WHEN SPREADS ARE TIGHT, INFLATION IS HOT, AND THE CURVE IS STEEPENING — WHY CREDIT ROTATION CAN’T BE STATIC (ATACX)

KEY HIGHLIGHTS

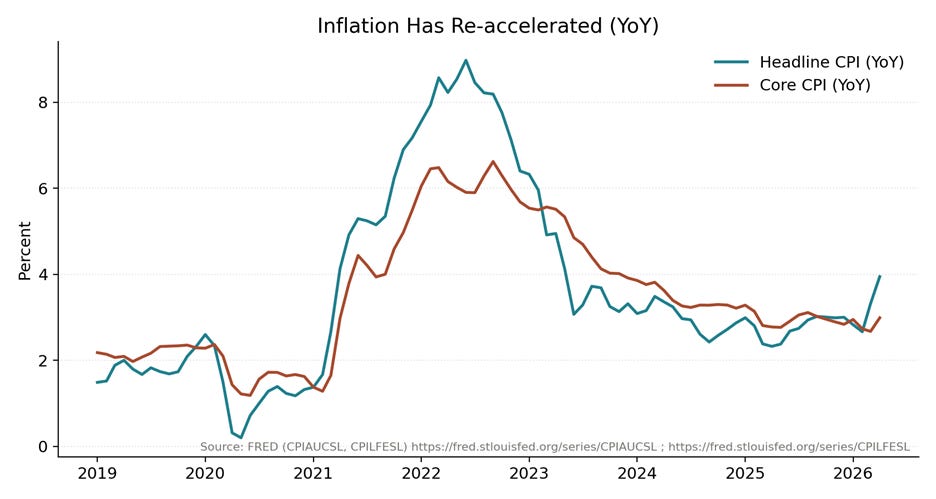

· **April CPI rose 0.6% m/m and 3.8% y/y**, while **core CPI rose 0.4% m/m and 2.8% y/y** — a mix that keeps policy uncertainty elevated.[1]

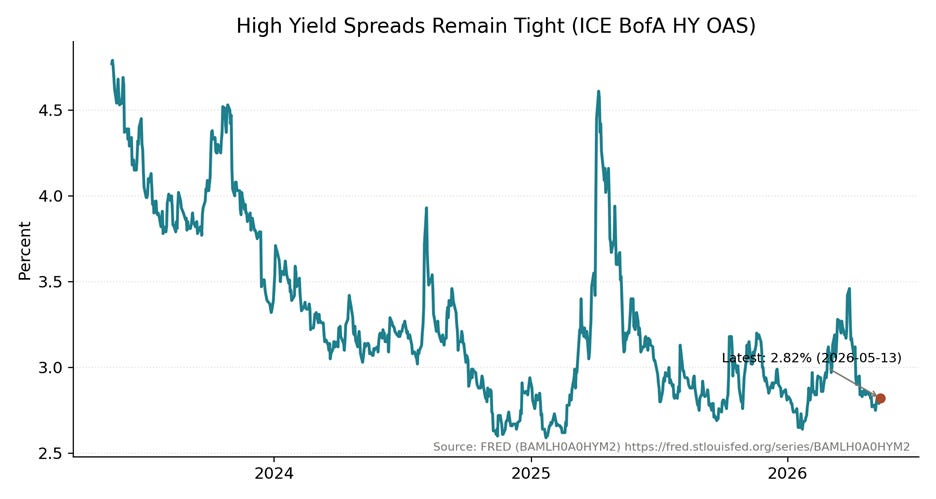

· **High yield option-adjusted spreads sit near 2.82%** (latest), a level that implies credit markets are still pricing a relatively benign default cycle.[2]

