WHEN THE CURVE RE-STEEPENS AND SPREADS STAY QUIET, CREDIT RISK IS HIDING IN PLAIN SIGHT (ATACX)

KEY HIGHLIGHTS

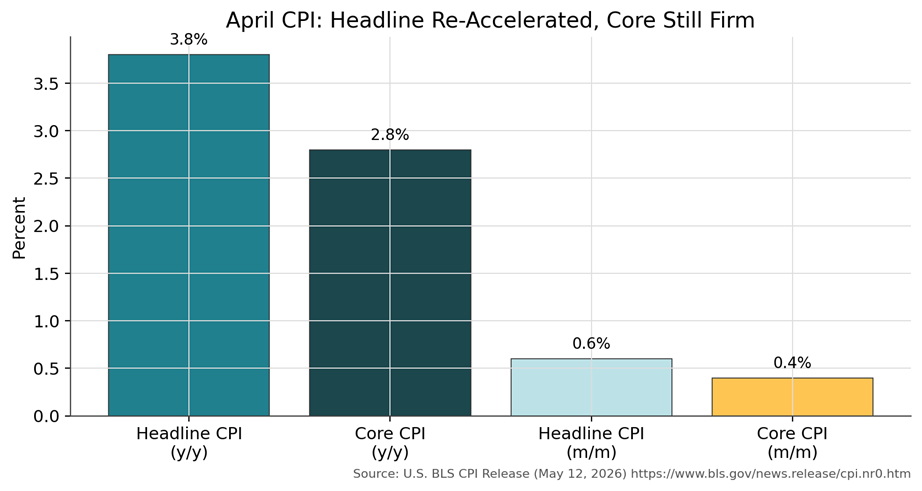

· **Headline CPI rose 0.6% m/m and 3.8% y/y in April**, while **core CPI rose 0.4% m/m and 2.8% y/y**—a reminder that inflation volatility is back in the driver’s seat.[1]

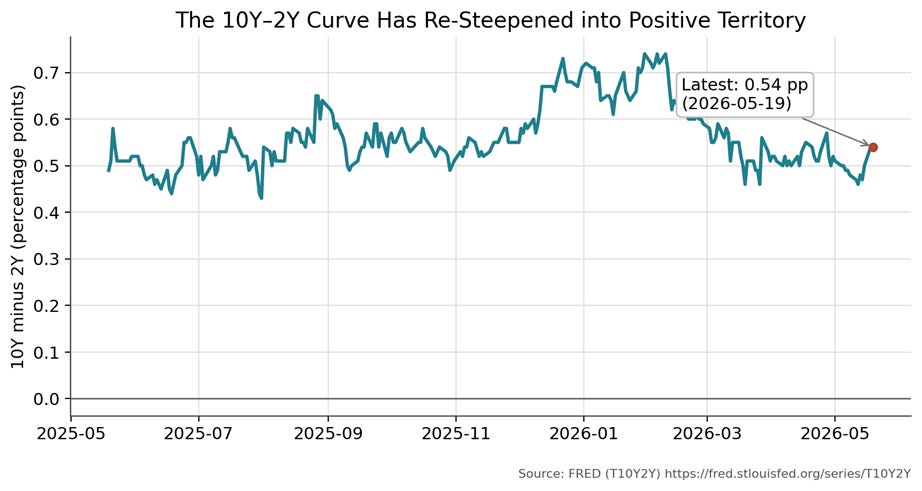

· The **10Y–2Y Treasury spread is back to +0.49 percentage points**—a sharp contrast to the deep inversion that dominated the prior cycle and a sign the market is re-pricing term premium.[2]

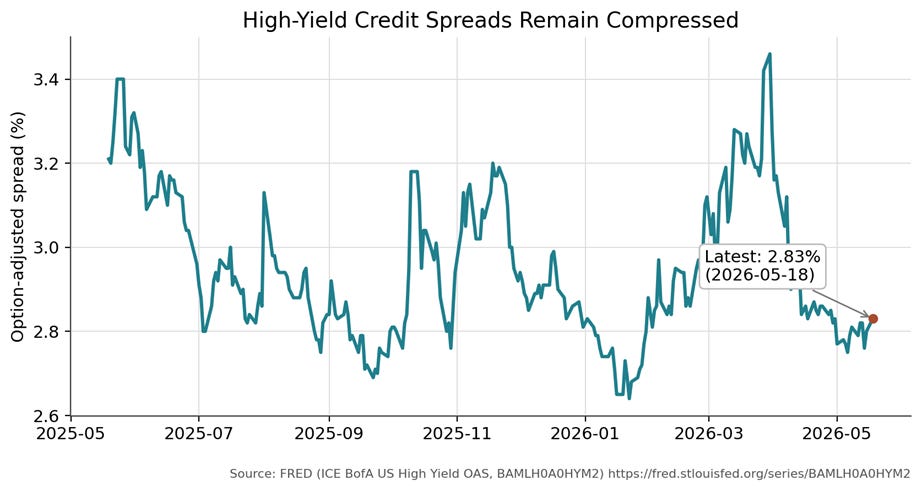

· Even with a hotter inflation pulse and a re-steepening curve, **high-yield option-adjusted spreads sit at just 2.80%**—a level that implies notable complacency about future volatility.[3]

· In this type of “quiet credit” regime, I believe the most important question isn’t whether the economy slows—it’s whether credit *reacts* fast enough when risk appetite turns.

