Key Highlights

Federal Reserve minutes explicitly flagged historically low credit spreads and opaque private-market financing tied to the AI infrastructure buildout as financial-stability risks.¹

A high-profile data center financing tied to CoreWeave failed to secure third-party debt at desired terms, illustrating emerging underwriting friction.²

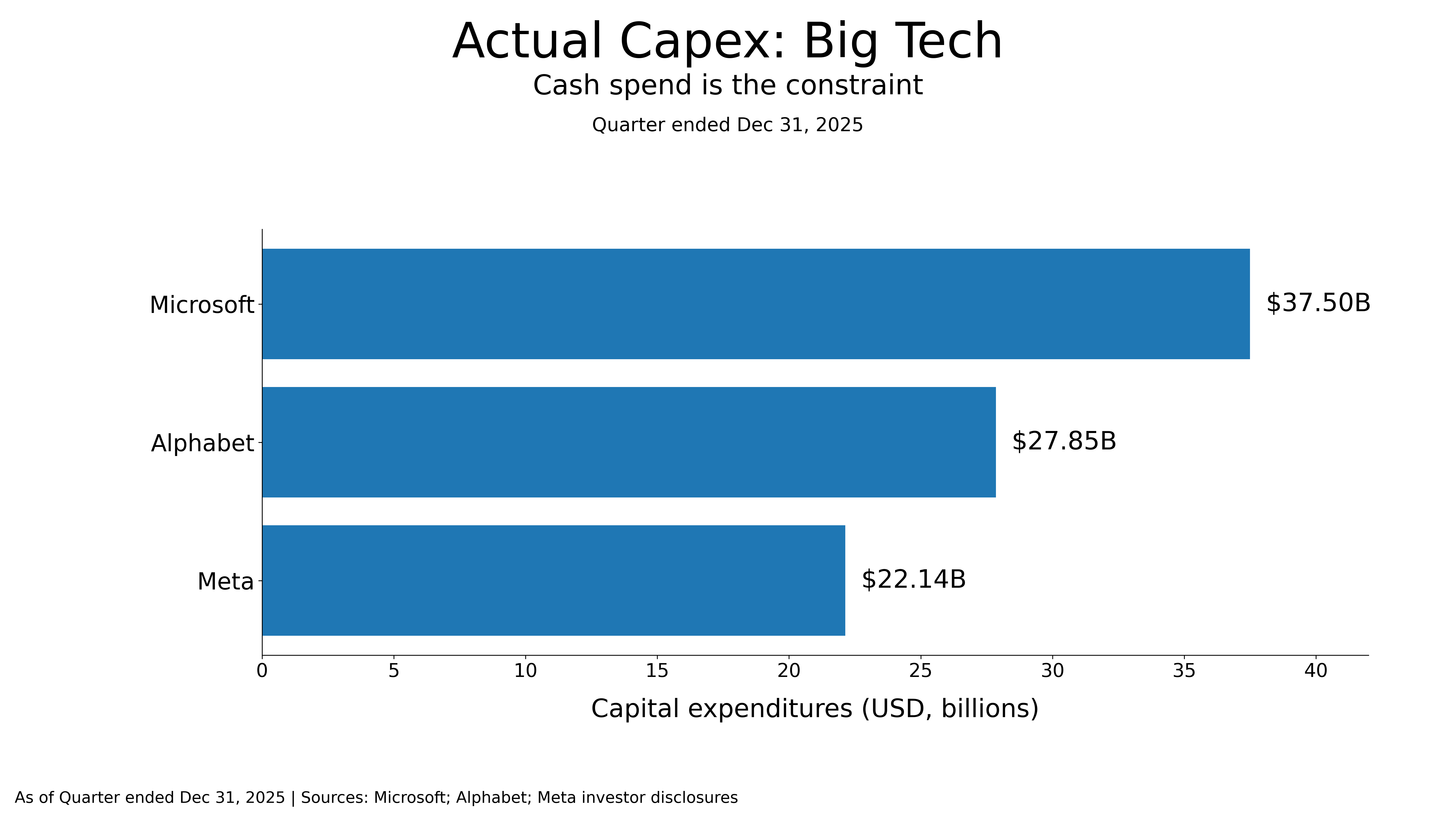

Big Tech’s 2026 capex guidance implies a historic scale of spending, with UBS forecasting a surge in investment-grade issuance to fund it.⁵⁶⁷⁹

Investment-grade and high-yield spreads sit near cycle tights, leaving limited buffer if growth expectations soften.¹¹¹³

If spreads widen while growth expectations cool, high-quality duration may outperform spread-heavy credit.

Financing Friction: When a Spending Boom Meets Underwriting Reality

Credit markets rarely collapse without warning. More often, they tighten incrementally—through failed syndications, tougher covenant demands, or rising skepticism toward marginal borrowers.

Two February developments brought that shift into focus. The Federal Reserve’s January meeting minutes noted “historically low credit spreads” and highlighted the need to monitor opaque private-market financing linked to the technology infrastructure buildout, alongside elevated equity valuations and concentration risk.¹ This language signals that policymakers now see credit conditions as central to the cycle.

At the same time, Business Insider reported that Blue Owl Capital struggled to arrange third-party financing for a large data center project tied to CoreWeave, with lenders citing concerns about tenant credit quality.² Blue Owl disclosed roughly $500 million of bridge financing through March 2026.² The deal’s difficulty does not constitute systemic stress. It does, however, illustrate how quickly lender appetite can shift when projects rely on sub-investment-grade counterparties.

This matters because much of the data center expansion uses short “mini-perm” construction loans—two-to-five-year facilities that must later refinance into longer-term project debt.³ That structure works when capital markets remain open and tenant credit is strong. It becomes fragile if refinancing windows narrow.

The Financial Times reported that developers are increasingly pursuing formal credit ratings—even mid-construction—to broaden the pool of institutional buyers.⁴ That shift from “easy syndication” to credit-structured placement reflects a market that is reassessing risk.

When spreads are tight, even modest underwriting friction can alter repricing dynamics.

Capex Scale, Issuance Scale, and Spread Asymmetry

The capex numbers now carry macro significance.