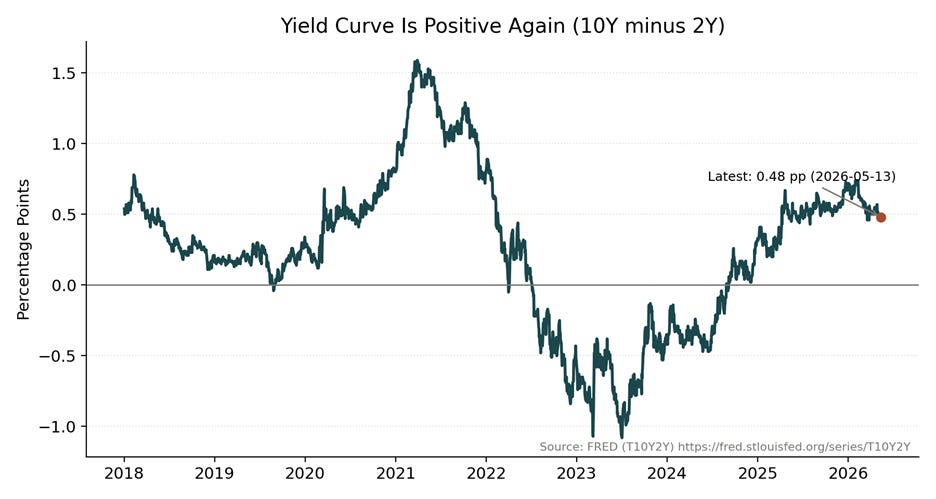

· The **10-year minus 2-year Treasury spread is around +0.48%**, signaling ongoing yield-curve steepening — a regime shift that can change which assets act “defensive.”[3]

· **Initial jobless claims are 211,000** (latest), consistent with a labor market that is slowing in pockets, but not breaking.[4]

· **ISM Services PMI is 53.6**, but the **Employment Index is 48.0**, highlighting late-cycle “growth-with-friction” conditions.[5]

I’ve found that the most dangerous market environments are the ones that feel stable: tight credit spreads, steady equity prices, and a narrative that tomorrow will look like yesterday. When inflation data re-accelerates while credit stays calm, I ask you to consider a simple possibility — the market is not pricing the next volatility regime correctly, and the cost of being static could rise quickly.

THE CURRENT BACKDROP: HOTTER INFLATION, “OK” GROWTH, AND A CREDIT MARKET THAT STILL BELIEVES

Inflation is the headline risk again, and not just because of year-over-year comparisons. In April, headline CPI rose 0.6% month-over-month, with core CPI up 0.4%.[1] Year-over-year, that puts headline CPI at 3.8% and core at 2.8%.[1] Those numbers matter because they keep the Federal Reserve’s reaction function uncertain: a single “good” month no longer changes the narrative when the trend is bumpier.

Yet the economy is not rolling over in a way that forces immediate easing. Initial jobless claims are 211,000 in the latest weekly data.[4] At the same time, services activity remains in expansion: ISM’s Services PMI printed 53.6 in April.[5] But look beneath the surface and you see the late-cycle tension: the ISM Services Employment Index is 48.0 — still signaling contraction in hiring even while activity stays positive.[5]

This is the kind of environment where both bulls and bears can be “right” for a while. Bulls can point to continued expansion. Bears can point to inflation pressure and labor-market cooling. The consequence is not necessarily a clean trend — it is regime shifts, bursts of volatility, and rotations that punish static allocations.

WHY I FOCUS ON CREDIT (NOT JUST EQUITIES) WHEN THE CYCLE TURNS

Equity investors often treat credit as a background variable — a confirmation signal. I treat it as a leading stress test.

Credit spreads embed a collective probability-weighted view of default risk, liquidity, and risk appetite. When spreads are wide, investors feel fear. When spreads are tight, investors feel comfort. But comfort can be the problem.

Today, the ICE BofA US High Yield Index option-adjusted spread is 2.82% (latest observation).[2] That is not a recessionary reading. It is not even a “mild stress” reading. In plain English, it suggests the credit market is still assuming the next twelve months will look like a typical, contained credit environment.

Now combine that with inflation re-acceleration.[1] If inflation stays sticky, rates can stay higher for longer, refinancing becomes more difficult, and dispersion inside high yield grows. In those conditions, the marginal borrower becomes the story — and credit spreads can move quickly even if the economy does not officially enter recession.

THE YIELD CURVE IS STEEPENING AGAIN — AND THAT CHANGES THE “DEFENSIVE” PLAYBOOK

One of the more important regime changes underway is the re-steepening of the yield curve. The 10-year minus 2-year Treasury spread is currently around +0.48% (latest).[3]

A positive and steepening curve can signal several things simultaneously:

1) the market expects growth/inflation to stay firmer than previously expected,

2) term premium can re-enter the conversation, and

3) longer-duration bonds can become more volatile.

For investors used to the post-2008 playbook, Treasuries are “always” the hedge. But hedges are regime-dependent. If inflation is the driver, and the curve is steepening, long duration can behave very differently than it did in a deflationary shock.