I’ve found that the easiest time to ignore risk is when the market seems to have already made peace with it. And right now, the combination of a re-steepening yield curve and still-compressed credit spreads is exactly the kind of backdrop that can lull investors into assuming the next drawdown will be orderly—until it isn’t.

THE MACRO BACKDROP: INFLATION VOLATILITY IS BACK

The latest CPI report is not just about the level of inflation—it’s about the *distribution* of outcomes investors have to contend with.

April’s headline CPI accelerated **0.6% month-over-month**, pushing the year-over-year rate to **3.8%**.[1] Core CPI (excluding food and energy) was also firm at **0.4% month-over-month** and **2.8% year-over-year**.[1] In other words: the “all clear” signal that many investors hoped would arrive in 2026 has not arrived.

When inflation re-accelerates, the market’s reflex is to focus on what the Fed will do next. But the more subtle—and in my view more important—implication is what inflation volatility does to *financial conditions* and *risk appetite*. Inflation uncertainty changes how investors discount cash flows, how lenders price risk, and how quickly liquidity can disappear when positioning is crowded.

This is precisely why credit-sensitive strategies can’t rely on “set it and forget it” allocations. The regime is changing, and the cost of being late can be far higher than the cost of being early.

THE YIELD CURVE MESSAGE: TERM PREMIUM IS NOT A FOOTNOTE ANYMORE

For much of the post-2022 period, curve inversion became the market’s favorite recession barometer. But inversion is not the signal; *the transition away from inversion* is often where markets can become unstable.

As of the latest observation, the **10-year minus 2-year Treasury spread is +0.49 percentage points**.[2] That’s not a trivial development—it is a shift in the market’s pricing of growth, inflation, and the path of policy rates.

A re-steepening curve can happen for good reasons (stronger growth expectations) or for less comfortable reasons (higher inflation risk and rising term premium). When inflation volatility is reasserting itself, it’s difficult to argue that term premium is benign.

Why does this matter for credit? Because credit spreads are not just compensation for default risk—they’re also compensation for liquidity risk and the potential for volatility shocks. A world where the curve steepens *because uncertainty is rising* is a world where credit can gap wider even without a textbook recession.

THE CREDIT PUZZLE: SPREADS ARE STILL TOO CALM

Here is the tension I want readers to focus on: macro volatility is rising, the yield curve is re-steepening, and yet credit spreads remain extremely tight.

The **ICE BofA US High Yield Index Option-Adjusted Spread is 2.80% (as of May 20, 2026)**.[3] Historically, spreads at these levels have often signaled one of two things:

1) the market expects a very benign path for growth and defaults, or

2) the market is underpricing the probability of a volatility event.

When spreads are compressed, the “carry trade” mentality tends to dominate. Investors reach for yield, assuming that any wobble will be temporary. The problem is that credit does not always re-price gradually.

In my work, I’m less interested in predicting *when* spreads will widen and more interested in recognizing *when the setup is fragile*. Tight spreads are not a guarantee of safety. In many cases, they’re an indicator that the market has already crowded into the same risk posture.

That’s where rotation becomes essential—not as a prediction tool, but as a response framework.

WHY UTILITIES MATTER IN A CREDIT DISCUSSION

One of the more persistent relationships I’ve studied is the role of Utilities as an intermarket signal.

Utilities are a “bond proxy” sector: higher dividend yield, more rate sensitivity, and often a defensive tilt when equity volatility rises. When Utilities begin to outperform the broader market, it can be an early warning that investors are quietly shifting toward defense—often before that shift shows up in credit spreads.

There is a behavioral reason for this. Equity investors can rotate sectors quickly, with low friction. Credit investors, by contrast, tend to move more slowly—especially when spreads are tight and the carry is tempting. By the time credit fully prices the risk-off regime, the move can be sharp.

This is why my approach emphasizes *leading* signals rather than coincident ones.

WHAT THIS MEANS FOR A CREDIT-ROTATION APPROACH (ATACX)

This is the environment that highlights why **The ATAC Rotation Fund (Ticker: ATACX)** exists.

ATACX is designed around a simple idea: credit regimes shift, and the best time to respect that shift is not after spreads blow out, but when intermarket signals begin to change beneath the surface.

