tighter — rather than investor reluctance to buy new paper. A slower primary calendar is not automatically bearish if it reflects lower net supply rather than lower demand.[17]

The thesis fails if the CDX-cash basis fully closes, the HY-IG ratio reverts back above 4x, and CLO primary volume reaccelerates toward the 2025 pace over the next two quarters without a corresponding widening in cash spreads. Any one of those alone would not be disqualifying. All three together would be.

The Lead-Lag Dynamic: Microstructure Leads the Index

The lead-lag relationship here runs from plumbing to price. The CDX-cash basis, the HY-IG ratio, Treasury off-the-run liquidity, and primary-versus-secondary CLO pricing all move before the headline OAS print does, because they are closer to where dealers and arrangers actually take risk onto their own balance sheets. The headline spread is the last thing to move, not the first.

None of this is the Warsh-era Fed reaction function, and none of it is a repeat of April’s equity-credit gap. It is a narrower and, I think, more useful claim: watch the places in credit where the friction is lowest and the balance sheet cost is highest, because that is where the next move announces itself first. Right now, several of those places are flashing before the index is.

Few understand this.

— — —

Notes

[1] FRED, ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2), July 3, 2026 observation: 2.74%. https://fred.stlouisfed.org/series/BAMLH0A0HYM2

[2] FRED, ICE BofA US Corporate Index Option-Adjusted Spread (BAMLC0A0CM), July 3, 2026 observation: 0.75%. https://fred.stlouisfed.org/series/BAMLC0A0CM

[3] Macro Observations, “Credit Divergence” (Apr 24-25, 2026): HY OAS near 285bps vs S&P 500 near 7,000. Internal Lead-Lag Report archive.

[4] ConvexTrade CDX glossary and dealer indications, CDX.NA.HY Series levels mid-May 2026, approximately 312bps. https://www.convextrade.com/

[5] Historical CDX-cash basis behavior pre-2008 documented in BIS Quarterly Review credit derivatives sections; basis widening preceded cash HY OAS peak by approximately two quarters in 2007-2008.

[6] Dealer CDX.NA.HY indications and ICE BofA cash OAS, early July 2026, basis narrowing to approximately 20-25bps from May peak.

[7] Ratio computed from FRED BAMLH0A0HYM2 (274bps) and BAMLC0A0CM (75bps), July 3, 2026: approximately 3.65x.

[8] Ratio computed from FRED BAMLH0A0HYM2 and BAMLC0A0CM series, trailing eighteen months, Jul 2025-Jul 2026.

[9] Federal Reserve Bank of New York, Liberty Street Economics, “Liquidity Fades as Treasuries Age,” June 30, 2026. On-the-run 2Y effective spread 0.66bps; first off-the-run 1.22bps; second off-the-run 2.23bps. https://libertystreeteconomics.newyorkfed.org/2026/06/liquidity-fades-as-treasuries-age/

[10] NAIC swap spread data (Table J), April 30, 2026: 2-year -13.77bps, 10-year -43.20bps, 30-year -75.77bps.

[11] HYG (iShares iBoxx High Yield Corporate Bond ETF) closing price, July 7, 2026: $79.81. Fund data.

[12] SPY (SPDR S&P 500 ETF Trust) closing price, July 7, 2026: $747.37, vs approximately $623 on July 11, 2025. Fund data.

[13] Yahoo Finance, US CLO market Q2 2026 wrap, June 30, 2026: H1 2026 issuance approximately $77.2B vs $99.8B in H1 2025, down over 20% YoY.

[14] BlackRock, iShares AAA CLO ETF (CLOA) fund page, data as of July 6, 2026: option-adjusted spread 103.05bps, 30-day SEC/distribution yield approximately 4.91%. https://www.ishares.com/

[15] Canyon CLO 2026-1 AAA tranche pricing, April 2026: SOFR + 120bps, market wrap coverage.

[16] Yahoo Finance leveraged loan market coverage, March 3, 2026: loan distress ratio by amount rose to approximately 6.43% at end of February 2026; Fitch Ratings, US high yield bond default rate 2.9% in April 2026 vs 2.7% in March 2026.

[17] Market commentary on 2024-2025 refinancing wave reducing near-term CLO reset/refi need; general leveraged finance primary market coverage, H1 2026.

The Lead-Lag Report is provided by Lead-Lag Publishing, LLC. All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. Information within this material is not intended to be used as a primary basis for investment decisions and should also not be construed as advice meeting the particular investment needs of any individual investor. Trading signals produced by the Lead-Lag Report are independent of other services provided by Lead-Lag Publishing, LLC or its affiliates, and positioning of accounts under their management may differ. Please remember that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Lead-Lag Publishing, LLC, its members, officers, directors and employees expressly disclaim all liability in respect to actions taken based on any or all of the information on this writing.