This is why rotation matters. It is not about predicting one perfect scenario — it is about having a rules-based way to adapt exposure as the market’s internal signals shift.

UTILITIES AS A SIGNAL: WHY A “BORING” SECTOR CAN LEAD CREDIT CONDITIONS

The most misunderstood part of our process is the signal itself.

At a high level, the ATAC credit-rotation framework uses intermarket behavior — specifically, how defensive equity leadership (utilities) behaves relative to the broad market — to infer what may come next for volatility and credit spreads.

Utilities are not magical. They are simply a real-time voting mechanism for risk preference. When investors quietly rotate into utilities, they are often de-risking before volatility shows up in the obvious places.

This is the core intuition:

That stress does not have to mean a “credit crisis.” It can mean spread widening from unusually tight levels. And when spreads are tight — like they are today — a move from complacency to caution can be enough to disrupt portfolios that assume stability.

WHAT THIS MEANS FOR POSITIONING: WHY A DUAL-REGIME APPROACH IS RATIONAL

I do not believe in always being “risk-on” or always being “risk-off.” The cycle changes, and the market changes faster than most investors want to admit.

In a re-accelerating inflation environment with tight spreads and a steepening curve, the biggest risk is not that you miss upside. The biggest risk is that you are positioned for yesterday’s regime.

This is where **The ATAC Rotation Fund (Ticker: ATACX)** becomes relevant. ATACX is a mutual fund structure that applies the same credit-rotation methodology associated with our broader work: rotating between credit risk-on exposure and defensive Treasury exposure based on intermarket signals.

The purpose is not to “call” the market. The purpose is to respond to it.

If credit spreads remain tight and risk appetite stays firm, the model can maintain a risk-on posture. But if defensive leadership emerges — the kind of shift that often happens before the headlines change — the model has a framework to move toward defense.

THE CONTRARIAN POINT: COMPLACENCY IS A DATA POINT, NOT A COMFORT BLANKET

Let me be direct: a 2.82% high yield OAS is not a guarantee of safety.[2] It is a data point about current psychology.

And the market’s psychology can change quickly when the macro data pushes back. A 0.6% monthly CPI print is not “cooling.”[1] A services economy that expands while employment contracts is not “healthy.”[5]

It is late-cycle ambiguity.

Late-cycle ambiguity is exactly when the value of an adaptive, rules-based approach tends to rise — because static portfolios rely on a stable correlation structure that may not persist.

CONCLUSION: ROTATION IS NOT A TRADE — IT’S A RISK MANAGEMENT PHILOSOPHY

When inflation is hot, the yield curve is steepening, and credit spreads are tight, I ask you to think in regimes rather than narratives.

The narrative can change overnight. The data changes gradually — until it doesn’t.

A credit-rotation approach is designed for that reality. It is designed to adapt when the market’s internal leadership shifts, rather than after the headlines declare a new regime.

That is the lens through which I view ATACX today.

Michael A. Gayed, CFA

ENDNOTES

1. U.S. Bureau of Labor Statistics, “Consumer Price Index Summary - 2026 M04 Results,” news release, May 12, 2026, accessed May 15, 2026, https://www.bls.gov/news.release/cpi.nr0.htm

2. Federal Reserve Bank of St. Louis, “ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2),” FRED, updated May 14, 2026, accessed May 15, 2026, https://fred.stlouisfed.org/series/BAMLH0A0HYM2

3. Federal Reserve Bank of St. Louis, “10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity (T10Y2Y),” FRED, updated May 13, 2026, accessed May 15, 2026, https://fred.stlouisfed.org/series/T10Y2Y

4. Federal Reserve Bank of St. Louis, “Initial Claims (ICSA),” FRED, updated May 14, 2026, accessed May 15, 2026, https://fred.stlouisfed.org/series/ICSA

5. Institute for Supply Management (ISM), “Services PMI at 53.6%; April 2026 ISM Services PMI Report,” PR Newswire, May 5, 2026, accessed May 15, 2026, https://www.prnewswire.com/news-releases/services-pmi-at-53-6-april-2026-ism-services-pmi-report-302761674.html

DISCLOSURES (ATACX)

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the “fear gauge” of Wall Street, is a real-time market index that measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com. Please read the Prospectuses carefully before you invest.

Investing involves risk including the possible loss of principal.

ATACX is distributed by Foreside Fund Services, LLC.

Learn more about ATACX at https://atacfunds.com/atacx/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.