The fund uses a rules-based credit rotation methodology that seeks to move between credit exposure and a more defensive posture as conditions warrant. The goal is not to avoid every drawdown. The goal is to avoid being structurally exposed to the *wrong* part of the cycle.

In a backdrop where inflation is re-accelerating, the curve is re-steepening, and spreads remain complacent, I ask investors to consider a key question:

If credit is pricing perfection while macro uncertainty is rising, what happens when the first real shock arrives?

Rotation is an attempt to answer that question without pretending we can forecast the catalyst.

THE BOTTOM LINE

When investors see tight spreads, they often interpret that as an “all clear” signal. I interpret it as a reminder to pay attention to what the market is not pricing.

Right now, we have:

- a hotter inflation pulse,

- a yield curve that has meaningfully re-steepened, and

- credit spreads that still imply a remarkably benign volatility outlook.

That combination does not guarantee a credit event—but it *does* suggest that the asymmetry has changed.

This is exactly when a tactical, signal-driven rotation framework can be most valuable.

ENDNOTES

[1] U.S. Bureau of Labor Statistics, “Consumer Price Index Summary,” news release, May 12, 2026, https://www.bls.gov/news.release/cpi.nr0.htm

[2] Federal Reserve Bank of St. Louis, “10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity Rate (T10Y2Y),” FRED, accessed May 22, 2026, https://fred.stlouisfed.org/series/T10Y2Y

[3] Federal Reserve Bank of St. Louis, “ICE BofA US High Yield Index Option-Adjusted Spread (BAMLH0A0HYM2),” FRED, accessed May 22, 2026, https://fred.stlouisfed.org/series/BAMLH0A0HYM2

Michael A. Gayed, CFA

DISCLOSURES (ATACX)

The Fund’s investment objectives, risks, charges, expenses and other information are described in the statutory or summary prospectus, which must be read and considered carefully before investing. You may download the statutory or summary prospectus or obtain a hard copy by calling 855-ATACFUND or visiting www.atacfunds.com/atacx/. Please read the Prospectuses carefully before you invest.

Junk debt, also known as high-yield bonds or speculative-grade debt, refers to fixed-income securities issued by companies or governments with lower credit ratings, offering higher interest rates to compensate investors for the elevated risk of default.

The VIX index, often called the “fear gauge” of Wall Street, is a real-time market index that measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 index options prices, serving as a key barometer of investor sentiment and market risk.

The ICE BofA BB US High Yield Index Option-Adjusted Spread measures the yield differential between BB-rated corporate bonds and a spot Treasury curve, quantifying the risk premium for below-investment-grade debt with a BB rating in the US market.

As with all ETFs, Fund shares may be bought and sold in the secondary market at market prices. The market price normally should approximate the Fund’s net asset value per share (NAV), but the market price sometimes may be higher or lower than the NAV. The Fund is new with a limited operating history. There are a limited number of financial institutions authorized to buy and sell shares directly with the Fund, and there may be a limited number of other liquidity providers in the marketplace. There is no assurance that Fund shares will trade at any volume, or at all, on any stock exchange. Low trading activity may result in shares trading at a material discount to NAV.

Because the Fund invests in Underlying ETFs an investor will indirectly bear the principal risks of the Underlying ETFs, including but not limited to, risks associated with investments in ETFs, equity securities, growth stocks, large and small capitalization companies, non-diversification, fixed income investments, derivatives and leverage. The prices of fixed income securities may be affected by changes in interest rates, the creditworthiness and financial strength of the issuer and other factors. An increase in prevailing interest rates typically causes the value of existing fixed income securities to fall and often has a greater impact on longer duration and/or higher quality fixed income securities. The Fund will bear its share of the fees and expenses of the underlying funds. Shareholders will pay higher expenses than would be the case if making direct investments in the underlying funds.

Because the Fund expects to change its exposure as frequently as each week based on short-term price performance information, (i) the Fund’s exposure may be affected by significant market movements at or near the end of such short-term periods that are not predictive of such asset’s performance for subsequent periods and (ii) changes to the Fund’s exposure may lag a significant change in an asset’s direction (up or down) if such changes first take effect at or near a weekend. Such lags between an asset’s performance and changes to the Fund’s exposure may result in significant underperformance relative to the broader equity or fixed income market. Because the Adviser determines the exposure for the Fund based on the price movements of gold and lumber, the Fund is exposed to the risk that such assets or their relative price movements fail to accurately predict future performance.

Past performance is no guarantee of future results.

Investing involves risk including the possible loss of principal.

ATACX is distributed by Foreside Fund Services, LLC.

Learn more about ATACX at https://www.atacfunds.com/atacx/ Lead-Lag Publishing, LLC is not an affiliate of Tidal/Toroso or ACA/Foreside.